by Poly, Zentrader

In a runaway market like we have at present, it’s pointless to get into fundamentals to support the level of the market. The driving force behind a move of this nature is speculation – participants’ collectively bidding the market higher without regard to the move’s sustainability. The mere discussion of fundamentals, especially efforts to correlate them to the current market, is a sign of a failure to understand the character of the market. It’s like a game of “pass the parcel“; at some point the music will stop and those holding the bag will pay.

In the long run, fundamentals such as valuations and growth really do matter. Over time, imbalances are always corrected and the markets revert to their mean. In a runaway bull move, more realistic and conservative valuations emerge which better reflect the future prospects of the companies in the market. In short, we’re now near the top of a massive runaway move, and I’m positive that the market will soon be in a correction. Because the retail crowd is absent this time around and, thus, is not displaying the typical irrational exuberance found near tops, I hesitate to call this a bubble. But whatever the name, the current market is grossly over-valued and, from a Cycles standpoint, extremely stretched.

I continue to believe that the market is working its way to a major Yearly Cycle top, one which is likely to also mark the top of the current great bull market. It’s taking time to get there simply because powerful bull markets always surprise to the upside. Just as bear markets grind lower to the point of absolute exhaustion, bull markets just keep powering higher, throwing off even the most speculative of traders before topping.

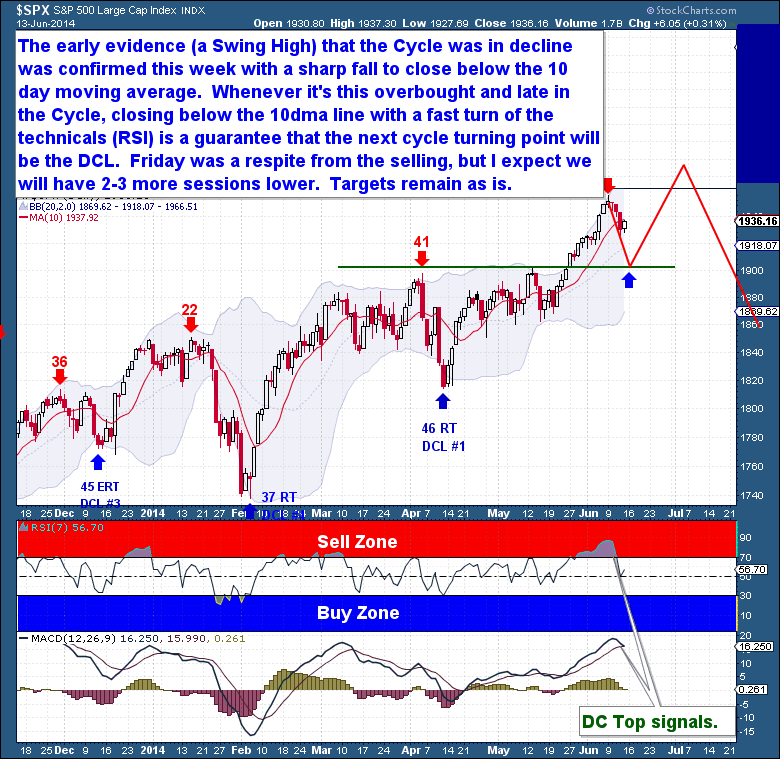

On the daily chart, the Swing High was confirmed this week when the S&P fell sharply to close below the 10 day moving average. Whenever the market is this overbought and this late in the Daily Cycle, closing below the 10dma and a turn in the technicals (RSI) almost guarantees a move into a DCL. Pundits grabbed the Iraq insurgency as the reason for the decline, but the Cycle was already on its way lower by the time the Iraq issue emerged.

Friday (a week ago, 20 June) was a respite from the selling, but I suspect it will turn out to be a one day pause to consolidate the 3 day sell-off. Once the markets open next week, I expect that the move will continue until the S&P finds a Cycle Low before the week is out. We have a FOMC meeting and press conference on Wednesday, and those events could well act as the DCL for the S&P.

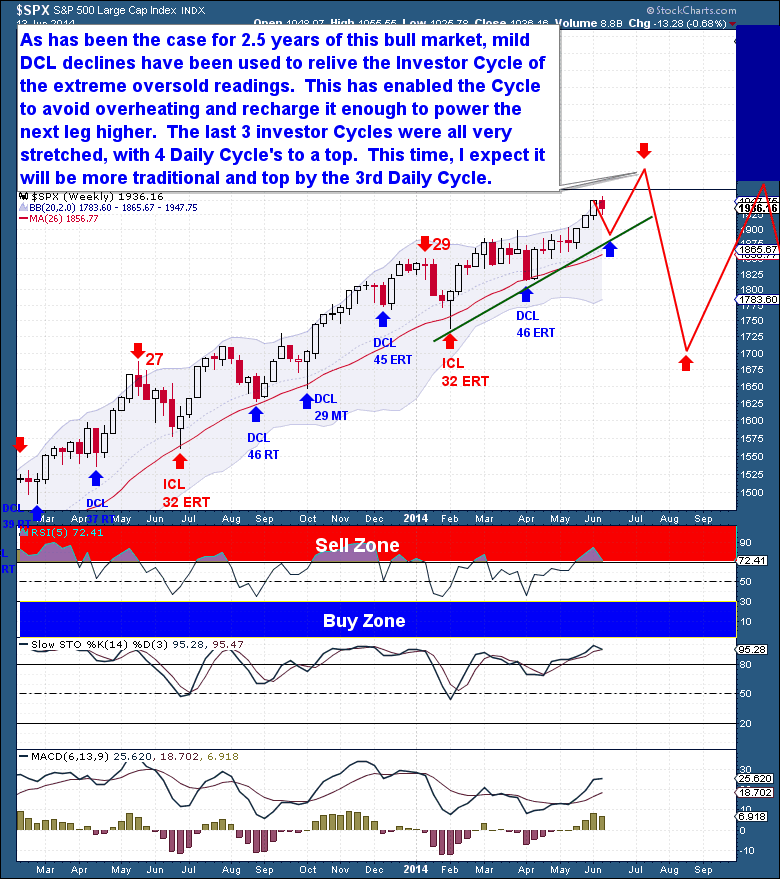

There is very little change in the Investor Cycle; the current move lower has helped only to relieve some of the more extreme overbought readings. This has been the case throughout the entire 2.5 year bull market. Each DCL has been mild and has served to relieve the Investor Cycle of extreme oversold readings. The DCLs have enabled the IC to avoid overheating and have sufficiently recharged it with the energy needed to power another leg higher.

The last 3 ICs were all stretched, and each had 4 Daily Cycles to the top as opposed to 2 or 3 Daily Cycles as is typical. This time, however, I expect we will see just 3 Daily Cycles, because the market needs the time to complete a Yearly Cycle decline within the framework of a steeper corrective ICL decline. But as the current Daily Cycle was so Right Translated, the final peak will need to come during the next Daily Cycle, and most likely near the end of the current month.

This is an excerpt from this week’s premium update from the The Financial Tap, which is dedicated to helping people learn to grow into successful investors by providing cycle research on multiple markets delivered twice weekly. Now offering monthly & quarterly subscriptions with 30 day refund. Promo code ZEN saves 10%.