Written by Steven Hansen

The Bureau of Labor Statistics monthly Job’s Situation is one of the most awaited reports. Pundits (including members of the Federal Reserve) talk about being in an employment strengthening cycle.

The degree employment is strengthening or not depends on how you view the data. My view is that employment is strengthening, but in the historical scheme of things – the rate of improvement is almost unnoticeable. I continue to have problems with the way employment data is delivered for consumption. Is a gain of xxx,xxx jobs good or bad???

The graph above shows both the seasonally adjusted gain of jobs in a given month (blue line in above graph), versus the percent change of jobs from the month one year ago (red line in the above graph). The red line has been fairly steady showing growth just under 2% for the last couple of years. With working population growing just under 1%, we are gaining jobs for the new entrants, as well as more jobs for the existing potential workforce.

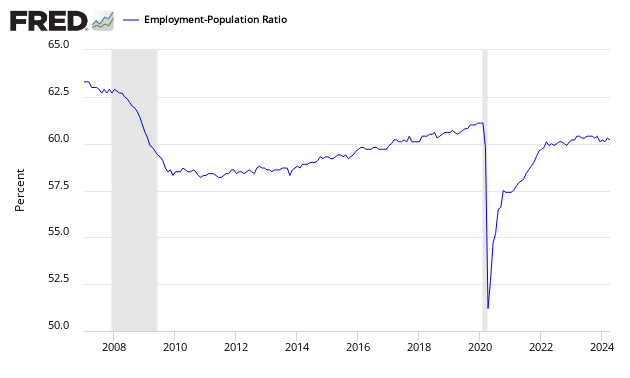

Confirmation of this growth cycle comes from another BLS data set in the household survey portion – Employment-Population Ratio shown in the graph below. This is a completely independent validation of growth – as the methodology and data do not overlap the headline jobs growth.

Unfortunately the trend line on the graph above shows improvement at the rate of no more than a half of a percent per year – meaning if this “improvement” continues, the total recovery of jobs is at least 8 years away.

Some argue structural changes are affecting employment. Per Federal Reserve Chair Yellen:

Along with cyclical influences, significant structural factors have affected the labor market, including the aging of the workforce and other demographic trends, possible changes in the underlying degree of dynamism in the labor market, and the phenomenon of “polarization”–that is, the reduction in the relative number of middle-skill jobs.

Consider first the behavior of the labor force participation rate, which has declined substantially since the end of the recession even as the unemployment rate has fallen. As a consequence, the employment-to-population ratio has increased far less over the past several years than the unemployment rate alone would indicate, based on past experience. For policymakers, the key question is: What portion of the decline in labor force participation reflects structural shifts and what portion reflects cyclical weakness in the labor market? If the cyclical component is abnormally large, relative to the unemployment rate, then it might be seen as an additional contributor to labor market slack.

There are structural shifts underway.

- It is very hard for the majority of the population to retire if they not like sleeping under bridges. Retirement benefits have been eliminated significantly from the private sector (and social security is not adequate as a sole means of retirement support);

- The decline of unionization has affected skill training;

- The secondary level school systems have eliminated skills training due to lack of funding. Now students must pay trade schools to learn skills;

- As the old folks cannot afford to retire, the young only have access to jobs through dead-man’s shoes;

- Robots will work around the clock;

- Young workers entering the workforce with higher education or skills carry loans which effect their ability to consume (and create other new jobs by their consumption).

And how did the USA get into this situation? One answer was to “transfer” responsibility for employment from the government who apparently was clueless on jobs to the Federal Reserve (who have no real tools to effect jobs growth).

The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.

[12 USC 225a. As added by act of November 16, 1977 (91 Stat. 1387) and amended by acts of October 27, 1978 (92 Stat. 1897); Aug. 23, 1988 (102 Stat. 1375); and Dec. 27, 2000 (114 Stat. 3028).]

I see no attempts at employment management being exercised by the Federal government. Employment management in the USA remains non-existent.

Other Economic News this Week:

The Econintersect Economic Index for September 2014 is showing our index declined from last months 3 year high. Outside of our economic forecast – we are worried about the consumers’ ability to expand consumption although data is now showing consumer income is now growing faster than expenditures growth. The GDP expansion of 4.2% in 2Q2014 is overstated as 2.1% of the growth would be making up for the contraction in 1Q2014, and 1.4% of the growth is due to an inventory build. Still, there are no warning signs that the economy is stalling.

The ECRI WLI growth index value has been weakly in positive territory for almost two years. The index is indicating the economy six month from today will be slightly better than it is today.

Current ECRI WLI Growth Index

The market was expecting the weekly initial unemployment claims at 295,000 to 325,000 (consensus 300,000) vs the 315,000 reported. The more important (because of the volatility in the weekly reported claims and seasonality errors in adjusting the data) 4 week moving average moved from 303,250 (reported last week as 302,750) to 304,000.

Weekly Initial Unemployment Claims – 4 Week Average – Seasonally Adjusted – 2011 (red line), 2012 (green line), 2013 (blue line), 2014 (orange line)

/images/z unemployment.PNG

Bankruptcies this Week: Lenco Mobile, Privately-held Associated Wholesalers, Privately-held Trump Entertainment Resorts