by Dee Woo

Summary

- What’s behind the property fever in China?

- The financial truth of the destocking of China’s property market.

- We use quantitative analysis to predict when the bubbles of China’s housing market will burst.

1. What’s behind the property fever in China?

Before Mount Vesuvius erupted in A.D. 79, the nobles in Pompeii carried on their extravagant lives without a care in the world. Humans have very narrow visions, oftentimes can only see people around them fiddling away the good times, and have no idea that their landmarks, such as Mount Vesuvius to Pompeii, can evolve into such a deadly force of mass-destruction.

Since April 2015, the property price in China has been growing fast, and the trading volume per month and price YoY growth rate have broken all previous records by significant margins. This market rally is the strongest in the 18-years long bull market of China’s housing market. Housing market speculation has become the talk of the town so much so that people would give up their own business or jobs for it.

However, the real picture of China’s economy couldn’t be more depressing apart from the red-hot housing market: the GDP growth rate has been falling steadily towards the historical lows since “Reform & Opening up”; the export values (rolling 12 months) YoY growth rate has been declining for the past 6 years and arrive at the level last seen in the aftermath of the 2009 global financial tsunami. If above facts were ignored, the period since April 2015 would be seen as the most prosperous by many, when the housing market is the hottest on record. China’s housing market is truly reminiscent of Pompeii right before A.D. 79.

Humans have very narrow visions, oftentimes can only see people around them fiddling away the good times, and have no idea that their landmarks-such as Mount Vesuvius to Pompeian, can evolve into such a deadly force of mass-destruction. However, the evolvement of the force of mass-destruction can be spotted well in advance by analyzing the macro financial economic data.

In the 18 years long bull market of China’s housing market, there are two market makers: local governments, and the institutional money which are property developers and their financial backers(banks, insurance companies and shadow banks). the retail investors are the residents-ordinary people enthusiastic about investing, the vanguard of which were nicknamed Chinese Damas.

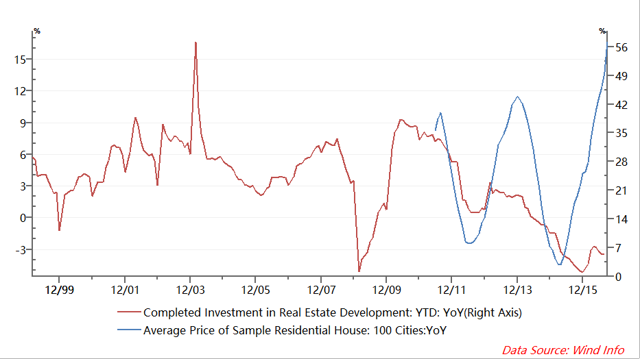

In the current housing market rally, how do the market makers and Chinese Damas (aka ordinary people) fare? Let’s look at the chart below:

Chart 1

2. The financial truth of the destocking of China’s property market

The destocking of property market is one of the 5 essential economic tasks in 2016 given by the central government, which are now one of the hottest trending economic topics in China.

According to Chart 1, in this rally, the YoY growth rate of “Average House Price in China” now reached its highest level since the data was collected and also surpassed its previous record by significant margins, meanwhile the YoY growth rate of” Completed Investment in Real Estate Development” drops to the historical lows and stay there since April 2015 when the housing market started to take off. This means that institutional money has flown out of the property sector during this rally.

If institutional money doesn’t buy into this rally, who do? The situation is much like what transpired in the 2015-16 Chinese stock market turbulence. According to Chart 2, during the crazy rally of A shares from June 2014 to June 2015, the net capital flow (rolling 12 months) of China started to drop very quickly and turn negative in late 2014 for the first time since the data was collected. The hot money was flowing out of China at its highest speed, which is the total opposite of what happened in the previous rallies of A shares. According to Bloomberg, China suffered capital outflow of $1 trillion in 2015. Hot money didn’t buy into the crazy Rally, and it was Chinese Damas that were left holding the bags and suffered the heaviest loss in the end.

Chart 2

CNNMFMRS: China Net Capital Flow(rolling 12 months), SHCOMP: Shanghai Stock Exchange Composite Index, Source: Bloomberg

The examples among the institutional money, which do not buy into this housing market rally are plenty. Let me count two of the biggest: Wanda and Anbang. Before 2015, Wanda Group invested totally $15 billion overseas, and in 2016, it invested $10 billion outside China so far. Since 2014, Anbang Insurance group has invested a hefty sum of $13.5 billion overseas. Wanda Group is one of the biggest real estate developers in China. The insurance industry which Anbang Insurance group belongs to is one of the most important funding sources for the housing sector. Now the biggest names among the institutional money who once were the biggest patrons of the property market, are moving their assets overseas on an unprecedented scale. This is one of the most fundamental reason why the YoY growth rate of “Completed Investment in Real Estate Development” stays at its historical lows during this housing market rally.

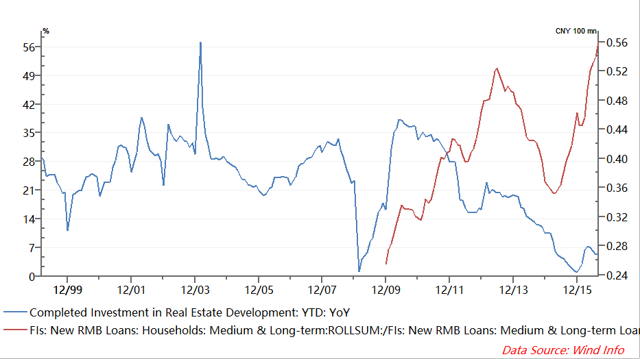

The trend couldn’t be clearer: The current market rally is the strongest one in the 18 years of China real property bull market. However, to the opposite of what happened in previous rallies, this time the institutional money is flowing out of the sector, and when netting out, the capital is flowing out of China as a whole at a speed unprecedented since “Reform & Opening up“. While the institutional money is abandoning the sector, who is fueling the rally? Let’s look at the chart below:

Chart 3

Completed Investment in Real Estate Development: YTD: YoY<Blue Line, Left Axis>, FIs: New RMB Loans: Households: Medium & Long-term (ROLLing 12 months)/FIs: New RMB Loans: Medium & Long-term Loans (ROLLing 12 months)< RedLine, Right Axis> Data Source: Wind Info

Be aware that the majority of “New RMB Loans: Households: Medium & Long-term” is home mortgage.

According to Chart 3, ever since ” New RMB Loans” data was collected from Dec 2009, ” New RMB Loans: Households: Medium & Long-term (ROLLing 12 months)/FIs: New RMB Loans: Medium & Long-term Loans (ROLLing 12 months)” almost moved in tandem with” Completed Investment in Real Estate Development: YTD: YoY“, which indicates that the institutional money and Chinese Damas almost leveraged up in line with each other in all the previous housing market rally.

The current rally is an exception: “New RMB Loans: Households: Medium & Long-term (ROLLing 12 months)/FIs: New RMB Loans: Medium & Long-term Loans (ROLLing 12 months)” rises up with unprecedented speed while ” Completed Investment in Real Estate Development: YTD: YoY” languishes at the historical lows.

The institutional money is abandoning the housing sector and reducing its respective leverages, and meanwhile Chinese Damas are leveraging up at the unprecedented speed. So it is the financial truth of the destocking of China’s property market.

3.Chinese Damas nearly run out of room to grow more leverage

This April, about 77% of “FIs: New RMB Loans: Medium & Long-term Loans” are home mortgages—close to the previous record number: 81%; this May, the YoY growth rate of the home price in the First-tier Cities arrived at 26.36%–a new record. Even more shockingly, in July, nearly all of “FIs: New RMB Loans: Medium & Long-term Loans” are home mortgages. The current housing market rally is entirely fueled by the Chinese Dama’s unprecedented leverages. How much further can Chinese Dama’s leverages go?

W e should also be aware that on the one hand, Chinese Damas are heavily restricted to exchange their RMB for dollars and shift their dollars aboard, and they end up buying up houses feverishly; on the other hand, the institutional money moguls are a privileged bunch who can easily exchange their rmb for billions of dollars and shift their assets aboard on a massive scale, and they end up reducing their exposures to China’s housing market substantially. Similar situations happened in the previous crazy rally of A shares as well.

According to Bloomberg, during the super strong rally and subsequent crash of A shares in 2015, the annual tally of China’s capital outflows reached 1 trillion dollars. In this regard, China’s housing market is not much different from A shares. There are all asset bubbles insanely leveraged up by Chinese Damas, which allow institution money to cash out.

In the casino that is China’s housing market, the institutional money has drastically cut down its exposures, and move its assets aboard on a massive scale; the local governments use the Local Debt Swap Program and the record number of “land kings” transactions to cash out and reduce their respective leverages; and there are only highly leveraged up Chinese Damas left holding the bag. So the question is how much further can Chinese Damas’ leverages go?

Let’s see the below data from Economist Jiang Chao of Haitong Securities:

When looking at the balance of total home mortgage and taking into account Housing Provident Fund, the average debt-to-income ratio of Chinese mortgage takers is close to 50% which is close to the level of the US before the subprime mortgage crisis. The new home mortgage/GDP ratio is also close to the historical high of the US.

There’s really no much room for Chinese Damas’ leverages to grow substantially further. Right when Chinese Damas’ leverages nearly get out of hand, Local governments in China announced a flurry of property market cooling measures, many of which are the strictest in the history. The situation is reminiscent of last April when China’s financial authorities started to crack down shadow lending in the stock market.

According to my prediction, if the government stands aside, China’s housing market will reach its secular peak around the first half of the year 2017 and very likely enter a violent downward correction.

The property market cooling measures will drastically reduce the number of potential house buyers who meet governments’ criterions and slow down the growth of home mortgages. The government want the house prices of the First-tier and second–tier Cities to move sideways on the current high levels, and therefore force the money towards the housing market of the third-tier and fourth–tier Cities. That way, the destocking of property market could be carried out across the whole country.

The local governments and institutional money across the country thus can decrease their exposures and leverages related to the property market, while the Chinese Damas are left holding the bag with really high leverages. If the housing market collapses, local governments and institutional money (central enterprises, state enterprises, privileged enterprises, and banks etc.) will be able to avoid as much damages as possible while the fortune of Chinese Damas will be dealt the deadly blow. So it is the ugly truth of the destocking of property market to help local governments and institutional money deleverage with Chinese Damas’ leverages greatly increasing.

4. Prediction when China’s housing market bubble will burst

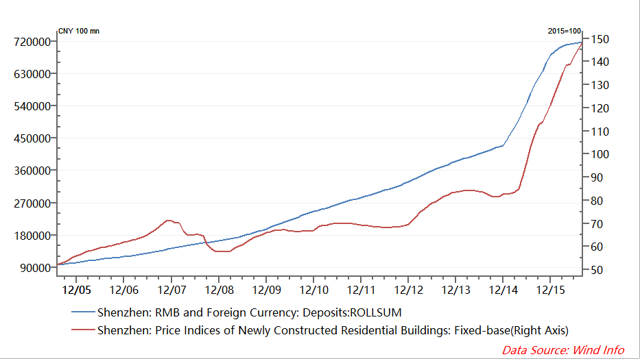

Chart 4

According to chart 4, since July 2005 when the data “Shenzhen: Price Indices of Newly Constructed Residential Buildings: Fixed-base” was first available, the variable of “Shenzhen: RMB and Foreign Currency: Deposits (rolling 12 months)” has been highly correlated to the variable of Shenzhen: Price Indices of Newly Constructed Residential Buildings: Fixed-base, the correlation coefficient of which is 0.94.

Since Dec 2014, the variable of “Shenzhen: RMB and Foreign Currency: Deposits (rolling 12 months)” has gone up super-exponentially, obeying a power law increase. Running its data series through the Log-Periodic Power Law (LPPL) model, we can predict the YoY growth rate of “Shenzhen: RMB and Foreign Currency: Deposits (rolling 12 months)” will collapse around this December, and six months later around June 2017, “Shenzhen: Price Indices of Newly Constructed Residential Buildings: Fixed-base” will reach its secular peak and afterwards very likely enter a violent downward correction.

Taking into account the government’s manipulation and intervention, I made some adjustment to my prediction. My final prediction is the house price of Shenzhen will reach its secular peak in around August 2017 (the difference between the actual time and my predicted time is less than 10 months) and afterward will very likely enter a violent downward correction. Since the house price of Shanghai is highly correlated to that of Shenzhen, the house price of Shanghai will reach its secular peak in around August 2017 (the difference between the actual time and my predicted time is less than 10 months) and afterward very likely enter a violent downward correction as well. The home prices in China’s housing market will reach its secular peak in around the second half of 2017 (the difference between the actual time and my predicted time is less than 10 months) and afterward very likely enter a violent downward correction.

5.When it comes to leverage, China’s housing market is just like A shares

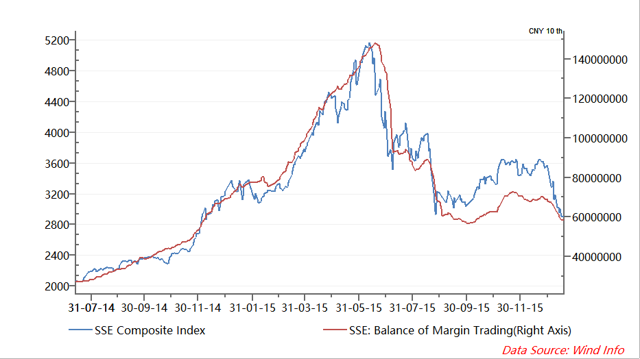

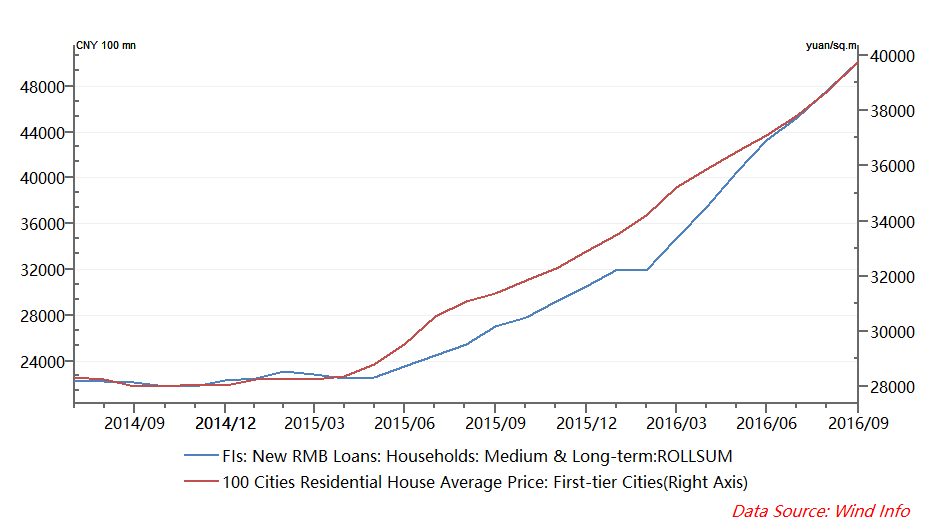

Let’s look at the 2 charts below:

Chart 5

Chart 6

According to Chart 5, fromJuly 2014 when A shares started its previous rally to January 2016 when A shares found its bottom, “SSE Composite Index” had been highly correlated to “SSE: Balance of Margin Trading”, the correlation coefficient of which is about 0.95.

According to chart 6, from July 2014 when the home price in the First-tier Cities started to move sideways to consolidate its previous bottom to present days, “FIs: New RMB Loans: Households: Medium & Long-term (ROLLing 12 months)” has been highly correlated to “100 Cities Residential House Average Price: First-tier Cities”, the correlation coefficient of which is about 0.98.

When it comes to the leverages-especially Chinese damas’ leverage, China’s housing market is just like A shares. It is also highly alarming that shadow landing plays a critical role in both market rallies in A shares and China’s housing market. Chinese home buyers are borrowing massive amounts of money to pay for down payments through the country’s hard-to-track shadow banking system. It is possible for someone with no savings at all to take out a mortgage in China.

Property developers, real estate agencies, and internet peer-to-peer lenders are active in this highly leveraged market, and they sell the loans as wealth-management products, to millions of individual investors in China. This is the Subprime mortgage of Chinese characteristics. The previous crazy rally of A shares had its notorious umbrella trust from shadow banks, and now the current insane rally of China’s housing market has its subprime mortgage offerings from shadow banks. It looks highly likely the history will repeat itself again.

In around the second half of 2017 (the difference between the actual time and my predicted time is less than 10 months), China’s housing market will enter its secular bear market. Considering the very high leverage, the process could be very forceful. It will be reminiscent of the massive market crash of A shares in 2015. China’s foreign reserve will face massive drawdowns. Its capital outflow will be really huge. In 2015 when China’s stock market crash, the tally of capital outflow that year is $1 trillion. When China’s housing market forcefully unwinds its leverages in around the second half of 2017(the difference between the actual time and my predicted time is less than 10 months), the situation will be much worse. RMB will probably be devalued by around 10% next year.

China’s Mount Vesuvius, its insanely leveraged housing market, will be erupting.