by Dirk Ehnts

by Dirk Ehnts

It seems that banks in Germany are not so happy with the idea of publication of the results of the most recent stress test, as the FT reports:

But an association representing Germany’s financial industry lobby groups argues in a letter seen by the Financial Times that the disclosures could spark further market volatility, violate business confidentiality and expose banks to legal risks.

“Given the tense situation which already exists in money and capital markets, we believe publishing the results with the present level of detail would exacerbate the sovereign debt crisis,” the Central Credit Committee, or ZKA, wrote to the EBA, the regulator running the tests, in a letter dated July1.

“To avoid further capital market turmoil, which would fly totally in the face of what the stress test was actually intended to achieve, we believe the level of detail needs to be significantly reduced.”

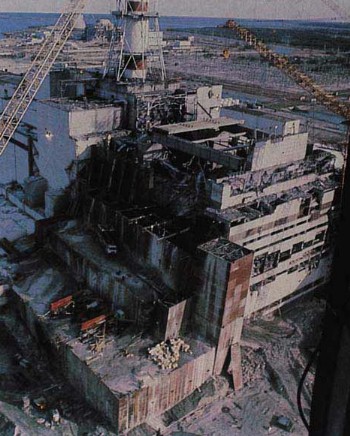

This reminds me of the 1986 Chernobyl nuclear disaster, which was caused by a test of the system. It led to a nuclear meltdown in the end.

A nuclear power station and a financial market have many things in common, from a systemic perspective. Among them are both complexity and tight coupling. While complexity is easy to comprehend, tight coupling might need explanation. Let me turn over to Richard Bookstaber (2007, p. 144), who now works as a Senior Policy Adviser to the Financial Stability Oversight Council and also Senior Policy Adviser at the SEC (and runs a blog):

The complexity at the heart of many recent market failures might have been surmountable if it were not combined with another characteristic that we have built into markets, one that is described as by the engineering term tight coupling. Tight coupling means that components of a process are critically interdependent; they are linked with little room for error or time for calibration or adjustment.

Last year I had the opportunity to talk to Andrew Haldane (just a day before the UK stress tests) and brought up this point (stress test results might lead to financial market turmoil). I think he understood that point. Does continental Europe understand it as well?

Related Articles

Banks: Flawed Regulation by Amar Bhide

Euro Crisis: Key Facts and Predictions by Elliott Morss

The Rough Politics of European Adjustment by Michael Pettis

A Quarter of European Banks are Stressed GEI News

Fragmentation of Global Power by Elliott Morss

End of the Shell Game? by Dirk Ehnts

Merchant of Venus Redux by Andrew Butter

U.S. and EU Debt Crises Compared by Andrew Butter

EU: Politics Financialized, Economies Privatized by Michael Hudson

Bank Capital is Illusory by Raihan Zamil

Dr. Dirk Ehnts is a research assistant at the Carl-von-Ossietzky University of Oldenburg (Germany). His focus is on economic integration and economic geography, covering trade, macro and development. He is working at the chair for international economics since 2006 and has recently co-authored a book on Innovation and International Economic Relations (in German). Ehnts has written at his own blog since 2007: Econblog 101. Curriculum Vitae.

Dr. Dirk Ehnts is a research assistant at the Carl-von-Ossietzky University of Oldenburg (Germany). His focus is on economic integration and economic geography, covering trade, macro and development. He is working at the chair for international economics since 2006 and has recently co-authored a book on Innovation and International Economic Relations (in German). Ehnts has written at his own blog since 2007: Econblog 101. Curriculum Vitae.