by Timothy Taylor, Conversable Economist

The number of shareholder-owned US corporations is in steep decline, falling from 7,507 in 1997 to 3,766 by 2015. Thus, Kathleen M. Kahle and René M. Stulz ask “Is the US Public Corporation in Trouble?” in their article in the Summer 2017 Journal of Economic Perspectives (31:3, pp. 67-88). (Full disclosure: I’ve been Managing Editor of JEP since its inception in 1987, and thus may be predisposed to believe that the articles appearing there are worth reading! All articles in JEP, from the most recent issue back to the first, are freely available online compliments of its publisher, the American Economic Association.)

Please share this article – Go to very top of page, right hand side, for social media buttons.

The blue line in this figure shows the number of publicly-trades US corporations. The bars show (inflation-adjusted) market capitalization–that is, the total value if you take all the shares of all the companies and multiply by the price of the shares.

Kahle and Stulz consider the evidence on US corporations along a number of dimensions. Here are a few of their points that caught my eye:

- “In 1975, the US economy has 22.4 publicly listed firms per million inhabitants. In 2015, it has just 11.7 listed firms per million inhabitants.”

- The main reason for the decline in the number of firms is mergers of existing firms–combined with a slowdown in the rate of new firms being created. “[T]he number of initial public offerings decreases dramatically after 2000, such that the average yearly number of initial public offerings after 2000 is roughly one-third of the average from 1980 to 2000 …”

- The average age of a public firm was 12.2 years in 1995, and 18.4 years in 2015.

- “A simple but rough benchmark is to compute the percentage of listed firms that are small, defined as having a market capitalization of less than $100 million in 2015 dollars. In 1975, 61.5 percent of listed firms are small … This percentage peaks at 63.2 percent in 1990, and then falls. The share of small, listed firms dropped all the way to 19.1 percent of listed firms in 2013, before rebounding slightly to 22.6 percent in 2015. In other words, small listed firms are much scarcer today than 20 or 40 years ago.”

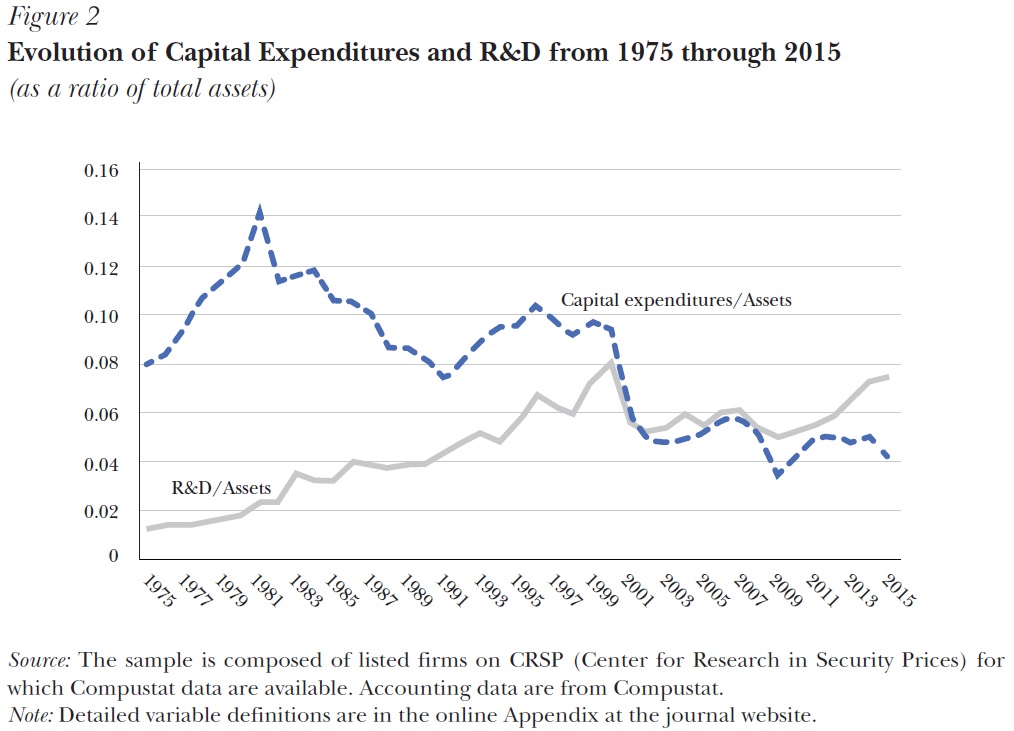

- “Listed firms have a much lower average ratio of capital expenditures to assets and a much higher ratio of R&D expenditures to assets in 2015 than they do in 1975. Figure 2 shows the evolution of average R&D to assets over time.”

- “[I]n 1975, 50 percent of the total earnings of public firms is earned by the 109 top-earning firms; by 2015, the top 30 firms earn 50 percent of the total earnings of the US public firms. Even more striking, in results not separately tabulated here, we find that the earnings of the top 200 firms by earnings exceed the earnings of all listed firms combined in 2015, which means that the combined earnings of the firms not in the top 200 are negative. In 1975, the 94 largest firms own half of the assets of US public firms, but 35 do so in 2015. Finally, 24 firms account for half of the cash holdings of public firms in 1975, but 11 firms do in 2015.”

- “None of our leverage measures are elevated at the end of the sample period in 2015, suggesting that concerns about corporate leverage are less relevant for public firms now than at other times during the sample period. Leverage is even less of an issue now because interest rates are extremely low since the credit crisis. Hence, interest paid as a percentage of assets has never been as low during the sample period as in recent years …”

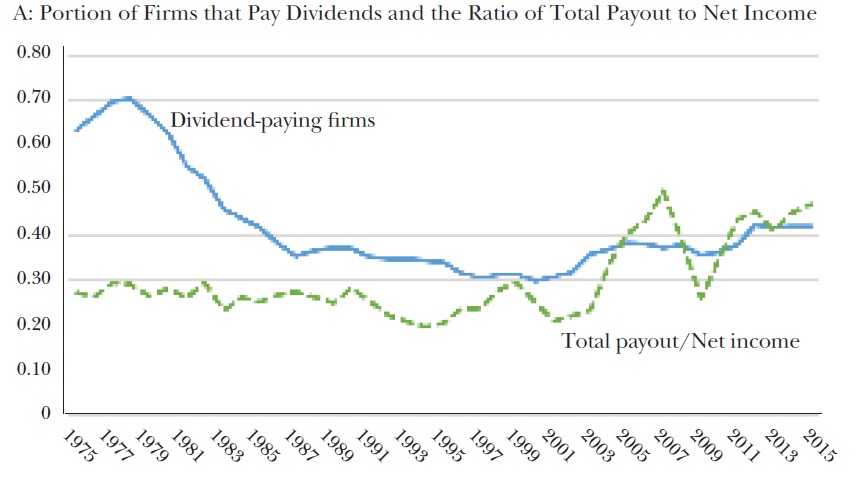

- The share of firms paying dividends dropped substantially in the 1980s and 1990s, to the point where one occasionally read about “the death of the dividend.” However, firms have been paying out more to shareholders through the mechanisms of repurchasing shares, and so the payouts of firms as as share of their net income has risen substantially since 2000.

- “These explanations imply that there are fewer public firms both because it has become harder to succeed as a public firm and also because the benefits of being public have fallen. As a result, firms are acquired rather than growing organically. This process results in fewer thriving small public firms that challenge larger firms and eventually succeed in becoming large. A possible downside of this evolution is that larger firms may be able to worry less about competition, can become more set in their ways, and do not have to innovate and invest as much as they would with more youthful competition. Further, small firms are not as ambitious and often choose the path of being acquired rather than succeeding in public markets. With these possible explanations, the developments we document can be costly, leading to less investment, less growth, and less dynamism. … It may be in the best interests of shareholders for firms to behave that way, but the end result is likely to leave us with fewer public firms, who gradually become older, slower, and less ambitious. Consequently, fewer new private firms are born, as the rewards for entrepreneurship are not as large. And those firms that are born are more likely to lack ambition, as they aim to be acquired rather than to conquer the world.”

In 1962, Richard Nixon announced that he was leaving politics and told the assembled journalists, with whom he had had a relationship that could politely be described as “adversarial“:

“Just think how much you’re going to be missing. You don’t have Nixon to kick around any more.“

Of course, Nixon came back, and I expect that the US public corporation will come back, as well. But even for those who like to kick around the public corporation, these patterns should offer some cause for concern. The public corporation, for all its warts and flaws, has been a primary engine of US economic growth for more than a century. When it no longer makes economic sense for most small firms to become public corporations, when the number of firms is being continually depleted by mergers, and when large firms are often paying out a larger share of their income or hoarding cash rather than investing, these are all legitimate causes for public concern.

The Kahle-Stulz paper is the first of four in a “Symposium about the Modern Corporation” in the Summer 2017 issue of JEP, and those interested in the subject will want to check out the other papers, too. Lucian A. Bebchuk, Alma Cohen, and Scott Hirst discuss “The Agency Problems of Institutional Investors (pp. 89-102). The traditional problem of corporate governance has been what economists called “the separation of ownership and control”, which refers to the fact that while shareholders technically own corporations, a very large number of relatively small shareholders are likely to have a hard time actually controlling the corporation. Instead, top executives and boards of directors may be able to cooperate in back-scratching arrangements that make their own lives easier. However, in recent years, large blocks of stock are owned by “institutional” investors, like the giant stock market index funds. Unlike the much smaller shareholders of the past, the large institutional investors have some power to exert control over large companies–but they may have much incentive to do so. After all, one large indexed mutual fund gets no advantage over other large indexed mutual funds by exercising oversight over corporations. No matter what one index fund does, or doesn’t do, investors in index funds just get the overall average market outcome. Luigi Zingales offers some thoughts “Towards a Political Theory of the Firm” (pp. 113-30). He writes of the dangers of a “Medici vicious circle,” which can be described in the slogan: “Money to get power. Power to protect money.” He writes:

“The ideal state of affairs is a “goldilocks” balance between the power of the state and the power of firms. If the state is too weak to enforce property rights, then firms will either resort to enforcing these rights by themselves (through private violence) or collapse. If a state is too strong, rather than enforcing property rights it will be tempted to expropriate from firms. When firms are too weak vis-à-vis the state, they risk being expropriated, if not formally (with a transfer of property rights to the government), then substantially (when the state demands a large portion of the returns to any investment). But when firms are too strong vis-à-vis the state, they may shape the definition of property rights and its enforcement in their own interest and not in the interest of the public at large, as in the Mickey Mouse Copyright Act example. …

“While the perfect “goldilocks” balance is an unattainable ideal, given that ongoing events will expose the tradeoffs in any given approach, the countries closest to this ideal are probably the Scandinavian countries today and the United States in the second part of the twentieth century. Crucial to the success of a goldilocks balance is a strong administrative state, which operates according to the principal of impartiality (Rothstein 2011) and a competitive private sector economy.”

Anat R. Admati provides “A Skeptical View of Financialized Corporate Governance” (pp. 131-50). She points out that the modern corporation has often sought to provide appropriate incentives to top corporate executives by linking their compensation to various financial measures, like stock market prices. However, she argues that this approach can in many cases provide misguided incentives, and does not seem to limit or hinder an ongoing parade of corporate scandals. From the abstract:

“Managerial compensation typically relies on financial yardsticks, such as profits, stock prices, and return on equity, to achieve alignment between the interests of managers and shareholders. But financialized governance may not actually work well for most shareholders, and even when it does, significant tradeoffs and inefficiencies can arise from the conflict between maximizing financialized measures and society’s broader interests. Effective governance requires that those in control are accountable for actions they take. However, those who control and benefit most from corporations’ success are often able to avoid accountability. The history of corporate governance includes a parade of scandals and crises that have caused significant harm. After each, most key individuals tend to minimize their own culpability. Common claims from executives, boards of directors, auditors, rating agencies, politicians, and regulators include “we just didn’t know,” “we couldn’t have predicted,” or “it was just a few bad apples.” Economists, as well, may react to corporate scandals and crises with their own version of “we just didn’t know,” as their models had ruled out certain possibilities. Effective governance of institutions in the private and public sectors should make it much more difficult for individuals in these institutions to get away with claiming that harm was out of their control when in reality they had encouraged or enabled harmful misconduct, and ought to have taken action to prevent it.”