from the St Louis Fed

A new public database helps reveal stark disparities in consumer credit in low- and-moderate-income (LMI) neighborhoods across U.S. metro areas, according to a recent article in Bridges.

In the article, Michael Eggleston, a senior community development specialist at the Federal Reserve Bank of St. Louis, examined data related to LMI neighborhoods in more than 200 metropolitan statistical areas (MSAs). An LMI neighborhood is an area where the median income is less than 80 percent of the median income in the associated MSA.

Significant Differences in Credit Profiles

Using the Consumer Credit Explorer (CCE),1 Eggleston found that the credit profiles of residents in LMI neighborhoods varied greatly among different metro areas.

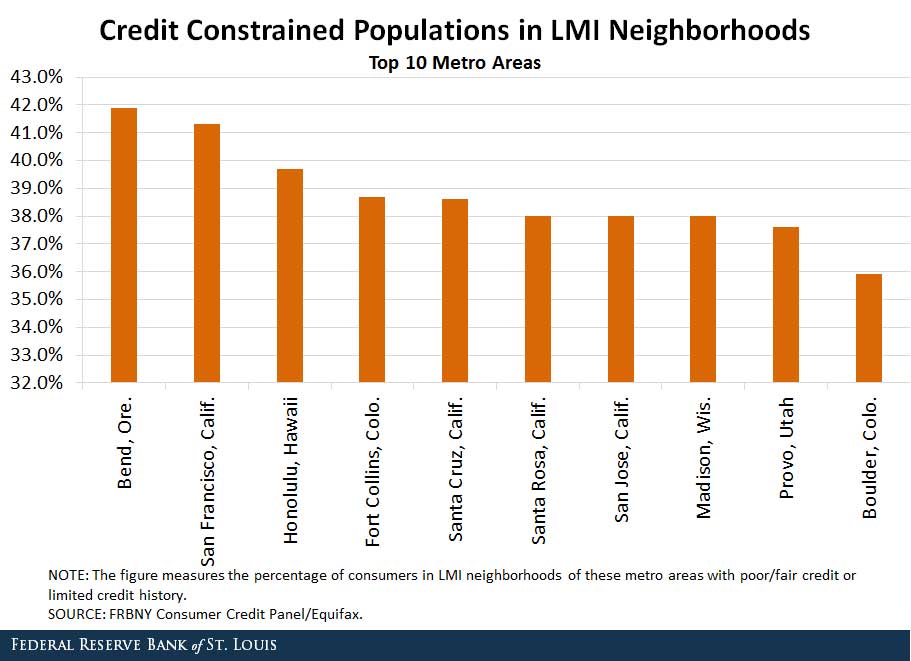

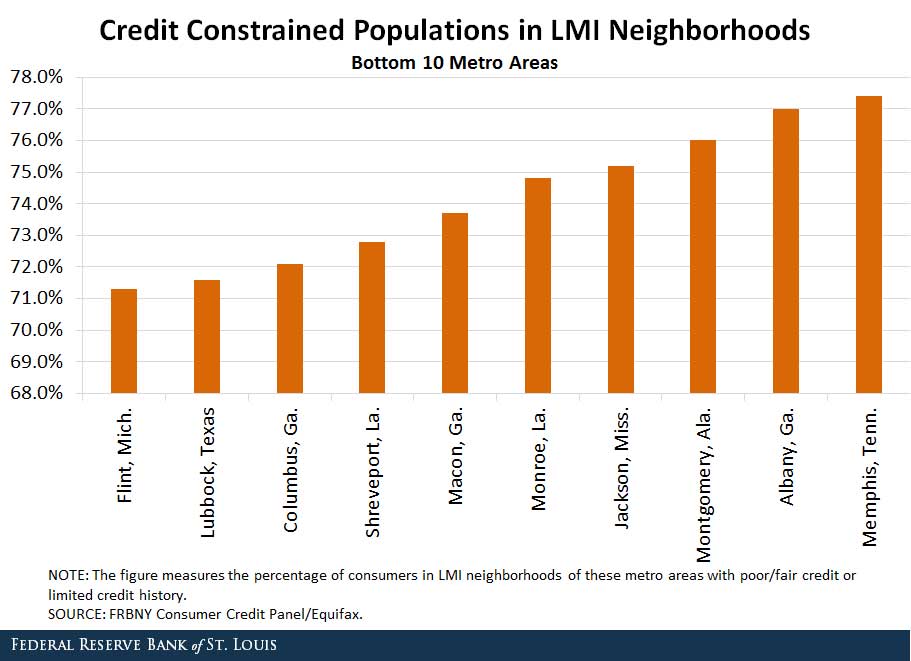

Boulder, Colo., is on one end of the spectrum. Only 35.9 percent of consumers in that metro area’s LMI neighborhoods were credit constrained, which is defined by the CCE as having poor/fair credit or limited credit history. On the other end of the spectrum is Memphis, Tenn., where 77.4 percent of the consumers in LMI neighborhoods were credit constrained. The figures below show the top 10 and bottom 10 metro areas in terms of credit constrained residents in LMI neighborhoods.

Eggleston found that LMI neighborhoods with relatively better credit tend to be in metros with a larger percentage of white residents, and they are typically found in the East, West and parts of the upper Midwest. They also tend to be in metros that have lower poverty rates.

On the other hand, metros in which LMI neighborhoods have poorer credit tend to be in the South and have larger shares of African-American residents. They also tend to have relatively high poverty rates.

Among the 10 MSAs in which people living in LMI neighborhoods have the poorest credit, the average poverty rate is 68 percent higher than the average poverty rate of the 10 MSAs in which people living in LMI neighborhoods have the best credit.

Implications of Disparities in Credit

Eggleston noted that this disparity in credit has implications for residents in these LMI neighborhoods. A good credit profile can be an important factor in determining an individual’s ability to get a car loan, rent an apartment or secure a job.

“In short, good credit can signify whether an individual’s financial situation is on the right track,” Eggleston wrote. “This can be particularly powerful for someone living in an LMI neighborhood where opportunities to improve their situation can be scarce and hope can feel far off in the distance.”

He also noted that the disparity may have implications for regulated financial institutions that serve LMI neighborhoods because of certain obligations under the Community Reinvestment Act (CRA).

Currently, the credit profile of an area served by a bank isn’t taken into consideration when determining whether the bank is meeting its CRA obligations. The disparity, however, “raises some important questions about the appropriate role of the CRA in promoting fair and impartial access to credit in underserved communities,” Eggleston wrote.

Notes and References

1 The Consumer Credit Explorer provides Federal Reserve Bank of New York Consumer Credit Panel/Equifax data, tabulated by the Federal Reserve Banks of Philadelphia and Minneapolis.

Additional Resources

Bridges: All Low- and Moderate-Income Areas Are Not Created Equal

On the Economy: How Do Incomes in the Largest Cities Compare?

On the Economy: What Issues Do Low- and Moderate-Income Households and Communities Face?

Source

https://www.stlouisfed.org/on-the-economy/2016/november/uncovering-credit-disparities-low-moderate-income-areas

Disclaimer

Views expressed are not necessarily those of the Federal Reserve Bank of St. Louis or of the Federal Reserve System.