Beware of Bubbles and Market Valuations in QE Sloshfest

by EconMatters, EconMatters.com

There have been several reports of money managers returning funds to investors because of a lack of attractively valued investment opportunities in the markets. This is actually very responsible and quite prudent from a fiduciary standpoint where most fund managers are so concerned about raising assets under management that they sacrifice the fund’s long term viability by investing at inopportune times, i.e., investing in assets at historically rich prices relative to the underlying fundamentals of the business.

QE has definitely distorted many asset prices to the upside, and with it finally ending this summer, fund managers are weary of buying at these levels without a guaranteed catalyst to replace the Fed’s monthly liquidity injections, and the global economy will really need to be humming along to replace $85 Billion of Fed injections via asset purchases. Thus, the takeaway is that many assets are overvalued when it comes to stock prices but we will focus on 5 candidates that we think are going to have a tougher time justifying their lofty stock prices due to a myriad of factors other than the taking away of the QE punchbowl.

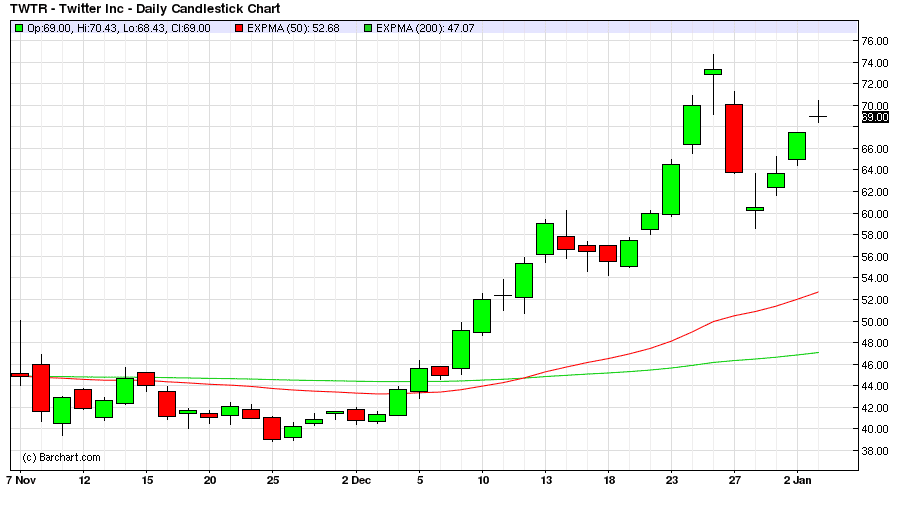

We will start with Twitter, Inc. (TWTR) which opened its IPO around $45 a share, traded between $40 and $45 a share for several weeks and then took off with the Santa Claus December Annual Rally to $73 a share. It is currently trading around $69 a share.

All the valuation metrics are going to look bad with this stock from EPS to Operating Margin and EBITDA, as the story for Twitter will be one of a growth stock so none of these valuations matter in the short term. This is the bullish case for the stock, and it makes for a great investment theme if you can sell the story that normal valuation metrics don’t matter, it creates the environment that many a momentum stock feeds off of from a frenzy standpoint.

However, the first and second earning’s reports for Twitter in 2014 are going to bring home the reality to investors that there is a difference between a great product used by the media and various celebrities for marketing purposes, and a revenue generating model that justifies a $38 Billion Market Cap.

The next bearish catalyst is the ending of the Lock-up Period, and as these probation periods from selling shares on the market expire, expect a lot more shares being added to the trading float trying to capitalize on the current lofty stock price in an overall bull market to secure their Payday for these initial investors in the company a la Facebook.

Once key technical support levels break and automated selling programs kick in this just adds more downside fuel to the fire as investors get nervous and reevaluate their “Greed Factor” and some large initial investors who were originally thinking in terms of holding out for becoming Billionaires, start to reevaluate and settle for becoming Multi-Millionaires, thus dumping additional shares onto an already saturated market.

Just like in Facebook, Inc. (FB) once the earning’s reality and the share unlocking takes place the Twitter stock will enter a defined downtrend, let the stock find a bottom before venturing to enter from the long side for what may provide a value proposition at some price.

But time will tell exactly what price constitutes value in this name, so investors will have to continually monitor earning’s results, the overall space that Twitter operates in, along with both the overall market and global economy.

But one thing is sure Twitter with a current Market Cap of $38 Billion, with it not actually being a profitable company by many financial metrics, is quite an expensive stock and due for a price realignment with a healthy dose of market reality reinforced by actual earning’s results in 2014.

Amazon

Amazon.com Inc. (AMZN) is the next candidate ripe for a pullback in 2014, it has had a nice run the last five years and the actual trading float is really small as much of the available float is in the hands of long term investors in the company.

However, with QE Infinity finally looking to come to an end which has definitely benefited this stock as much as any over the last five years, these long term investors may finally start locking in these gains and secure this wealth by diversifying into more capital preservation type investments. Especially since Amazon has gotten a relative pass on earnings over the last five years due to growing the company and gaining market share, at some point the company has to start producing larger profits than 0.28 earnings per share to justify a 1400 P/E ratio.

Our thesis on the stock is that Amazon finally starts to get punished for poor earnings in 2014 and in combination with the lofty stock appreciation over the last five years buttressed by a multitude of QE initiatives that capital gains finally get locked in at these levels in the stock. Similarly to how the major Apple run to $700 a share ended very abruptly with a six month and $300 haircut in the stock, once the downturn in investor sentiment occurs, and the downtrend gains speed, losses become self-fulfilling for investors, leading to additional selling, and given how far this stock has come in recent years there is no real support until the $240 a share level.

Consequently if the downtrend takes hold in 2014 the pullback could be quite severe for investors trying to hold through the weakness in the stock. Sort of like David Einhorn and Greenlight Capital’s approach to their Apple position, they would have been much better off by selling at $700 a share, and buying back in after the collapse at around $400 a share.

Amazon is a good company with a bright future, but from a valuation standpoint it is due for a major pullback in 2014. Any investors already in the name need to take profits ASAP, and new investors should avoid trying to pick a bottom too soon, Amazon has a lot of hot air in its stock price, and once the key technical levels of support fail, look out below!

Tesla

Tesla Motors, Inc. (TSLA) is our third stock candidate setting up investors for a sour 2014 campaign. The stock is the ebullient highs of around $195 a share, trading currently around the $150 a share level and we expect the stock to fall below the $100 a share level some time in 2014; whether that area represents a good buying opportunity for investors is an entirely different matter.

But some of the headwinds for 2014 are going to be stiff earning’s comps for 2013 where environmental credits made earnings look a whole lot better than they actually were given the lofty stock price. With the dismal automobile numbers for December being recently released it appears that many people who needed to upgrade their vehicles have already done so in 2013, and this was one of our concerns with GM as a possible headwind. Furthermore, given Ford’s downbeat profit forecast in 2014, December’s automobile numbers, and the rise in interest rates 2014 seems to be setting up for disappointment in the automakers, and yes that includes the electric car manufacturers as well.

We also think 2014 is finally the year that oil prices retreat with more supply coming on line than a slightly improving economy can utilize from a demand perspective that gasoline prices stay low relative to the peaks of the last four years, thus further dis-incentivizing the electric over fossil fuel economic switch by consumers. With the US Domestic oil resurgence, North American increased output and Iraq, Libya, and Iran all producing more oil globally in 2014 we expect oil to be under considerable price pressure which ultimately reflects itself in

downward pressure on alternative energy plays like TSLA.

Finally there is just the valuation of the stock, it can even be a great company with a long term bright future eventually, but the actual quarterly and annual automobiles that Tesla produces just doesn’t equate with a $19 Billion Market Cap with negative Earnings per Share, negative Operating Margin, negative Net Income and negative EBITDA. Plain and simple the stock is vastly over valued at current levels of automobile production based on company costs versus profits from an investment standpoint. Investors should not even begin to look at Tesla Motors, Inc. from a long standpoint until it drops below $100 a share.

Priceline

The fourth candidate due for a pullback in 2014 is priceline.com Incorporated (PCLN) which has had quite a run, more than doubling in 2013 alone, you think there isn’t a lot of liquidity out there in markets!

Priceline started 2013 at around $650 a share and reached a high of close to 1,200 a share in the fourth quarter before retreating to trading currently at the 1,130 level. You think some investors might want to take some profits in this name? You better believe it, the stock already looks to be rolling over and this stock is going to ramp up speed on the downtrend. It is a no brainer that Priceline falls below $950 a share in 2014; it is just a matter of how fast!

The price to the upside was fueled by the small float, low daily active trading volume, and lofty price so momentum to the long side just sort of snowballed, self-reinforcing the stock to excessive margin expansion in 2013.

With a $60 Billion Market Cap, and Gross Margin of 0.83 with Operating Margin of 0.36 and a P/E of 32.68 Priceline is one of the ‘uber-pricey’ names in the investing world and vastly over-valued when compared to solid companies like Apple Inc. (AAPL) with a P/E of 13.61 and Exxon Mobil Corporation (XOM) with a P/E of 13.00.

And arguments can be made for both of these solid companies to pullback in 2014 once stocks readjust to life without the Federal Reserve pumping $85 Billion worth of liquidity in the financial markets each month, i.e., Exxon Mobil Corporation is right at all-time highs for a company that has been around long enough for my grandfather to have invested in it!

This does not bode well for Priceline investors; get out while you still can because the drop is going to be brutal in this name for 2014. Moreover, investors in this stock, who have any historical reference, will remember the magnitude of the crash that this stock has undertaken in the past once the selling begins in earnest. For investors unfamiliar with the potential declines in this stock check the 1999 – 2000 time period charts.

I point this out to any bottom pickers, just stay away from this stock in 2014 the downside risk is too great for any potential upside gains, there is so much liquidity air in Priceline that there are going to be absolutely gut wrenching down days in 2014.

Netflix

The final stock due for a pullback in 2014 is Netflix, Inc. (NFLX) which is a great company, and has done wonders for the space, but valuations are just too rich considering the actual fundamentals of the business.

We have been Netflix, Inc. subscribers for years, and although we keep the product we recognize the limitations of limited selection choices compared to other online outlets, outdated series to binge upon, and more interesting live opportunities with competitive media viewing choices. My online media viewing world would be much more negatively affected if I suddenly lost YouTube access as opposed to our Netflix, Inc. subscription.

However, the real issue with Netflix is the valuation of the stock, and how much good news is already priced in the stock. Netflix received a great lift in 2013 when the original programming of House of Cards really boosted the stock, but the problem is that with binge viewing and no commercials, it only takes a weekend to knock out an entire season, and then the rest of the year is spent searching for decent content to watch. It still takes forever for the latest releases to actually hit Netflix streaming!

The stock more than tripled in 2013, going from around $100 a share to a high of $389 a share. The stock is currently trading at $363 a share with a Market Cap of $21 Billion, Earnings per Share of1.20, and a P/E of 303.85. Netflix is not a cheap investment, and frankly with the ever-changing landscape of online media who knows if the company will even exist in five years!

The problem is that with momentum stocks like Netflix, once a downside catalyst emerges, the bloom comes off the rose real quick as investors bail at record pace and all seemingly at the same time. Just look what happened to the stock when Reed Hastings raised subscriptions fees and made customers angry in the process, it went from $300 a share to $55 a share rather quickly.

It is no secret from an operational standpoint that Netflix is going to have to raise subscription revenue from existing customers, and at what price do customers just drop the service? We have it and frankly we can take it or leave it: the service offerings versus other viewing alternatives are probably below average even among free viewing options, and we are in the higher income bracket. The point is that Netflix is spending a lot of money to offer what little quality content they have right now, and they will need to spend more to keep up with consumer’s demands, and from an operational standpoint does the financial math even add up – is this a “destined broke” business model long-term? Can they ever bring in enough subscription revenue to balance out the soaring content costs and escalating requirements for additional new content and not alienate their customer base in the process? This is my real concern for the stock long-term aside from the 2014 valuation concerns. We don’t think the risk versus reward justifies any long position in the stock at these current price levels, and we expect a rather precipitous drop for the stock sometime during 2014.

If I had to bet on a catalyst it probably comes down to a series of relatively disappointing earnings reports in the wake of an increased volatility period inspired by lack of QE Liquidity in the market. Moreover, expect the drop to be significant, we expect at least a $100 a share price drop from current levels in the stock for 2014.

Final Thoughts

So now you have our five stock candidates ripe for a pullback in 2014. Be careful with these investment vehicles when trying to pick a bottom, just as they rose to tremendous heights with seemingly little effort, remember that margin debt has been at record levels for 2013, QE Infinity is finally being wound down, and interest rates are rising on cheap money both from a stock buybacks perspective, and an overall borrowing standpoint for the investing universe.

In short, these names can fall farther than investors ever think once the downside momentum kicks in, with existing buyers selling, newly added shorts coming to the table, and losses begetting additional losses. In the modern era of investing, market timing is just as important as picking the right companies to invest in, and 2014 will not be a good year for investors in these five companies.