from the Dallas Fed

Positive signs are continuing for the Texas oil and gas sector. Prices for West Texas Intermediate (WTI) crude oil rose in November. Texas oil and gas employment expanded further in October, marking nine consecutive months of increases.

Rig counts in the Permian Basin reached the highest level in over two years. Total U.S. liquefied natural gas (LNG) exports reached an all-time high in November.

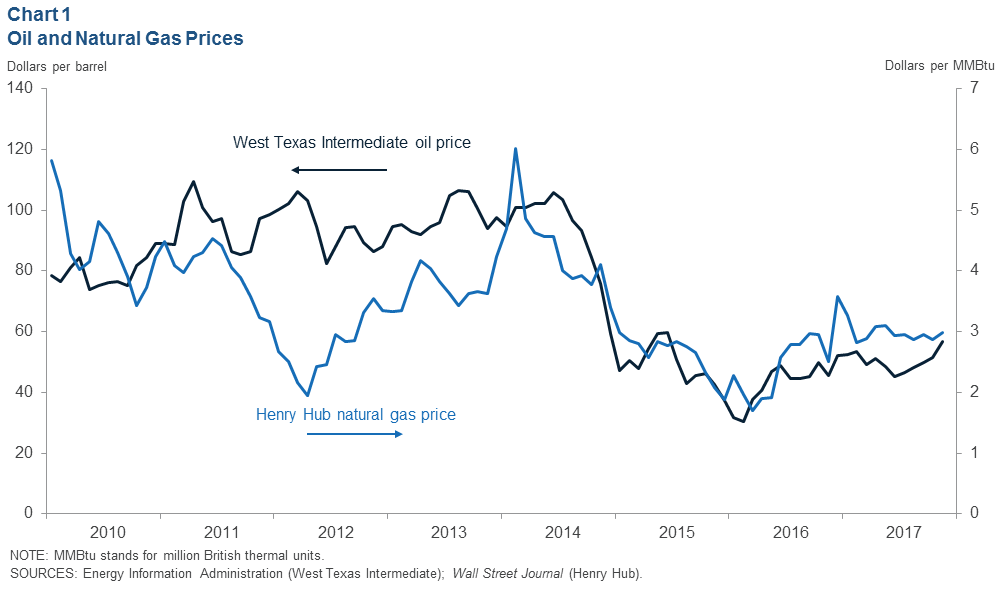

Oil and Natural Gas Prices

The average WTI spot price increased to $56.64 per barrel in November from $51.58 in October, the highest level in over two years (Chart 1). On Nov. 30, members of OPEC agreed to extend the production cuts until the end of 2018, with strong support from both Russia and Saudi Arabia. The extension, coupled with recent geopolitical tensions in the Middle East as well as continuing signs of drawdowns in Organization for Economic Cooperation and Development global inventories, supported the upward price movement.

Henry Hub natural gas prices were $2.99 per million British thermal units (MMBtu) in November, compared with $2.87 in October. Heating degree days for November were 6 percent below the 10-year average, likely placing a lid on prices under $3 per MMBtu even though U.S. natural gas inventories are below the five-year average, and U.S. LNG exports are at an all-time high.

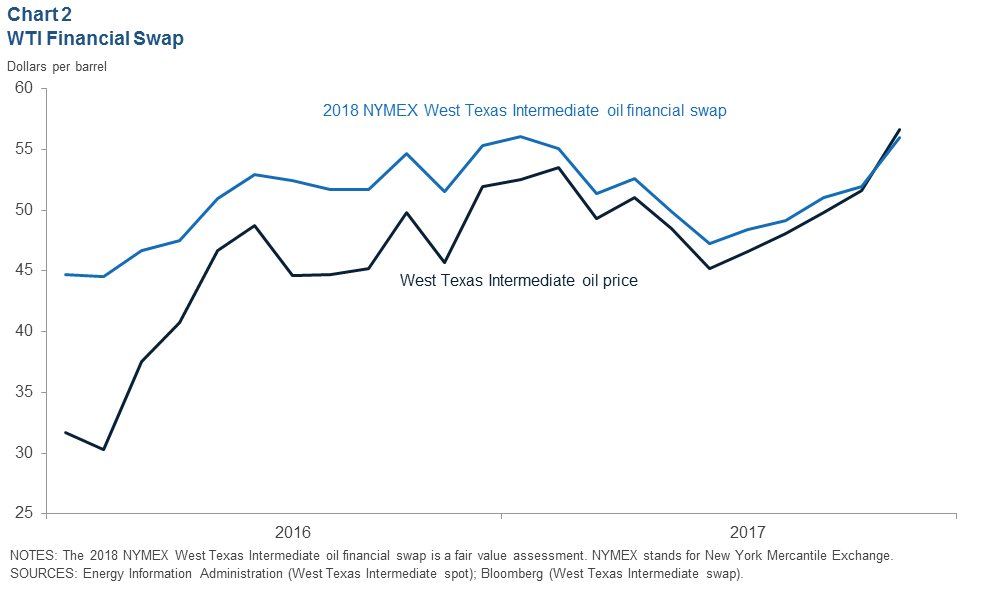

WTI Financial Swap

The 2018 WTI crude oil financial swap increased to $55.94 per barrel in November from $51.97 in October (Chart 2). The WTI swap has gone up by $9 per barrel since June, making it more attractive for producers to lock in prices for future production. In line with the increase, a variety of external reports point to greater producer hedging activity in recent months.

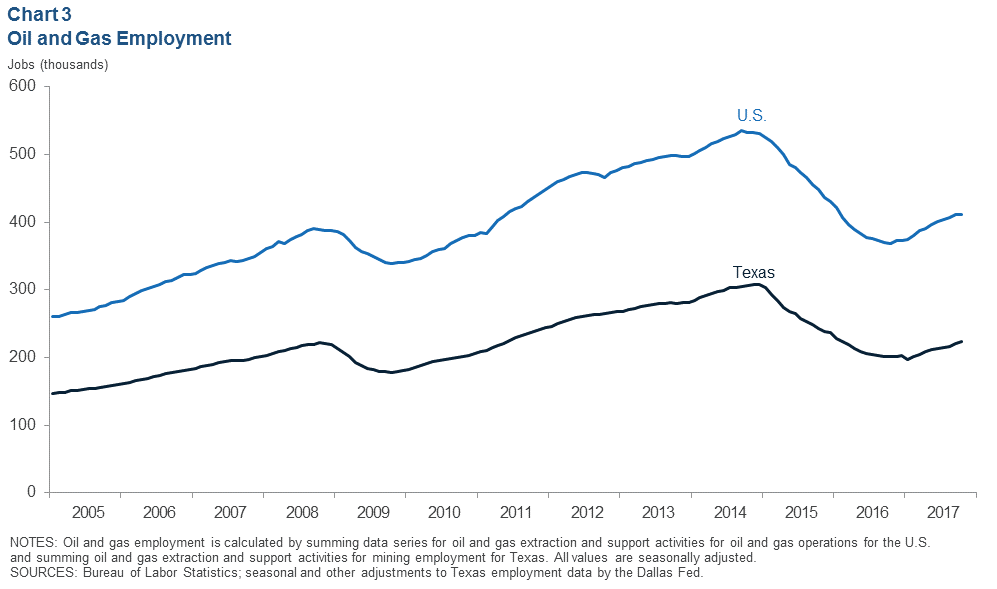

Oil and Gas Employment

Texas oil and gas employment expanded in October by 3,200 jobs to roughly 223,300 (Chart 3). Support activities for mining added 2,500 jobs, and payrolls in oil and gas extraction increased by 700. U.S. oil and gas employment stood at 411,000 in October, with Texas accounting for 54 percent of the total.

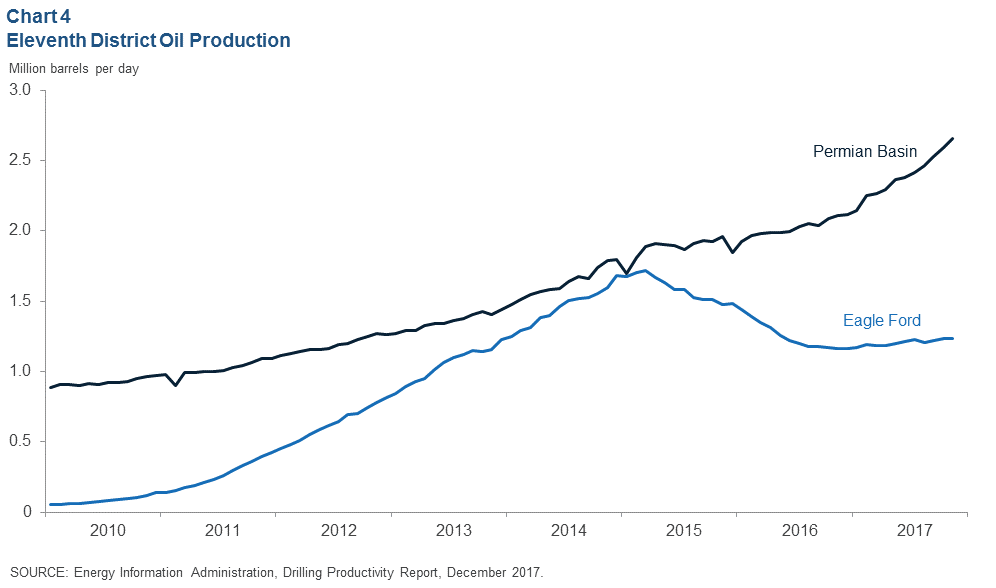

Eleventh District Oil Production

Permian Basin production rose in November by 67,800 barrels per day (b/d) to 2.66 million, and Eagle Ford production was up 5,200 b/d to 1.24 million (Chart 4). While Permian production has grown strongly for the past 12 months, Eagle Ford production has only edged up. The Enterprise Products Partners’ 450,000 b/d Midland-to-Sealy pipeline is nearing completion, which should help support production growth in the Permian as it will provide additional takeaway capacity.

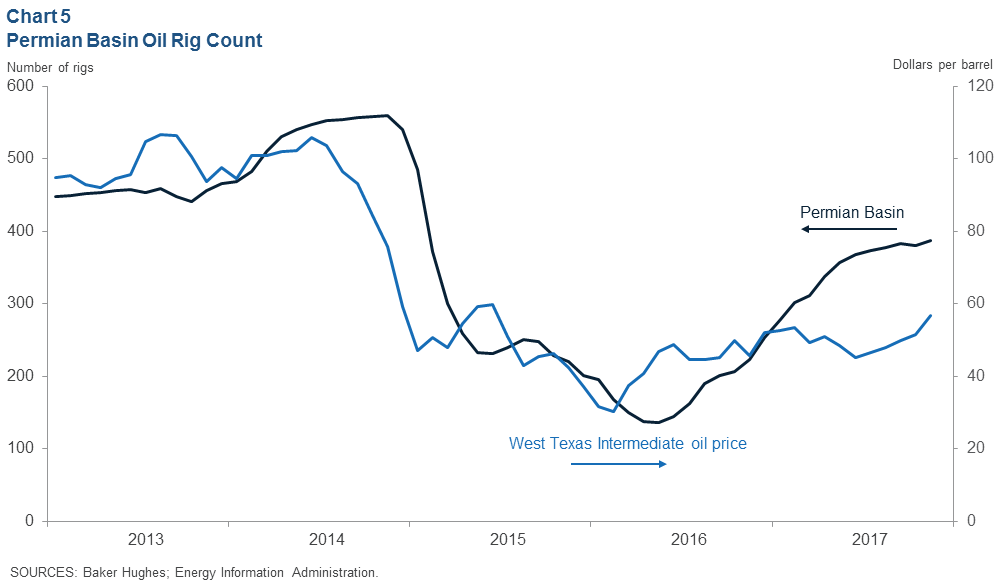

Permian Basin Rigs

Oil-directed rig counts in the Permian Basin increased from 381 in October to 388 in November, the highest level since January 2015 (Chart 5). Despite showing signs of plateauing in September and October, rig counts in the Permian have continued to rise with increases in WTI prices. Higher rig counts have translated into higher production, with the Permian Basin growing by 0.5 million b/d over the past 12 months.

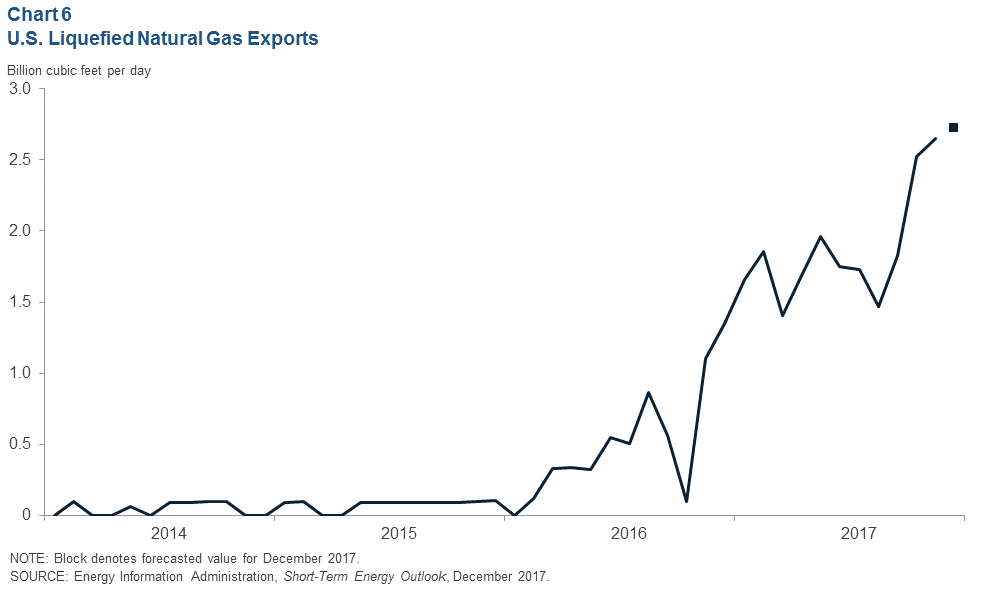

LNG Exports

U.S. LNG exports rose to 2.7 billion cubic feet per day (bcf/d) in November from 2.5 bcf/d in October, marking an all-time high (Chart 6). Given 2.8 bcf/d of current natural gas liquefaction capacity, U.S. LNG facilities are being highly utilized to meet global winter heating demand. The Energy Information Administration projects that natural gas liquefaction capacity will more than triple to 9.6 bcf/d by the end of 2019, which will help facilitate U.S. LNG exports going forward.

Additional charts of interest can be found in the Dallas Fed’s monthly energy slideshow.

Source

https://www.dallasfed.org/research/energy/indicators/en1712.aspx