Econintersect: The IMF revised their projections for global economic growth.

Global growth is projected to increase during 2013, as the factors underlying soft global activity are expected to subside. However, this upturn is projected to be more gradual than in the October 2012 World Economic Outlook (WEO) projections.

The summary of the report continues:

Policy actions have lowered acute crisis risks in the euro area and the United States. But in the euro area, the return to recovery after a protracted contraction is delayed. While Japan has slid into recession, stimulus is expected to boost growth in the near term. At the same time, policies have supported a modest growth pickup in some emerging market economies, although others continue to struggle with weak external demand and domestic bottlenecks. If crisis risks do not materialize and financial conditions continue to improve, global growth could be stronger than projected. However, downside risks remain significant, including renewed setbacks in the euro area and risks of excessive near-term fiscal consolidation in the United States. Policy action must urgently address these risks.

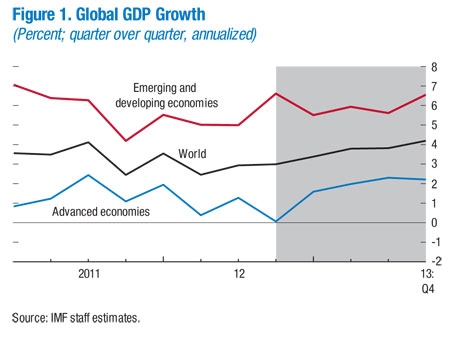

Economic conditions improved modestly in the third quarter of 2012, with global growth increasing to about 3 percent. The main sources of acceleration were emerging market economies, where activity picked up broadly as expected, and the United States, where growth surprised on the upside. Financial conditions stabilized. Bond spreads in the euro area periphery declined, while prices for many risky assets, notably equities, rose globally. Capital flows to emerging markets remained strong.

Global financial conditions improved further in the fourth quarter of 2012. However, a broad set of indicators for global industrial production and trade suggests that global growth did not strengthen further. Indeed, the third-quarter uptick in global growth was partly due to temporary factors, including increased inventory accumulation (mainly in the United States). It also masked old and new areas of weakness. Activity in the euro area periphery was even softer than expected, with some signs of stronger spillovers of that weakness to the euro area core. In Japan, output contracted further in the third quarter.

Turning to the updated outlook, growth in the United States is forecast to average 2 percent in 2013, rising above trend in the second half of the year (Table 1). These forecasts are broadly unchanged from the October 2012 WEO, as underlying economic conditions remain on track. In particular, a supportive financial market environment and the turnaround in the housing market have helped to improve household balance sheets and should underpin firmer consumption growth in 2013. The projections, however, are predicated on the assumptions in the October 2012 WEO that the spending sequester will be replaced by back-loaded measures and the pace of fiscal withdrawal (at the general government level) in 2013 will remain at 1¼ percent of GDP.

The near-term outlook for the euro area has been revised downward, even though progress in national adjustment and a strengthened EU-wide policy response to the euro area crisis reduced tail risks and improved financial conditions for sovereigns in the periphery. Activity is now expected to contract by 0.2 percent in 2013 instead of expanding by 0.2 percent. This reflects delays in the transmission of lower sovereign spreads and improved bank liquidity to private sector borrowing conditions, and still-high uncertainty about the ultimate resolution of the crisis despite recent progress. During 2013, however, these brakes start easing, provided that the planned policy reforms to address the crisis continue to be implemented.