by Philip Pilkington

Article of the Week from Fixing the Economists

Recently I did a post on the work of Katharina Pistor and included some very broad details of something related that I’m working on. Despite me saying clearly and multiple times in the piece that I was massively oversimplifying I nevertheless got some response pointing to supposed “errors” and “banalities” in what I was saying.

The most substantive was that prices cannot be understood in terms of stock-flow equilibria. What followed was a rather muddled argument but one that I think can be summarised by quoting here two comments that were left on that blog. The first ran like this:

At any moment, price in financial exchanges is determined by current orders placed by participants. There is no reason why those should be linked to past purchases in a mechanistic way implied by stock-flow relationship. Also, stock variables evolve, by definition, continuously, and thus cannot jump, while prices jump all the time.

So, the criticism here is that whereas with, say, income the stock rises in lockstep with the accumulation of flows and there are no “jumps” in the case of prices we sometimes see such “jumps”. The latter part of this statement is obvious nonsense and rests on taking too literally the term “flow”. What the commenter was presumably imagining was a bathtub with a tap turned on, and the steady “flow” of the water out of the tap adding to the “stock” of water in the tub.

But this metaphor, taken too literally, can blind us what we’re really dealing with here. In economics they can indeed “jump”. Imagine we have a flow of income that adds $5 to the stock every second. After ten seconds had passed the stock would have risen by $50 in a smooth, flow-like manner. But now let’s say that we alter this and say that $50 are added at every ten second interval. Then we will no longer see the same steady flow dynamic that we saw before and rather we will see what appears to be a “jump” in the stock every ten seconds.

Of course, this is actually an illusion because the second scenario is no more a “jump” than the first scenario, it just appears that way due to our having first conceived of the flow relation as being the accumulation of $5 every second and then later changing the nature of the flow relation.

The second criticism was tied to this and made slightly more sense, but was nevertheless based on another misconception. Here it is:

If asset price was stock variable driven by investment flows, that would mean that whenever I invest 1$ in the asset, the price always goes up by 1$ (or some multiple of it, but always by the same amount). That’s how a stock-flow relationship is defined, and it’s also how financial markets DO NOT work, period.

The ambiguity here is in the brackets. In a Keynesian multiplier stock-flow relationship, for example, the stock will rise by the amount of income times, say, the marginal propensity to consume (MPC). So, say we have a rise in income of $1 and the MPC is 0.2 we will have a total rise in income of $1.20. As the commenter says this is indeed “always the same amount”, but only over a set period.

So, what is the corollary when thinking of price dynamics? Simple. It’s a Marshallian construction called the price elasticity of demand. If a financial asset has a very low price elasticity of demand any buying/selling of this asset will have substantial price effects, while if there is a high price elasticity of demand any buying/selling of this asset will have far less significant price effects.

In marginalist economics, of course, it is thought that there is a negative relationship between, for example, price and quantity demanded. In my framework this is not necessarily true, yet the basic insight in the price elasticity of demand holds nevertheless — if in slightly modified form.

For an excellent real world example of this with reference to the gold market see this post by hedge fund manager Mark Dow.

Thus, if we imagine that we know the price elasticity of demand at any point in time — just as we imagine that we know the MPC in the multiplier relation — we can ensure that there are fixed relations between investment flows and price, as mediated by the price elasticity of demand. Just as the MPC provides the “bridge” between income received and total income in the multiplier relationship, the price elasticity of demand provides the “bridge” between investment flows into a financial asset and the price.

This is, of course, not a very heterodox idea at all, but it seems that some mainstream economists, so used to their downward-sloping demand curves and their efficient markets, have never really thought through in detail how prices work in the real world. But then, that is what my work is trying to remedy. That everyone will tell me that what I am saying is “sooooo obvious” is a given. But I’ve seen too many mistakes and misconceptions to be convinced that what I’m doing is not important; and, ironically, it seems to be those who tell me how banal and unimportant what I’m doing is that could do with being exposed to it the most. But is that not always the case in economics?

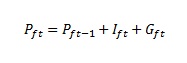

Addendum: We can lay this argument out mathematically with reference to the equations we laid out in the last post. The first equation laid out there was as follows:

We can modify this by adding a price elasticity of demand term, d, as follows:

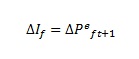

We can then take the second equation we laid out in our previous post, which was:

And we can substitute this in to get:

Now we can see that if the price elasticity of demand is a larger number, say above 1, then the effects of increased/decreased investment on price will be greater. While if it is a smaller number, say below 1, then the effects of increased/decreased investment on price will be lesser.