Econintersect: The Congressional Budget Office has produced an economic outlook this year that will have pundits spinning the data. Economic outlooks never include forecasting recessions (there has been 10 recessions since 1950, and the USA has never gone without a recession in any 10 year period) – and this outlook is no exception. This forecast admits there is a headwind to employment caused by Obamacare. Econintersect is presenting this forecast beginning with a look at the changes from the previous forecast.

The following section comes directly from the CBO forecast:

Comparison With CBO’s February 2013 Projections

CBO’s current economic projections differ in some important respects from the projections it issued in February 2013 (see Table 2-3). In particular, projected growth of real GDP is now lower in each year than it was last February, and the projected level of real GDP in 2023 is 2 percent lower.21 (That comparison and the others discussed here exclude the effects of changes that BEA made to the definition of GDP in its comprehensive revision in July 2013, which are described in Box 2-1 on page 29.)22 Of that downward revision of 2 percent to output in 2023, 1½ percentage points stems from a reduction in CBO’s estimate of potential output, both for recent years and for the next decade, and one-half of a percentage point owes to a gap between actual and potential output that CBO now incorporates. The agency’s current estimate of potential output in 2013 is one-half percent lower than its previous estimate, primarily because of newly available data released in BEA’s comprehensive revision to the national income and product accounts (leaving aside definitional changes). And for 2013 to 2023, CBO’s projection for the growth of potential GDP is about 0.1 percentage point lower per year than its previous estimate, resulting in an additional downward revision to potential output of about 1 percent at the end of the projection period. The revision to projected growth of potential output over the next decade is the net result of several factors:

- A downward revision to the projected growth of potential total factor productivity (reflecting a reassessment of historical trends); that measure of productivity is now projected to grow by an average of 1.2 percent per year, compared with the 1.3 percent projected previously.

- A downward revision to the projected growth of the capital stock (reflecting new data and lower projected investment resulting primarily from higher federal debt); the capital stock is now projected to grow by an average of 3.1 percent per year, compared with the 3.4 percent projected previously.

- Little net change to projected growth of potential hours worked, as revisions to historical data that suggest a stronger trend were roughly offset by more negative estimated effects from the recession and weak recovery and from the ACA.

In addition, CBO now projects that, on average, a gap between GDP and potential GDP will remain during the 2018–2024 period. In the agency’s current projections, real GDP is one-half percent below potential GDP, on average, during that period. That projection is based on CBO’s estimate that, on average, GDP has been that much lower than potential GDP since the end of World War II and, in fact, lower than potential GDP during each of the past five business cycles. In contrast, last year CBO projected that GDP would equal potential GDP in the later years of the projection period.

CBO’s projection of GDP growth for the coming decade is revised down not only because of the downward revision to GDP at the end of the decade, but also because of an upward revision to GDP in 2013 stemming from last summer’s comprehensive revision of the national income and product accounts (leaving aside definitional changes).

Compared with last February’s estimates, CBO’s current projection for the unemployment rate is lower for the next few years but then higher. In the near term, the projection is lower because of unanticipated declines in the unemployment rate and the rate of labor force participation last year. Later in the coming decade, the projection is higher, as CBO anticipates that the rate will, on average, exceed the natural rate by about one-quarter of a percentage point; last year, CBO projected a return to the natural rate.

CBO currently projects higher long-term interest rates in 2014 and 2015 and higher short-term interest rates in 2015 and 2016 than it estimated a year ago. Those increases reflect in part a more rapid rebound in longterm rates during the past year than the agency had anticipated. They also reflect a somewhat faster projected recovery in the labor market, implying that the Federal Reserve is likely to start raising the federal funds rate slightly sooner than CBO previously expected. CBO also currently projects lower short-term and long-term interest rates in 2017 and later years than it estimated previously. Those decreases primarily reflect the new projection that real GDP will be slightly below its potential, on average.

The current forecast also includes a lower rate of inflation, as measured by the price indexes for personal consumption expenditures and GDP, over the next few years. Both overall and core inflation in the PCE price index in 2013 were lower than had been anticipated in CBO’s previous forecast. Core inflation rates tend to be fairly persistent, probably because observed inflation affects workers’ and businesses’ expectations for inflation, and those expectations influence workers’ bargaining for wages and businesses’ decisions about prices. So CBO has dampened its near-term projection to reflect the expected persistence of those recent lower-than-anticipated rates of inflation. In addition, BEA’s comprehensive revision of the national income and product accounts lowered estimates of historical inflation rates in the PCE and GDP price indexes. (As a consequence of that revision, CBO projects a slightly larger difference between inflation as measured by the CPI and the PCE price index than what it estimated previously.)

Given the downward revisions to both historical and projected inflation in the GDP price index, CBO has revised down its projection of the level of the GDP price index in 2023. In addition to lowering estimates of historical inflation rates, the comprehensive revision also adjusted the reference year for the GDP price index to 2009 from 2005. Therefore, in order to compare the current projection of inflation in the GDP price index with the previous projection, CBO adjusted the previous projection to reflect 2009 dollars. With that adjustment, the level of the GDP price index in CBO’s current projection for 2023 is 1.7 percent lower than the level that was projected a year ago. Coupled with CBO’s 2.0 percent downward revision to its projection of real GDP in 2023, the 1.7 percent downward revision to the level of prices in 2023 puts CBO’s current projection of nominal GDP in that year 3.6 percent lower than it was before.

Here is a summary level extract from the CBO

The federal budget deficit has fallen sharply during the past few years, and it is on a path to decline further this year and next year. CBO estimates that under current law, the deficit will total $514 billion in fiscal year 2014, compared with $1.4 trillion in 2009. At that level, this year’s deficit would equal 3.0 percent of the nation’s economic output, or gross domestic product (GDP)—close to the average percentage of GDP seen during the past 40 years.

As it does regularly, CBO has prepared baseline projections of what federal spending, revenues, and deficits would look like over the next 10 years if current laws governing federal taxes and spending generally remained unchanged. Under that assumption, the deficit is projected to decrease again in 2015—to $478 billion, or 2.6 percent of GDP. After that, however, deficits are projected to start rising—both in dollar terms and relative to the size of the economy—because revenues are expected to grow at roughly the same pace as GDP whereas spending is expected to grow more rapidly than GDP. In CBO’s baseline, spending is boosted by the aging of the population, the expansion of federal subsidies for health insurance, rising health care costs per beneficiary, and mounting interest costs on federal debt. By contrast, all federal spending apart from outlays for Social Security, major health care programs, and net interest payments is projected to drop to its lowest percentage of GDP since 1940 (the earliest year for which comparable data have been reported).

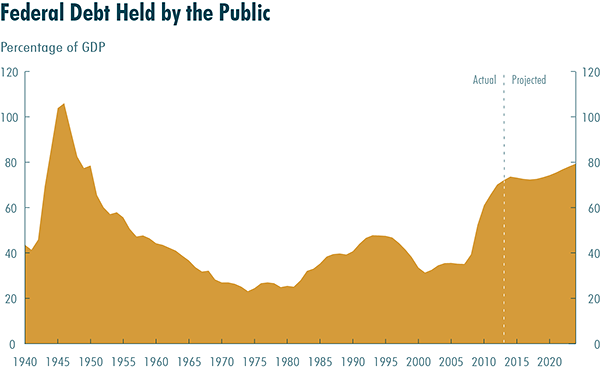

The large budget deficits recorded in recent years have substantially increased federal debt, and the amount of debt relative to the size of the economy is now very high by historical standards. CBO estimates that federal debt held by the public will equal 74 percent of GDP at the end of this year and 79 percent in 2024 (the end of the current 10-year projection period). Such large and growing federal debt could have serious negative consequences, including restraining economic growth in the long term, giving policymakers less flexibility to respond to unexpected challenges, and eventually increasing the risk of a fiscal crisis (in which investors would demand high interest rates to buy the government’s debt).

After a frustratingly slow recovery from the severe recession of 2007 to 2009, the economy will grow at a solid pace in 2014 and for the next few years, CBO projects. Real GDP (output adjusted to remove the effects of inflation) is expected to increase by roughly 3 percent between the fourth quarter of 2013 and the fourth quarter of 2014—the largest rise in nearly a decade. Similar annual growth rates are projected through 2017. Nevertheless, CBO estimates that the economy will continue to have considerable unused labor and capital resources (or “slack”) for the next few years. Although the unemployment rate is expected to decline, CBO projects that it will remain above 6.0 percent until late 2016. Moreover, the rate of participation in the labor force—which has been pushed down by the unusually large number of people who have decided not to look for work because of a lack of job opportunities—is projected to move only slowly back toward what it would be without the cyclical weakness in the economy.

Beyond 2017, CBO expects that economic growth will diminish to a pace that is well below the average seen over the past several decades. That projected slowdown mainly reflects long-term trends—particularly, slower growth in the labor force because of the aging of the population. Inflation, as measured by the change in the price index for personal consumption expenditures (PCE), will remain at or below 2.0 percent throughout the next decade, CBO anticipates. Interest rates on Treasury securities, which have been exceptionally low since the recession, are projected to increase in the next few years as the economy strengthens and to end up at levels that are close to their historical averages (adjusted for inflation).

Deficits Are Projected to Decline Through 2015 but Rise Thereafter, Further Boosting Federal Debt

Assuming no legislative action that would significantly affect revenues or spending, CBO projects that the federal budget deficit will fall from 4.1 percent of GDP last year to 2.6 percent in 2015—and then rise again, equaling about 4 percent of GDP between 2022 and 2024. That pattern of lower deficits initially and higher deficits for the rest of the coming decade would cause federal debt to follow a similar path. Relative to the nation’s output, debt held by the public is projected to decline slightly between 2014 and 2017, to 72 percent of GDP, but then to rise in later years, reaching 79 percent of GDP at the end of 2024. By comparison, as recently as the end of 2007, such debt equaled 35 percent of GDP (see the figure below).

Revenues

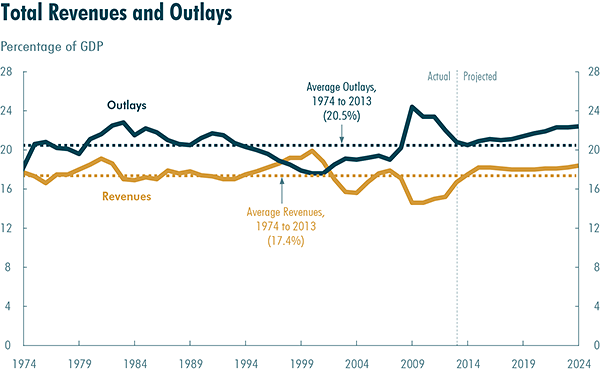

Federal revenues are expected to grow by about 9 percent this year, to $3.0 trillion, or 17.5 percent of GDP—just above their average percentage of the past 40 years (see the figure below). Revenues were well below that average in recent years, both because the income of individuals and corporations fell during the recession and because policymakers reduced some taxes. The expiration of various tax provisions and the improving economy underlie CBO’s projection that revenues will rise sharply this year. Those factors will increase revenues further in 2015, with CBO’s baseline showing another 9 percent rise. After 2015, revenues are projected to grow at about the same pace as output and to average 18.1 percent of GDP under the current-law assumptions of CBO’s baseline.

Spending

Federal outlays are expected to increase by 2.6 percent this year, to $3.5 trillion, or 20.5 percent of GDP—their average percentage over the past 40 years. CBO projects that under current law, outlays will grow faster than the economy during the next decade and will equal 22.4 percent of GDP in 2024. With no changes in the applicable laws, spending for Social Security, Medicare (including offsetting receipts), Medicaid, the Children’s Health Insurance Program, and subsidies for health insurance purchased through exchanges will rise from 9.7 percent of GDP in 2014 to 11.7 percent in 2024, CBO estimates. Net interest payments by the federal government are also projected to grow rapidly, climbing from 1.3 percent of GDP in 2014 to 3.3 percent in 2024, mostly because of the return of interest rates to more typical levels. However, the rest of the government’s noninterest spending—for defense, benefit programs other than those mentioned above, and all other nondefense activities—is projected to drop from 9.4 percent of GDP this year to 7.3 percent in 2024 under current law.

Changes From CBO’s Previous Projections

Since May 2013, when CBO issued its previous baseline budget projections, the agency has reduced its estimate of this year’s deficit by $46 billion and raised its estimate of the cumulative deficit between 2014 and 2023 by $1.0 trillion. (That 10-year period was the one covered by the previous baseline.) Those changes result from revisions to CBO’s economic forecast; newly enacted legislation; and other, so-called technical factors, such as new information about recent spending and tax collections.

Most of the increase in projected deficits results from lower projections for the growth of real GDP and for inflation, which have reduced projected revenues between 2014 and 2023 by $1.4 trillion. Legislation enacted since May has lowered projected deficits during that period by a total of $0.4 trillion (including debt-service costs). Other changes to the economic outlook and technical changes have had little net effect on CBO’s deficit projections.

Economic Growth Is Projected to Be Solid in the Near Term, but Weakness in the Labor Market Will Persist

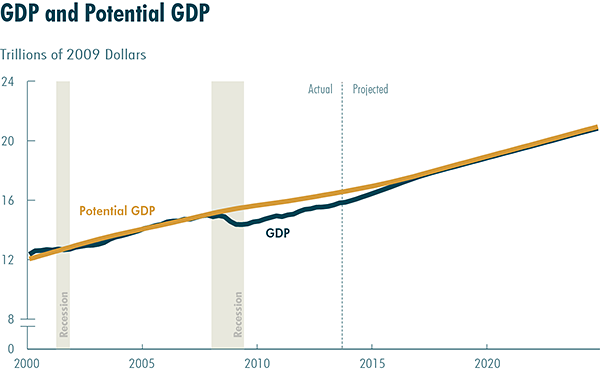

In the next few years, CBO expects, further growth in housing construction and business investment will raise output and employment, and the resulting increase in income will boost consumer spending. In addition, under current law, the federal government’s tax and spending policies will not restrain economic growth to the extent they did in 2013, and state and local governments are likely to increase their purchases of goods and services (adjusted for inflation) after having reduced them for several years. As a result, CBO projects, real GDP will expand more quickly from 2014 to 2017—at an average rate of 3.1 percent a year—than it did in 2013.

By the end of 2017, the gap between GDP and potential GDP (the maximum sustainable output of the economy) is expected to be nearly eliminated (see the figure below). Between 2018 and 2024, GDP will expand at the same rate as potential output—by an average of 2.2 percent a year, CBO projects. Thus, CBO anticipates that over the 2014–2024 period as a whole, real GDP will increase at an average annual pace of 2.5 percent.

The Economic Outlook Through 2017

Real GDP is projected to grow by 3.1 percent this year, by 3.4 percent in 2015 and 2016, and by 2.7 percent in 2017. CBO expects that those increases in output will spur businesses to hire more workers, pushing down the unemployment rate and tending to raise the rate of participation in the labor force (as some discouraged workers return to the labor force in search of jobs). That effect on participation in the labor force will keep the unemployment rate from falling as much as it would otherwise: CBO projects that the unemployment rate will decline only gradually over the next few years, finally dropping below 6.0 percent in 2017. Nevertheless, the labor force participation rate is projected to decline further because, according to CBO’s analysis, the upward pressure on that rate from improvements in the economy will be more than offset by downward pressure from demographic trends, especially the aging of the baby-boom generation.

CBO expects that the PCE price index will increase by less than 2.0 percent a year for the next several years. With such low inflation and considerable slack in the labor market, CBO anticipates that the Federal Reserve will keep short-term interest rates (such as those on 3 month Treasury bills) at their current low levels until mid-2015 but that long-term interest rates (such as those on 10-year Treasury notes) will gradually rise as the economy strengthens.

The Economic Outlook for 2018 to 2024

Beginning in 2018, CBO’s projections of GDP are based not on forecasts of cyclical movements in the economy but on projections of trends in the factors that underlie potential output, including total hours worked by labor, capital services (the flow of services available for production from the nation’s stock of capital goods, such as equipment, buildings, and land), and the productivity of those factors. In CBO’s projections, the growth of potential GDP over the next 10 years is much slower than the average since 1950. That difference stems primarily from demographic trends that have significantly reduced the growth of the labor force. In addition, changes in people’s economic incentives caused by federal tax and spending policies set in current law are expected to keep hours worked and potential output during the next 10 years lower than they would be otherwise. Although CBO projects that GDP will expand at the same rate as potential GDP, CBO also projects, on the basis of historical experience, that the level of GDP will fall slightly short of its potential, on average, from 2018 through 2024.

The unemployment rate is expected to edge down from 5.8 percent in 2017 to 5.5 percent in 2024 because factors associated with the persistently high long-term unemployment experienced in recent years are expected to have diminishing effects on the unemployment rate after 2017. As measured by the PCE price index, both inflation and core inflation (which excludes the prices of food and energy) are projected to average 2.0 percent a year between 2018 and 2024. Interest rates on 3-month Treasury bills are projected to average 3.7 percent during those years, and rates on 10-year Treasury notes are projected to average 5.0 percent.

To read the entire forecast:

[click on the image below to read the entire forecast]

source: http://www.cbo.gov/sites/default/files/cbofiles/attachments/45010-Outlook2014.pdf