PBOC May Be Trying to Cover for Credit Bubble Unprecedented in Modern World History

Econintersect: A press release by the People’s Bank of China (PBOC) was made available today (24 June 2013). The date on the document was 17 June 2013. All last week the PBOC was being criticized for lack of statements about the turbulence in the Chinese credit markets. For the story as it developed see GEI News, 19 June, 21 June and 22 June.

Now, if we can believe that the 17 June date represents when the banks in China received the policy statement then the PBOC was clearly communicating in real time to the banks, and in fact pre-announced the tightening of the short-term interbank lending market.

On the other hand, absent further information, it is also possible that the letter was backdated to 17 June in order to provide cover for what could be considered a failure to communicate.

And, if the letter was communicated to the banks on 17 June (and somehow was never leaked to the press), what is the justification of not making the information public in a timely manner?

Incendiary Statement?

Perhaps it is the incendiary nature of the statement, which essentially told the banks to manage their own liquidity, which would be a justification for not releasing to the public. Issuing such a directive in a country where rolling over loans has become a common factor could be something akin to yelling “Fire” in a crowded theater.

Exploding Local Government Debt

There has been much focus on the wild credit spending of local governments. Since February 2012 banks have received instructions to roll over many of the $1.7 trillion of local government loans when they come due in 2012, 2013 and 2014 rather than seek repayment or restructuring. (See GEI News.)

After only a year into this rollover program, Simon Rabinovitch reported (April 2013) in the Financial Times that local government debt was estimated at various amounts up to $3.2 trillion.

China Debt-Deflation Risk

Nearly a year ago John Hempton wrote a GEI Opinion article which warned that China faced a serious debt-deflation risk. Since then CPI has shrunk and PPI has spent nearly a year in deflation. Is the debt burden part of that prediction coming to pass?

Ponzi Finance by Manufacturers?

Also a year ago, Craig Tindale (GEI Opinion) wrote an article which discussed what appeared to be Ponzi financing by Chinese construction equipment manufacturers.

Special Investment Vehicles, Chinese Style

Last week Ambrose Evens-Pritchard reported in The Telegraph that the credit rating agency Fitch declared that China’s shadow banking system is out of control and under mounting stress as borrowers struggle to roll over short-term debts. Fitch listed as problems $1.4 trillion in so-called trust products in the shadow banking system and $2 trillion in wealth products. Much of these shadow banking system assets are “hidden second balance sheet” items for banks.

According The Telegraph, half of the wealth products niche must be rolled over every three months and another 25% within six months.

Note: Econintersect has not determined if there is overlap between the trust products and wealth products. If there is, the total would be less than $3.4 trillion, but more than $2.0 trillion.

China Banking System Bigger than U.S.

It appears that local government debt may not be the only over-leveraging problem facing China. Overall credit has grown within China from $9 trillion to $23 trillion in less than five years. This has replicated the entire U.S. commercial banking system for assets and kicked debt to GDP up to 200%, five times that of the U.S. going into the Great Financial Crisis of Japan at the top of their bubble in 1989.

This Need Not Be the End of the World

However, this need not lead to a global financial disaster. Here is an excerpt from The Telegraph:

“This is beyond anything we have ever seen before in a large economy. We don’t know how this will play out. The next six months will be crucial,” she [Charlene Chu, Fitch senior director in Beijing] said.

The agency downgraded China’s long-term currency rating to AA- debt in April but still thinks the government can handle any banking crisis, however bad. “The Chinese state has a lot of firepower. It is very able and very willing to support the banking sector. The real question is what this means for growth, and therefore for social and political risk,” said Mrs Chu.

Maybe not another global financial disaster but certainly a lot of economic stress. Michael Pettis may be able to collect on his bet with The Economist sooner than he expected. Pettis’ projection that China’s GDP would fall to 3% in its economic rebalancing efforts and The Economist challenged him on that.

Pettis may gain from his bet but the rest of the world will endure depressed economic activity if China growth falls to a U.S.-like level, especially all the commodity producers in the world.

Added note of interest: Here is another excerpt from The Telegraph:

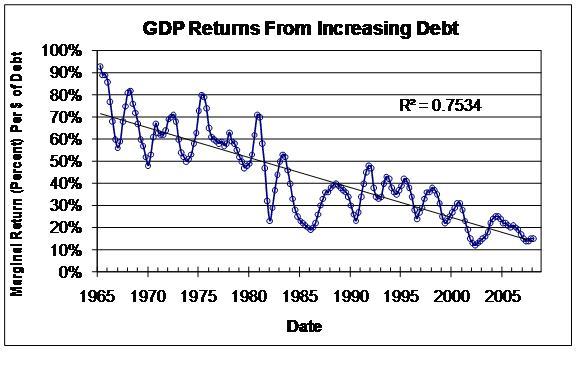

However, a new problem has emerged as the economic efficiency of credit collapses. The extra GDP growth generated by each extra yuan of loans has dropped from 0.85 to 0.15 over the last four years, a sign of exhaustion.

This behavior was observed in the U.S. in the years before the GFC. Following is a graph prepared by this editor using U.S. data in early 2009:

China is at the same 15% level reached by the U.S. in 2002 and 2008.

China is at the same 15% level reached by the U.S. in 2002 and 2008.

Here is the full statement released by the PBIC 24 June 2013:

General Office of the People’s Bank of China on commercial banks’ liquidity management issues letter

Source: communication 2013-06-24 11:08:47 2013-06-24

China PBOC Shanghai headquarters, branches, business management department, provincial (capital) city center branch, Shenzhen Central Sub-branch, the National Development Bank, the policy banks, state-owned commercial banks, joint-stock commercial banks, China Postal Savings Bank, Beijing Bank of Shanghai, Jiangsu Bank:

At present, the overall liquidity of the banking system at a reasonable level, but due to changes in the financial market factors, and near the end of half an important point, the objective of commercial banks liquidity management has put forward higher requirements. According to the current CPC Central Committee and State Council on the economic work of the relevant requirements, financial institutions must continue to conscientiously implement the prudent monetary policy, and effectively improve risk awareness, and constantly improve liquidity management and scientific initiatives, continue to strengthen liquidity management, promote stable monetary environment.

Commercial banks should pay close attention to the market liquidity situation, to strengthen the liquidity factors analysis and forecasting, good half a key point late liquidity arrangements. Commercial banks should concentrate storage for taxes and statutory reserve deposit and other factors impact on liquidity in advance to arrange sufficient positions to maintain adequate levels of reserve ratio, to ensure the normal settlement; according to macro-prudential requirements for an asset is reasonable configuration, carefully controlled expansion of credit and other assets too fast may lead to liquidity risk, market liquidity fluctuations in a timely manner to recapitalize; fully estimate the volatility of interbank deposits, effective control of maturity mismatches; financial institutions, particularly large commercial banks In strengthening its own liquidity management, while also actively play their own advantages, with the central banks play a stabilizing role of the market.

All financial institutions to balanced liquidity and profitability and other business objectives, reasonable arrangements for the total amount and maturity structure of assets and liabilities, a reasonable grasp of general loans, bills financing the configuration structure and delivery schedule, focusing on the stock of money and credit by activating support the real economy avoid deposits “red point” and other acts to maintain steady and moderate growth in money and credit.

General Office of People’s Bank of China

June 17, 2013

Sources:

- General Office of the People’s Bank of China on commercial banks’ liquidity management issues letter (The People’s Bank of China, translation, via Google, 24 June 2013, contents dated 17 June 2013)

- China: Banks Told to Roll Over Local Government Loans (GEI News, 12 February 2012)

- China local authority debt ‘out of control’ (Simon Rabinovitch, Financial Times, 16 April 2013)

- China’s Macroeconomic Miracle: Kleptocracy (John Hempton, GEI Opinion, 11 July 2012)

- China: Will a Concrete Bubble Turn into Concrete Shoes? (Craig Tindale, GEI Opinion, 05 July 2012)

- Fitch says China credit bubble unprecedented in modern world history (Ambrose Evans-Pritchard, The Telegraph, 16 June 2013)

- The Declining Usefulness of Debt (John Lounsbury, Seeking Alpha, 07 May 2009)