Written by Lance Roberts, Clarity Financial

Why I Am Buying Bonds (For A Trade)

Over the last three weeks, I have been selectively buying bonds into portfolios as opportunities have presented themselves. Importantly, I am buying ACTUAL bonds, not bond funds or ETF’s, so the rise in rates over the last week is not important to my holding period return or my return of principal.

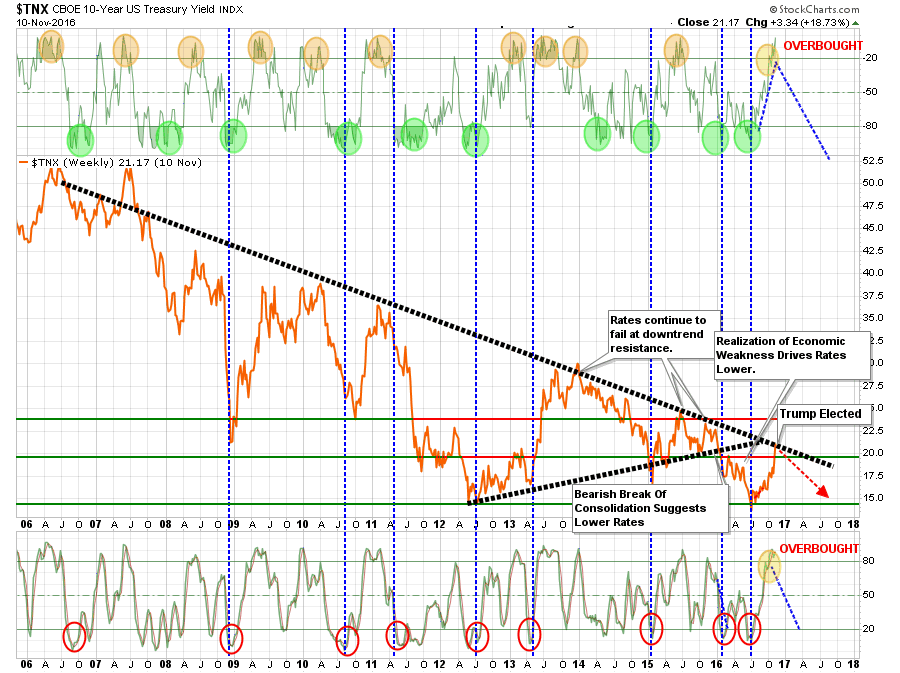

However, the spike in rates this past week, now has me buying bond ETF”s for a trading opportunity. As shown below, interest rates are now pushing overbought conditions only seen near absolute peaks in interest rates movements. (Orange circles)

What is interesting is that stock buyers are told to buy stocks after big corrections, yet it works EXACTLY the same way with bonds. When interest rates spike, bonds become VERY oversold and operate on exactly the same premises as stocks.

So, bonds are now EXTREMELY oversold and this is as good of an opportunity as one will get to buy bonds.

Does this mean rates will plunge on Monday? No. Rates could go a bit higher from here, but it will likely not be much. As Jeff Gundlach stated last week:

“I do think this rate rise is about 80% through. If yields rise beyond ‘critical resistance’ levels, including 2.35% on the 10-year note, then things are in really big trouble.”

He is right, higher rates negatively impact economic growth. But in BOTH CASES, the outcome for bonds is EXCELLENT.

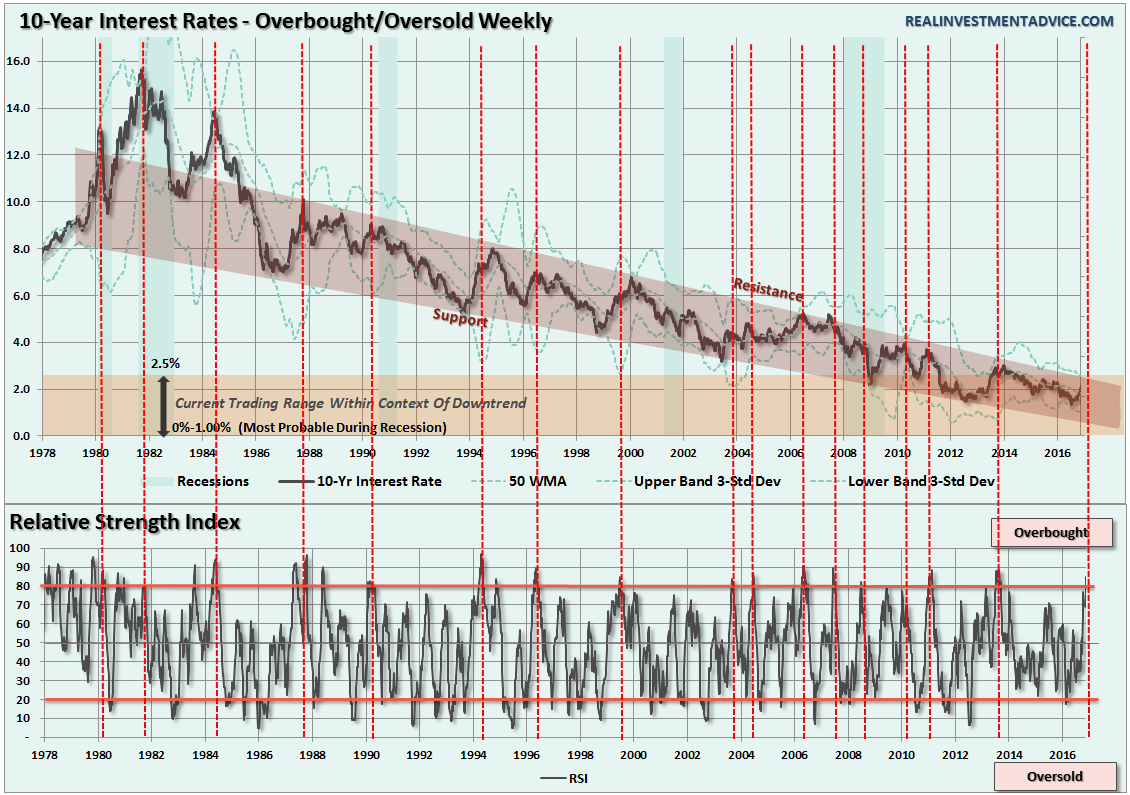

The chart below shows the long-term trend of the 10-year Treasury going back to 1978 as compared to its RSI index.

Whenever the RSI on rates has exceeded 80%, red dashed lines, it has preceded a subsequent decline in rates. In other words, overbought rates are a signal to buy oversold bonds for a potential reversion trade.

As I have repeatedly written in the past:

“While the punditry continues to push a narrative that ‘stocks are the only game in town,’ this will likely turn out to be poor advice. But such is the nature of a media driven analysis with a lack of historical experience or perspective.

From many perspectives, the real risk of the heavy equity exposure in portfolios is outweighed by the potential for further reward. The realization of ‘risk,’ when it occurs, will lead to a rapid unwinding of the markets pushing volatility higher and bond yields lower.”

“This is why I continue to acquire bonds on rallies in the markets, which suppresses bond prices, to increase portfolio income and hedge against a future market dislocation.

In other words, I get paid to hedge risk, lower portfolio volatility and protect capital. Bonds aren’t dead, in fact, they are likely going to be your best investment in the not too distant future.

In the short-term, the market could surely rise. This is a point I will not argue as investors are historically prone to chase returns until the very end. But over the intermediate to longer-term time frame, the consequences are entirely negative.

As my mom used to say: ‘It’s all fun and games until someone gets their eye put out.’”

So, yes, from a trading perspective, one of the “most unloved” asset classes to own currently – bonds.

Model Update

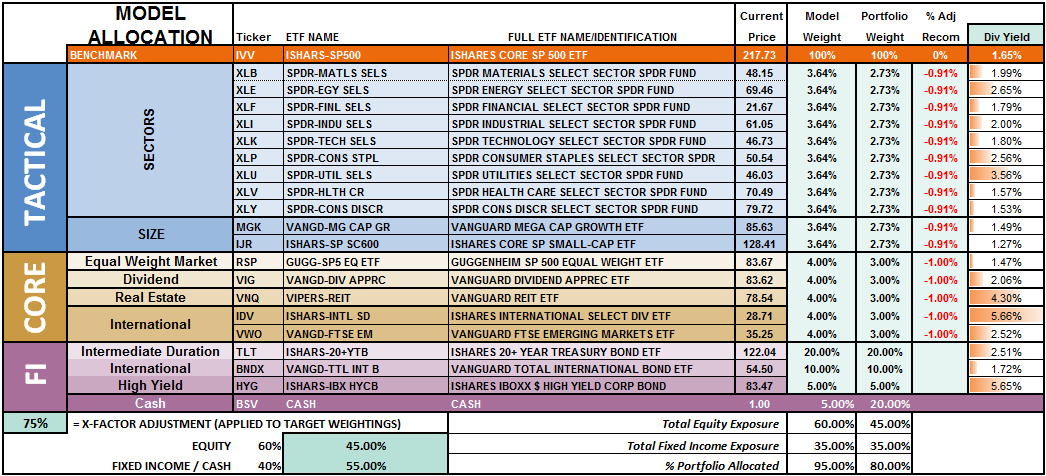

S.A.R.M. Sector Analysis & Weighting

I will update this analysis in Tuesday’s Technically Speaking post (click here for free e-delivery)

Let’s take a look at the equal weighted portfolio model.

(Note: This is an equally weighted model example and may differ from discussions of overweighting/underweighting specific sectors or holdings.)

The overall model still remains underweight target allocations. This has been due to the inability of the markets to generate a reasonable risk/reward setup to take on more aggressive equity exposure at this time.

However, the rally last week which pushed the markets back above the 50-dma keeps portfolios allocated at model weights. Provided the markets can reduce the current overbought condition, without triggering further “sell signals,” model allocations will be able to be increased for the seasonally strong period.

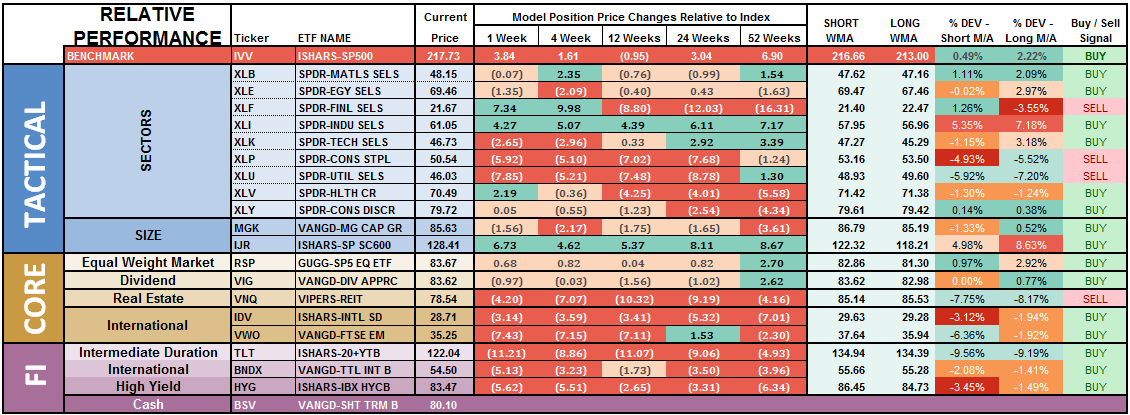

Relative performance of each sector of the model as compared to the S&P 500 is shown below. The table compares each position in the model relative to the benchmark over a 1, 4, 12, 24 and 52-week basis.

Historically speaking, sectors that are leading the markets higher continue to do so in the short-term and vice-versa. The relative improvement or weakness of each sector relative to index over time can show where money is flowing into and out of. Normally, these performance changes signal a change that last several weeks.

Notice in the next to the last column to the right, the majority of sectors which have previously been pushing extreme levels of deviation from their long-term moving average, have corrected much of those extremes. Furthermore, previously all areas were on long-term buy signals but continued weakness in the markets, combined with a loss of momentum, have eroded much of the previous strength.

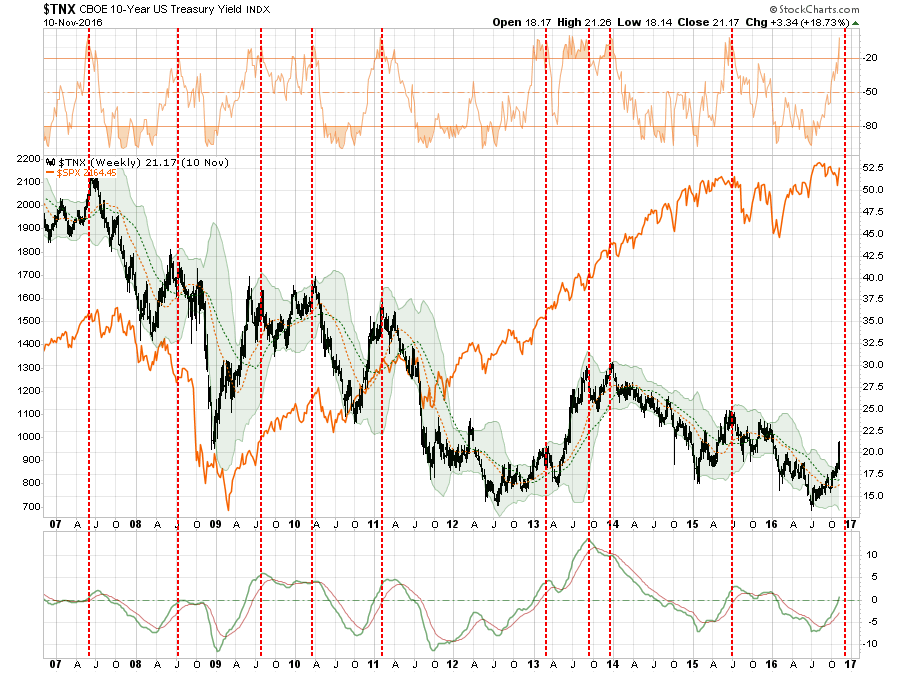

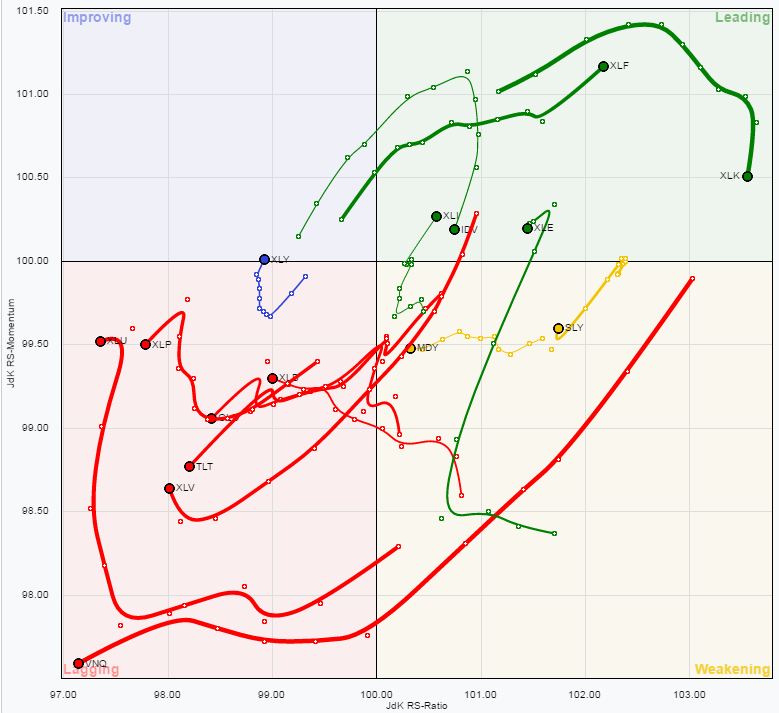

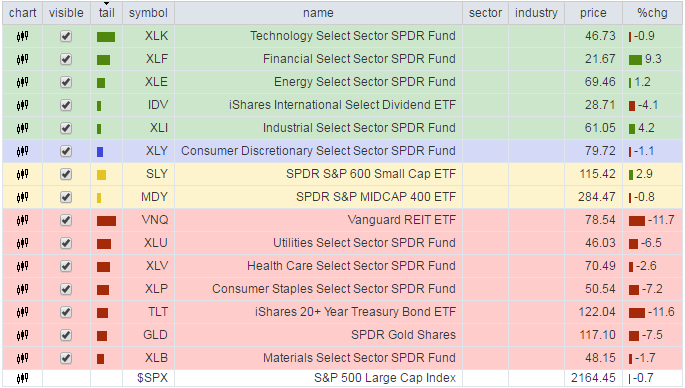

There is a broad deterioration across sector performance which suggests overall weakness in the markets will likely continue in the near-term. Some caution is currently advised as the market has now been split distinctively between the “risk on” and “safety” trade as shown below in the “spaghetti” chart, via StockCharts.

Utilities, REIT’s, Staples, Materials, Bonds, Gold, and Healthcare have remained under pressure this past week.

As I have stated over the last couple of weeks:

“With the rise in rates largely done, sectors with the most benefit from falling rates look reasonable.”

The opposite holds true for those sectors that are adversely affected by a stronger dollar and weaker oil prices. With dollar tailwind still intact, and oil prices grossly extended, profit taking in Small-Cap, Mid-Cap, Emerging Markets, International and Energy stocks seems logical. This recommendation remains from the last couple of weeks and remains salient. “

While the rise in rates this past week due to the unexpected victory by Donald Trump in the Presidential election, it has only served to reinforce positioning in lagging areas of the market for a “reversion” trade over the next few weeks.

Also, as I stated last week:

“Lastly, given that a bulk of the sectors remain either in weakening or lagging sectors, this suggests the current advance in the market remains on relatively weak footing.

I have been recommending taking profits in the Technology sector. This was due to the extreme levels of outperformance of that sector which has begun to fade. The rotation out of technology is likely not complete yet and brings into focus extremely oversold sectors such as Health Care, Utilities and Staples as potential candidates.”

That advice remains this week as well.

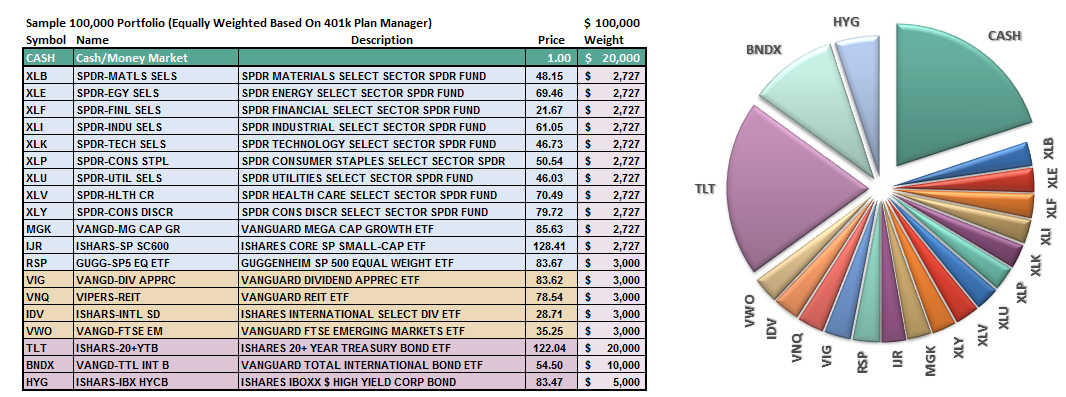

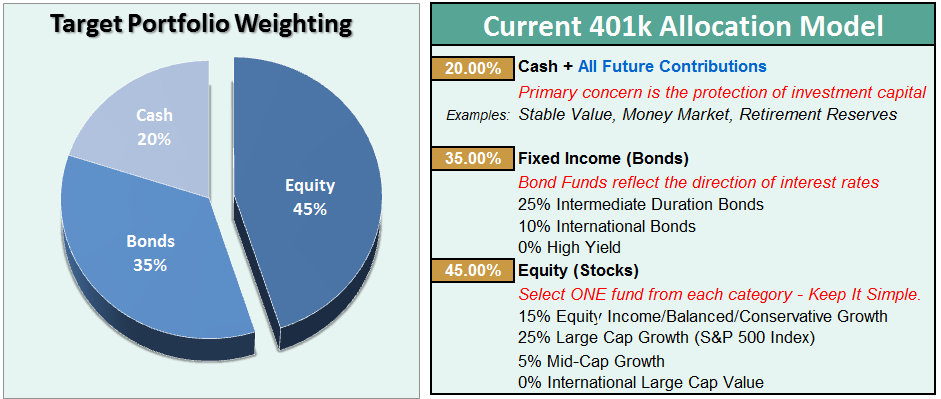

The risk-adjusted equally weighted model has been increased to 75%. However, the markets need to break above the previous consolidation range to remove resistance to a further advance.

Such an increase will change model allocations to:

20% Cash

35% Bonds

45% in Equities.

As always, this is just a guide, not a recommendation. It is completely OKAY if your current allocation to cash is different based on your personal risk tolerance, time frames, and goals.

For longer-term investors, we still need to see improvement in the fundamental and economic backdrop to support the resumption of a long-term bullish trend. Currently, there is no evidence of that occurring.

THE REAL 401k PLAN MANAGER

The Real 401k Plan Manager – A Conservative Strategy For Long-Term Investors

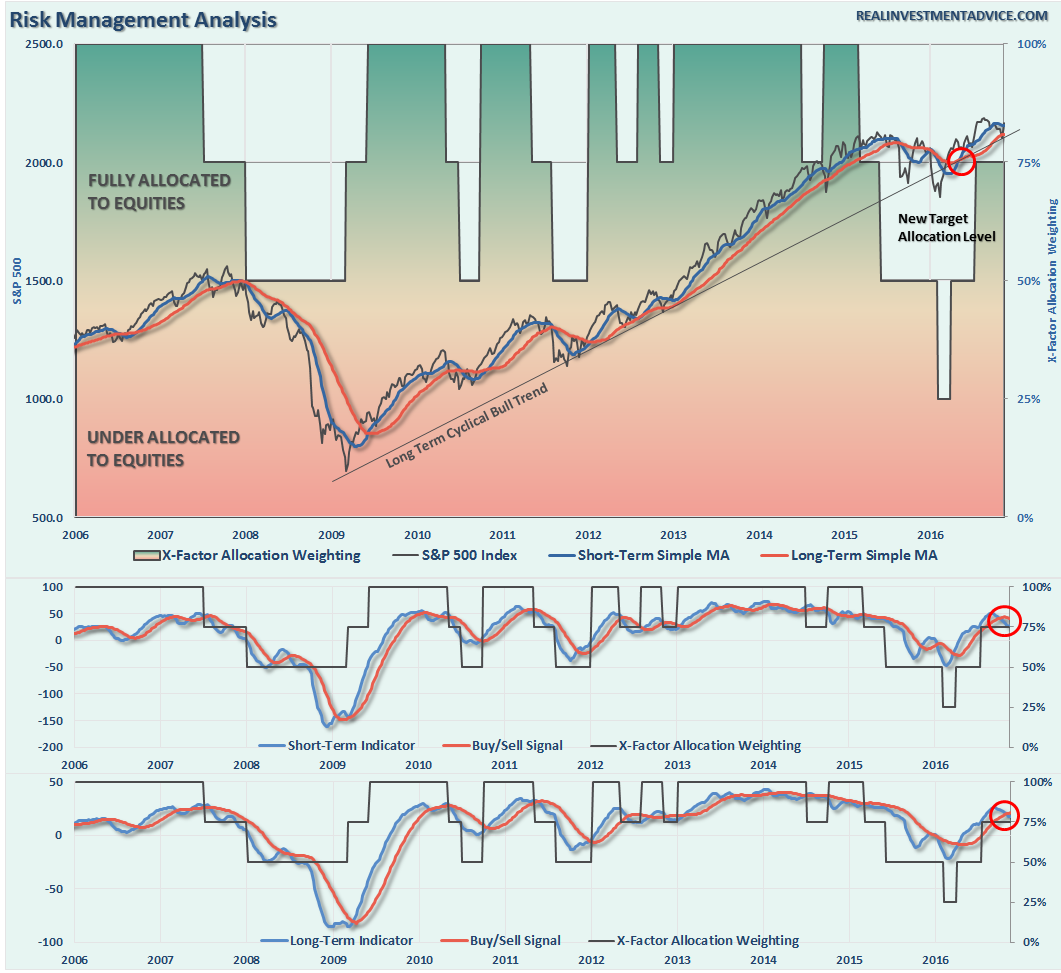

NOTE: I have redesigned the 401k plan manager to accurately reflect the changes in the allocation model over time. I have overlaid the actual model changes on top of the indicators to reflect the timing of the changes relative to the signals.

There are 4-steps to allocation changes based on 25% reduction increments. As noted in the chart above a 100% allocation level is equal to 60% stocks. I never advocate being 100% out of the market as it is far too difficult to reverse course when the market changes from a negative to a positive trend. Emotions keep us from taking the correct action.

Trump Wins – Market Surges

Well, that certainly wasn’t expected.

I don’t mean the “Trump” win.

I mean the markets surge as it was widely expected that a Trump victory was impending doom for the markets both domestically and globally.

The markets not only reversed the breakdown, and rallied this week as I suggested in last week’s missive, it also broke back above the downtrend resistance. This sets the market up for an advance in the near term back to all-time highs.

That’s the good news.

The bad news is, this rally is likely done for the moment and we need to wait for confirmation of the breakout before increasing equity exposure as we head into the seasonally strong period of the year.

As I stated last week, now reversed:

“By the time breaks of major support occur, and signals are registered, the markets tend to be grossly oversold. This is the case now and suggests a rally will likely ensue next week.”

Use the rally from last week to clean up portfolios as detailed in last weekend’s missive.

The lower allocations to “risk” in portfolios has lowered volatility and kept principal safe over the last several months. Once we can get past the election and get some clarity when can start making decisions about the “seasonally strong” period of the year.

However, as noted in the chart above, we have now triggered a secondary “sell” signal that keeps us on alert. As stated last week:

“We are dangerously close to triggering a second sell signal, the bottom part of the chart, which will likely coincide with a failed rally attempt over the next week or two. Such an outcome would suggest a weaker market environment in the intermediate term with a high degree of caution required.”

If you need help after reading the alert; don’t hesitate to contact me.

Current 401-k Allocation Model

The 401k plan allocation plan below follows the K.I.S.S. principal. By keeping the allocation extremely simplified it allows for better control of the allocation and a closer tracking to the benchmark objective over time. (If you want to make it more complicated you can, however, statistics show that simply adding more funds does not increase performance to any great degree.)

401k Choice Matching List

The list below shows sample 401k plan funds for each major category. In reality, the majority of funds all track their indices fairly closely. Therefore, if you don’t see your exact fund listed, look for a fund that is similar in nature.