Written by Lance Roberts, Clarity Financial

I have a couple of thoughts on market drivers these past two weeks:

Please share this article – Go to very top of page, right hand side, for social media buttons.

- While the market popped a week ago Thursday due to a perceived “trade deal” between Trump and Juncker, there was no deal really. There was a lot of hand shaking, back slapping and talk – but nothing of substance came from the meeting. At best, the agreement set the tables with the EU back to where they were before Trump manufactured the whole trade/tariff issue to begin with. So, I guess you can credit Trump for effectively solving the problem he created to start with, but not much more than that. Expect trade-related issues to return to the market sooner rather than later.

- We remain underweight industrials, materials, emerging and international markets.

- Amazon ($AMZN) had a blow out quarter for earnings which was a good thing given the large contribution it has made to the markets advance this year. However, while the earnings at the bottom line were fantastic it was due almost solely to a sub-3% tax rate. Had it not been for the changes to the tax law last year, it is highly likely the shortfalls in revenue would have equated to a Facebook type plunge in the shares on the following Friday versus less than a 1% gain. There is no argument the behemoth has turned the corner profitability wise, however, the huge boost to bottom line earnings from a highly-reduced tax rate will fade in the coming quarters and operating margins will again become an issue. At 286x trailing earnings and 90x projected earnings, which will likely prove to be to low, the risk of a deeper correction in the company outweighs the potential reward.

- We currently have no positions in $AMZN

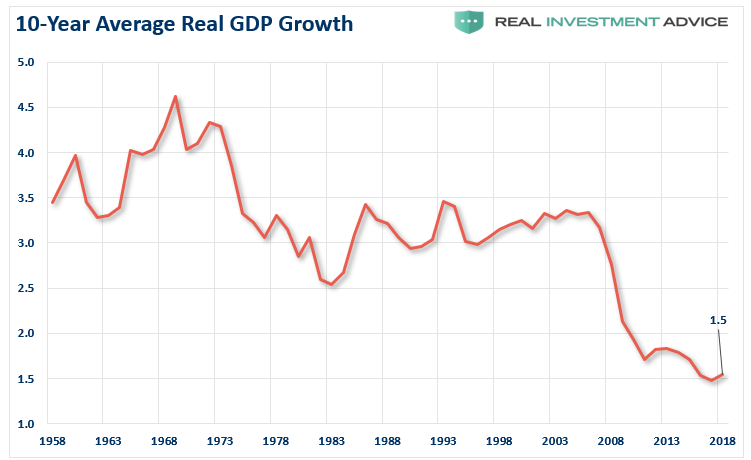

- The 4.1% GDP number left MUCH to be desired. While Trump was busy taking victory laps a week ago following the print, and making claims we could see 8 or 9% in the future, the reality is very little actually changed economically speaking. As I showed on Thursday 26 July, when I penciled in a 4% gain (I was 0.1% short on my estimate):

“Making similar adjustments for wages and productivity, we find the 5-year averages change very little. More importantly, current action is more typical of a late cycle expansion as opposed to the beginning of a new one.”

“An unusually large number of one-off factors appear to have boosted 2Q GDP, many of which are directly related to escalating trade concerns. As companies and countries race to secure supplies that may become expensive later on, exports have surged and inventories have swelled. If these trends are one-time adjustments (and our economists believe they are), the ‘payback’ in 2H could be significant. Enjoy the 2Q GDP number, which may be the last best print for a while.”

But more importantly, despite the fact the BEA just revised the trailing GDP numbers UP by almost $1 Trillion (going all the way back to 1967) Trump’s hopes are just a bit more than outlandish when you consider the 10-year trailing average of real GDP just rang in at 1.5%.

While fighting trade wars, pushing tax cuts and increasing government spending may provide short-term boosts to the economy by pulling forward future consumption – they do not address the issues which are detracting from longer-term growth.

- Debt

- Spending Hikes

- Demographics

- Surging health care costs

- Structural employment shifts

- Technological innovations

- Globalization

- Financialization

Our friends at the Committee for a Responsible Federal Budget concurred with our views on Friday stating:

“Unfortunately, even 3 percent growth is unlikely to continue over the medium and long terms. An economy cannot operate above potential capacity indefinitely, as timing shifts and the sugar high fade. And potential GDP – which grows when people work more hours, new factories and machines and software are built, and society learns how to more efficiently produce goods and services – is limited by an aging population. As we outlined in our paper How Fast Can America Grow?, population aging means lower labor force growth, less investment, and perhaps even less productivity. As a result, nearly every forecaster projects a long-term growth rate of around 2 percent per year above inflation. The Congressional Budget Office projects a rate of 1.8 percent.

(Note: there is no assumption by the CBO, or the BEA, for a recession in the next decade. This is highly unlikely to be the case and resultant GDP numbers will be disastrously worse than current projections.)

As I stated on Thursday:

“These factors (noted above) will continue to send the debt to GDP ratios to record levels. The debt, combined with these numerous challenges, will continue to weigh on economic growth, wages and standards of living into the foreseeable future.

So, while the economic report on Friday will be a “rosy” picture in the short-term, it is likely going to be the best print we see between now and the onset of the next recession.”

Seen This Before

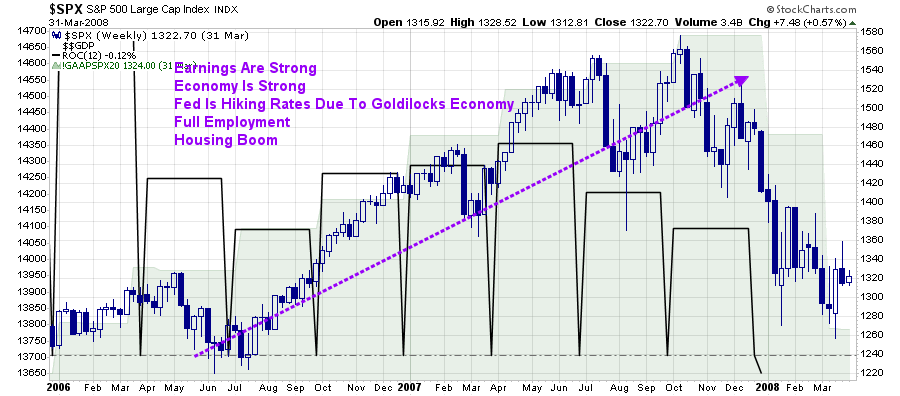

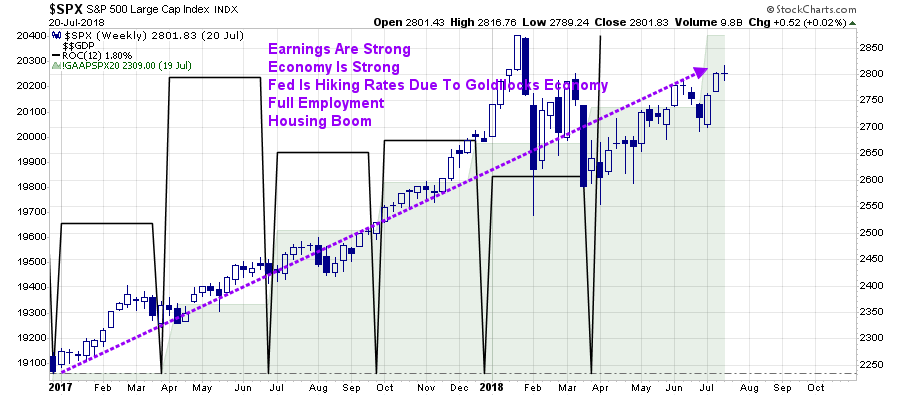

Last week, I compared charts from 2007-2008 to the 2017-present run-up. One of the biggest points being made currently for an uninterrupted bullish advance from current levels into the foreseeable future is that with earnings and economic growth strong, there is no reason for the party to end.

I have added GDP and S&P 500 valuations to those charts from last week.

In 2007, both economic growth and earnings were rising along with the market which was not surprising given the bullish exuberance of market participants at the time along with a booming housing market, excess liquidity and rising oil prices. The Fed was hiking interest rates and the “Goldilocks economy” was set to continue indefinitely. (There was no recession predicted at the time for the next decade according to the CBO/BEA)

The current environment is much the same as it was in the first half of 2007. Rising earnings and GDP, no prediction of a recession anywhere (despite a falling yield curve) and the Fed is raising rates and reducing monetary liquidity without consequence.

As I noted last week:

“From an investment management standpoint, there is absolutely ‘no doubt’ how this current evolutionary cycle in the market ends. We just don’t know the “when,” and becoming aggressively under-allocated to equity risk too soon not only impacts performance in the short-term but also subjects us, as portfolio managers, to career risk.”

However, that is a game I must play as a portfolio manager…you don’t. This is particularly if you are within 3-5 years of retirement.

Investing is not a game, or a competition, that YOU must win. There is no prize for winning but a heavy toll that will be paid for losing.

As Doug Kass noted last week:

“Investing is a complicated mosaic – making decisions on only one or two factors often leads to a dangerous journey, particularly when valuations and stock prices are elevated, when a market’s leadership seems to be narrowing and certainly with the recent emergence of a ‘two-sided market’ (from a formerly one-sided and bullish market) which often leads to a one -sided and bearish market. And, our investment world is more transparent and the transmission of news quicker and more universal than it has ever been. Communication is instantaneous and through a plethora of broadcasting and social media platforms, we are almost all armed with the same information about at the same time. It is how we interpret and analyze that information and our willingness to be open to changing data is what sets our opinion and investment performance apart.

I worship not at the altar of price momentum but rather at the altar of security analysis and margin of safety. That process provides me with a relatively concise analysis of the relationship of reward and risk.

At the core of my near-term concern are the deterioration (and worsening rate of change) in reward v. risk, the growing ambiguity of the trajectory of global economic growth, the pivot in monetary worldwide monetary policy, the likelihood of a steady move higher in short-term interest rates (and a higher risk free rate of return), evidence of a loss of any fiscal responsibility (on the part of Democrats and Republicans), expanding policy risks in part based on the behavior of our President, the possibility of a ‘Blue Wave’ in November and the evolution of a one-sided (long) market structure (and a rising role of FAANG stocks).”

While we remain long-biased in portfolios currently, Doug’s view of the risk should not go unnoticed.

It is often thought that since we openly recognize and understand prevailing risks, which may or may not come to fruition, that such means we are bearish and sitting in cash. That is never the case.

Without a thorough understanding of the prevalent risk, making an assumption of the possibilities and probabilities of a given market environment, and associated return and allocation assumptions, is impossible. In other words, without understanding the risk, you are effectively “driving with a blindfold, hoping for a positive outcome.”

Such is rarely the case over the longer-term.

We prefer to drive with our eyes open, aware of our surroundings, and arrive safely at our destination. This is particularly the case when we have passengers (clients) riding along with us.

While we are prudently aware of the risk, we are long equity and allowing the market to work for us. But, we also have a strategy and investment discipline to deal with “accident” should one occur.

Drive long enough, particularly blindfolded, and one will happen.