Written by Lance Roberts, Clarity Financial

I am traveling this week with my family for our annual “year-end” ski trip. I am working on a laptop so I won’t be able to update some of the weekly market stat reports, but I did want to pen a few paragraphs on the market as we move into the last two trading days of the decade. I promise the full version of the newsletter will return next week.

Please share this article – Go to very top of page, right hand side, for social media buttons.

I want to start with the quote from last week’s missive only because it is so apropos:

“We are so overbought, and this is feeling like a panicky-just-get-me-in buy day. Be careful about being impressed.” – Kevin Muir

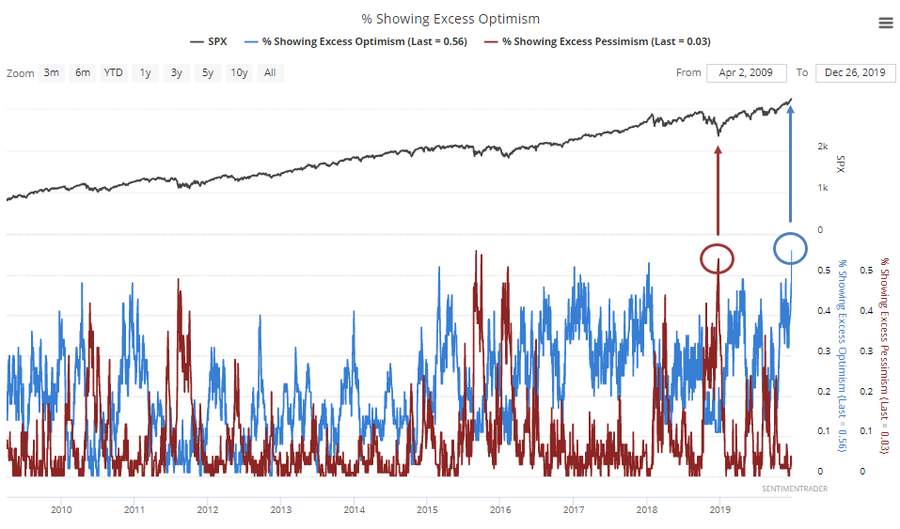

That remains the case again this week as investor optimism has surged to record highs. As noted by Sentiment Trader, this is a marked reversal from just 1-year ago as sentiment plumbed more extreme lows.

Of course, this reversal in optimism should not be a surprise. My pal Victor Adair at Polar Futures group explains this well.

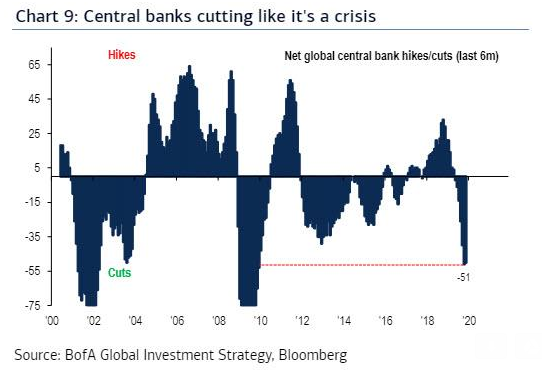

“The most important message from the financial markets in 2019 was, ‘Don’t Fight The Fed.’ The 180 degree turn in Federal Reserve policy…the Powell Pivot…caused markets to realized that it was, once again, ‘All About The Central Banks.’

In December 2018 the Fed raised interest rates and indicated that they expected to be raising rates in 2019…but instead of raising rates they cut rates three times…stopped their quantitative tightening policies and wrapped up 2019 by pumping vast amounts of liquidity into the market.

The Fed’s policy reversal inspired Central Banks around the world to step up their own monetary stimulus programs. That global shift to easier monetary policy may or may not have kept the world economy from slipping into recession in 2019…but it certainly helped drive global stock and bond markets to big gains. Bond yields hit All Time Lows, the ‘stack’ of negative yielding bonds soared to a high of ~$17 Trillion and major stock indices kept making ‘New All Time Highs.'”

As I penned last week:

“This stimulus is the largest ever outside of a ‘recession’ or ‘financial crisis,’ which should lead to the obvious question of ‘what exactly is going on we don’t know about?'”

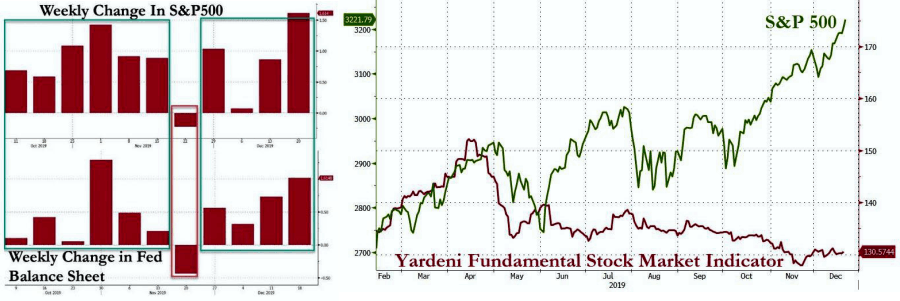

This surge of liquidity is the reason for the markets surge over the last 3-months and was the crux of Friday’s “Morning Market Commentary” which was provided to our RIAPRO subscribers:

“While the media has continued to use the same straw man of trade optimism to justify the rally whatever trade agreement there may actually be was priced in long ago.

The reality is that the Fed’s $500 billion flush of liquidity into year-end to meet short-term funding needs has been interpreted by the markets at “QE.” This interpretation, and subsequent F.O.M.O, led to a rush by managers to benchmark performance and push equity allocations, and subsequently investor optimism, toward record highs.”

Sign up before the New Year using promotion code: SANTA and get a 25% discount for the first 90-days.

This message hasn’t changed over the last week:

“While the Federal Reserve accurately states this is NOT ‘Quantitative Easing,’ apparently market participants didn’t get the memo. The market has risen in every single week the Fed has been active, despite collapsing fundamentals. (h/t ZeroHedge)”

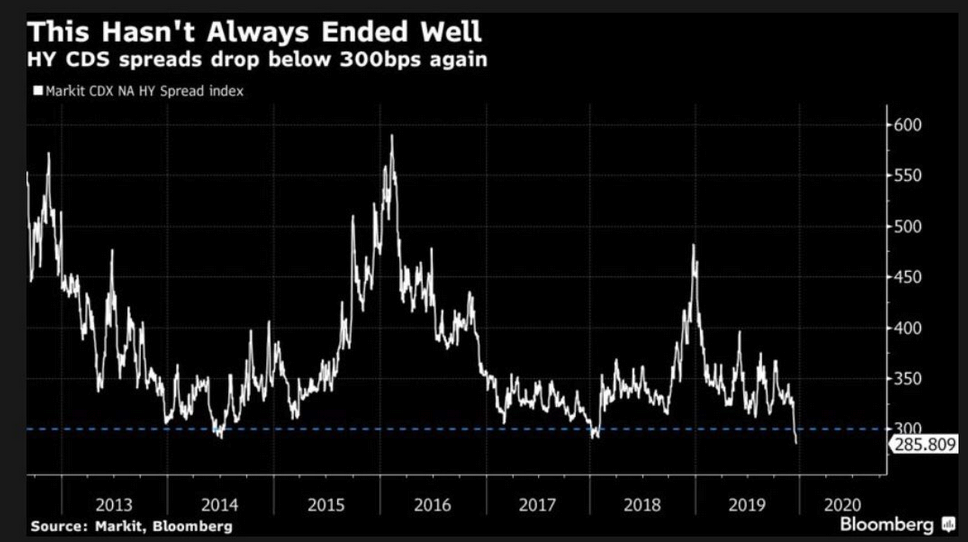

Speaking of optimism, and outright complacency, the difference (spread) between the high yield (junk debt) CDX index and U.S. Treasury yields has fallen back below 300 basis points. The index measures the cost of insuring high yield debt against default. This extremely low cost of insurance, especially this far into an economic expansion, reeks of complacency and a chase for extra yield as we are seeing in other asset markets.