Written by Lance Roberts, Clarity Financial

Last week, I discussed the continuation of the “market melt-up.

Please share this article – Go to very top of page, right hand side, for social media buttons.

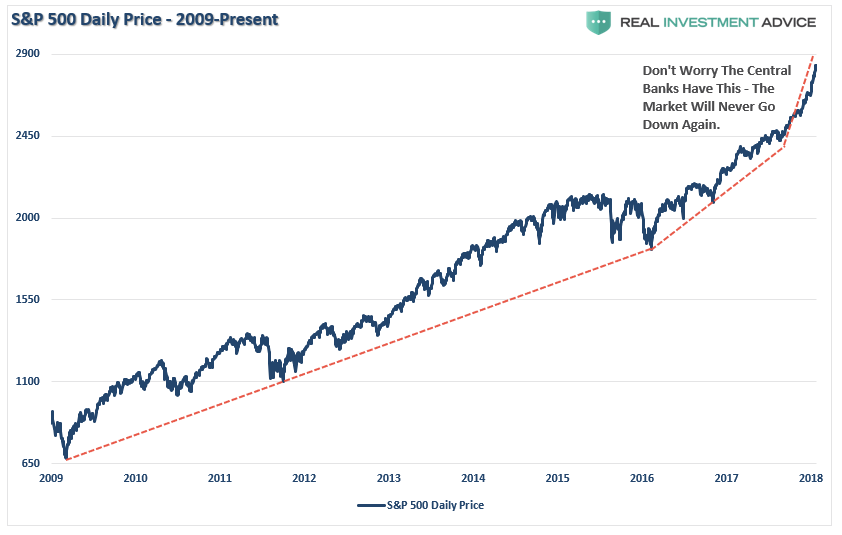

“Since the beginning of the year, the acceleration in the markets has continued unabated. As I showed yesterday, the acceleration in the S&P 500 has now gone parabolic.”

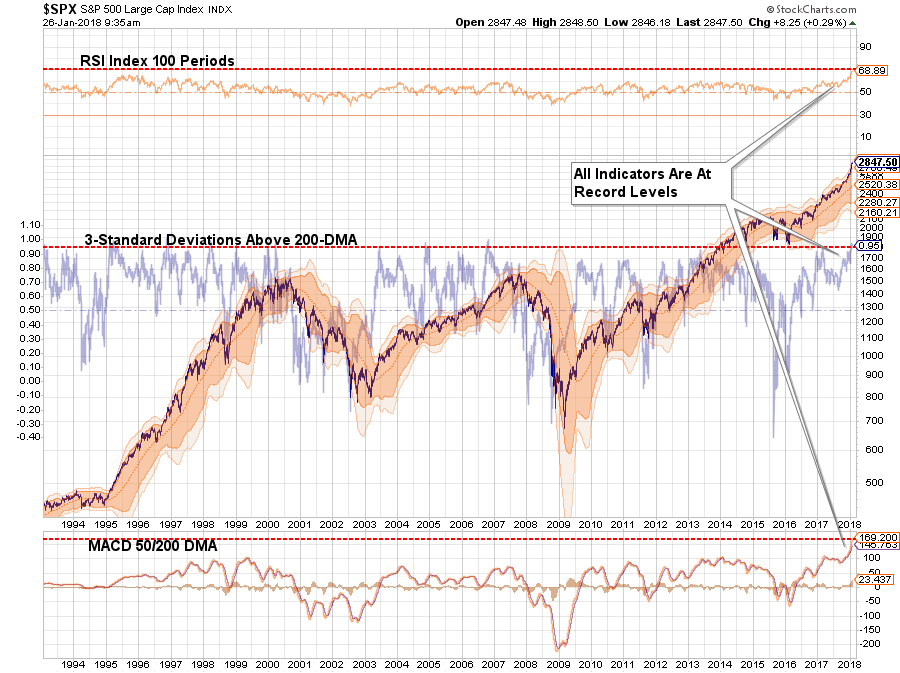

“Never before in recent history has the market been this overbought and extended from longer-term averages which suggests that a correction that reduces such conditions is highly likely in the near-term.”

Well, this past week, the market tripped “over its own feet” after prices had created a massive extension above the 50-dma as shown below. As I have previously warned, since that extension was so large, a correction just back to the moving average at this point will require nearly a -6% decline.

Econintersect note (added 05 February): The 6% decline was realized today, although the averages rebounded by market close to -4.8% for the day.

I have also repeatedly written over the last year:

“The problem is that it has been so long since investors have even seen a 2-3% correction, a correction of 5%, or more, will ‘feel’ much worse than it actually is which will lead to ’emotionally driven’ mistakes.”

The question now, of course, is do you “buy the dip” or “run for the hills?”

Don’t do either one, yet.

Yes, corrections do not “feel” good. But they are part of a “healthy” market cycle. In more normal, healthy, bullish trends corrections should be used as buying opportunities to increase exposure to equity risk in portfolios.

However, the recent parabolic acceleration in the markets heading into the New Year was neither normal or healthy. Much of it had to do with the massive liquidity injection by the Federal Reserve at the end of 2017 as shown below.

But, after the stumble this past week, it will be interesting to watch the next the Fed’s balance sheet over the next month to see if they continue with their planned $30 billion / month reduction.

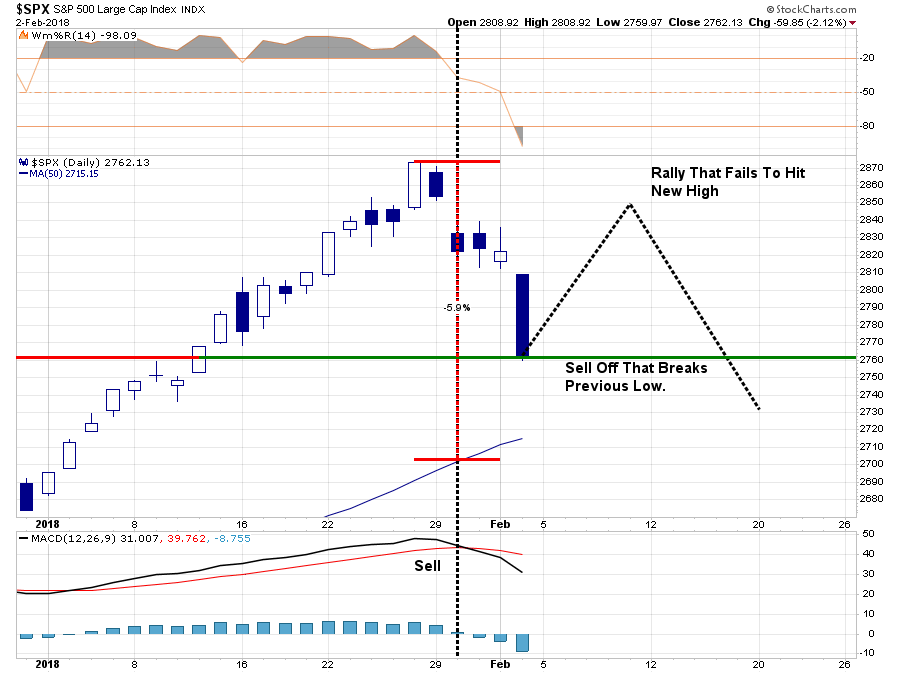

At the moment, this is the expected correction we have been discussing over the last several weeks. It is also something we had planned for by reducing overweight positions and adding a short-hedge to portfolios.

With the markets on a short-term sell signal (noted by gold vertical dashed lines in the chart above,) the current correctional process is underway and still has room to go at this juncture. But, with the market now oversold on a VERY short-term basis a rally over the next week, or so, would not be surprising.

It is the outcome of that rally that is most important to the current bull market advance.

This is what we are looking for to drive our next set of portfolio actions:

- If the market rallies back and sets a new closing high, the bullish trend will be confirmed and equity allocations will remain at target levels and hedges removed.

- If the market rallies back BUT FAILS to set a new high, a series of actions will take place.

- At the point of rally failure, portfolio hedges will be modestly increased.

- If the subsequent decline breaks the previous low, the hedges will be further increased and tactical trading long positions will be reduced.

Why is this important? We will address that in following articles over the next few days.