Money Morning Article of the Week

by Keith Fitz-Gerald, Money Morning

All eyes have been on Greek debt crisis this week, and rightfully so.

The country lied to get into the European Union, managed its finances terribly during its membership, and now wants to renege on its obligations.

I’m not surprised and chances are you aren’t either. We’ve been talking about the fallacy of central banking and the dangers associated with derivatives trading for years.

Now we need to talk about what happens next and, of course, what Greece means for your money.

The markets right now are all about the big boys and their toys, and specifically the estimated $1.5 quadrillion worth of derivatives on the planet at the moment.

You’re not hearing a lot about this because our leaders do not understand the connection, which, of course, means they do not understand the risks either.

Thankfully, we do.

The Risks of a Greek Default

Greece owes some 320 billion euros ($363.6 billion), approximately 75% of which is due to a motley crew of lenders including the International Monetary Fund, European Central Bank, European Financial Stability Facility, and Eurozone governments, all of whom are doing business with the world’s big banks and trading houses. Each euro is hypothecated at least once, but perhaps as many as nine times because of the way the world’s fractional deposit banking system works and the largesse associated with government printing.

In plain English, this means two things: a) that there may be only one euro in the system for every nine created out of thin air because b) the banks have entered into agreements that reuse collateral pledged by clients as collateral for its own trading or borrowing.

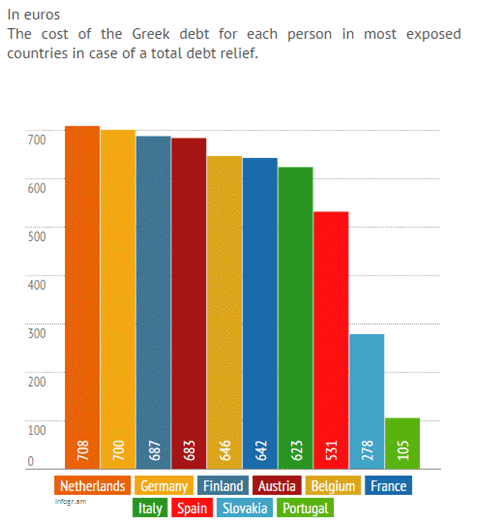

I realize this is hard to grasp, so let me put this another way by showing you the cost of Greek debt for each person in the most exposed countries in the event Europe has to do a total bailout.

It’s no wonder people are angry. If you live in Denmark or Germany, for example, you owe 708 euros ($805) and 700 euros ($795) respectively to cover Greece’s mess. Finland… 687 euros ($781). And so on.

Here’s where it gets really ugly, though.

In the event of a Greek default, the derivatives the big banks are trading as “insurance” against such an occurrence kick in. That, in turn, creates the risk of a cascading default as traders compete with each other to find the single euro of real money in the system and save themselves from ruin. The problem is that nobody knows who’s got it.

As a side note, if you’ve ever wondered why U.S. interest rates aren’t through the roof or rising faster than hot air at a political convention, here’s your answer.

In order to trade derivatives and re-hypothecate assets, you’ve got to have lots of collateral, ideally U.S. Treasuries because they’re considered the “safest” assets on the planet. This is why rates are low… because demand for U.S. paper remains high as a result of the constantly mounting trading risk.

I don’t know about you, but this kind of stuff makes me hopping mad because the big banks are, once again, being allowed to take the rest of the world on another white-knuckle ride nobody’s signed up for.

How the Greek Debt Talks Will End

I see three possible outcomes after the “trial period” for the next stage (assuming all approvals fall in place for it).

- Greece gets kicked out or “voluntarily” leaves the Eurozone. If this happens, I see the euro hitting parity with the dollar in a hurry. The U.S. stock market corrects immediately, then moves on because, let’s face it, letting Greece go it alone is like seeing Montana go bankrupt – only about 2% of the Eurozone’s GDP. No offence to Montana; I love your state and your people. Just making a relative comparison here to illustrate a point.

- The EU puts new rules in effect for Greek banks. This causes Greek markets to bounce hard. The euro falls, but stops short of parity. Global markets realign but don’t show any serious disruption longer term.

- There’s an agreement. World markets breathe a sigh of relief, the band plays on. Derivatives traders have a field day because, once again, they’ve won. The euro trades in a narrow band because “crisis is averted” as the headlines will undoubtedly trumpet.

The Austrian economist in me wants to see alternative No. 1 happen. It’s short, sweet, and the least damaging longer term. Some combination of No. 2 and No. 3 are probably what we’re going to get though.

That’s because Greece would effectively play make-believe in response to an offer from Europe to remortgage its financial obligations against a future that will somehow never arrive.

We could debate what that looks like all day long and it wouldn’t matter. That’s because any move, any agreement delivers what politicians the world over crave most – the appearance of reform.

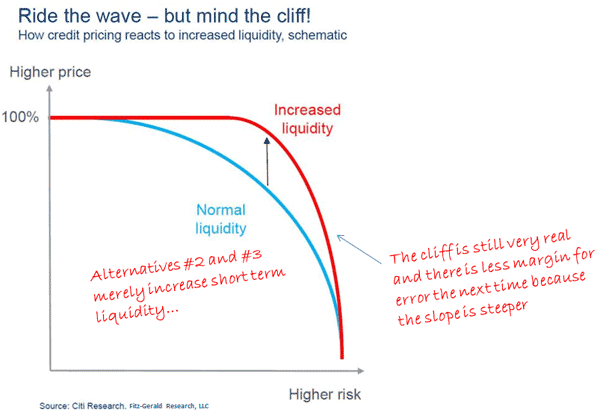

Neither really does anything other than stave off the inevitable because central bankers will not be doing anything more than increasing liquidity (again). The cliff everybody fears is still very real… just down the road a bit. And that means there is less room for error the next time Greece decides it doesn’t want to live up to its obligations.

My guess is that’ll be about 12 to 24 months from now, when Greek citizens figure out that fiscal responsibility comes with the territory and that this is what happens when you play in the big leagues.

So, how do you handle this?

First, you don’t panic. That’s the other guy’s job.

We’ve spent a long time preparing for this moment and we’ve gone to great lengths to recommend only the best companies with the strongest growth, earnings, brands, and promise knowing full well that those things are defensible when it comes to yet more central banking madness.

We’ve also increasingly limited our choices to the “must-have” sectors, which further reinforces upside opportunity. When this stuff breaks loose (and it will), our holdings will prove more resilient than the “nice-to-haves” everybody finds so appealing at the moment.

Second, we’ve got our trailing stops in place.

If the markets roll over, or even get rockier from here, we’re going to be taking our fair share of profits as we head for the sidelines. At the same time, we’ll be holding pat knowing full well that we’re also preventing small losses from becoming catastrophic portfolio wreckers from which most investors never recover. For more on how to use trailing stops to protect your gains, here’s a rundown.

And third, we’ve got an ace in the hole.

That’s the Rydex Inverse S&P 500 Strategy Fund (RYURX). This little gem zigs when the S&P 500 zags, so it’ll provide great balance if a Grexit turns into anything more serious than a short-term speed bump.

Most investors will find having 3% to 5% of overall assets invested in this fund not only stabilizes your overall investment portfolio, but can be a source of significant profits, too, if things head south.

If you don’t already own it, I wouldn’t wait much longer. Greece runs out of money in roughly 14 days and that means the train is leaving the station.

The Bottom Line: The Greek situation is tenuous at best. There are going to be lots of stops, starts, and conflicting headlines as we get closer to the drop-dead date by which either Greece has to have a deal or has to go it alone. Make sure your trailing stops are up to par as suggested and that you’re confining new money to the types of choices we’re laying out as “must-haves” rather than the “nice-to-haves” that offer you very little defense against central banking madness.