by Rohini Grover and Ajay Shah, ajay shah blog

A remarkable feature of options trading is that it reveals a forward-looking measure of the market’s view of future volatility. This was first done by CBOE in 1993 with the S&P 500 index options, with an information product named `VIX’ which reveals the market’s view of future volatility of the US stock market index.

CBOE computes and disseminates VIX every 15 seconds. VIX is often termed a `fear index’ as it conveys the fears of the market. It has found numerous applications:

- Time-series econometrics processes historical data to help us make statements about the future. VIX brings a unique forward-looking perspective into time-series analysis.

- VIX measures uncertainty in the economy e.g. when examining the effect of macroeconomic shocks (Bloom, 2009).

- The international finance literature has emphasised the role of VIX in shaping capital flows to emerging markets [example]. E.g. it is interesting to look at what happened in India on the days in which a very large rise or fall of the VIX took place.

- Trading strategies can be constructed which employ VIX as a tool for making decisions for switching between positions.

- VIX based derivatives offer methods to directly trade on VIX. In the US, CBOE introduced VIX futures and options on March 26, 2004 and February 24, 2006 respectively. In 2012, the open interest for these contracts was at 326,066 contracts and 6.3 million respectively. In India, futures on VIX have been launched at NSE, but the contract has not taken off.

All of us treat VIX as a hard number — we talk about a value of VIX such as 24.53 as if it is known precisely. But VIX is computed from a set of option prices. These option prices suffer from microstructure noise and from the limits of arbitrage. Each option price is only an imprecise reflection of the thinking of the market. This raises concerns about the extent to which imprecision in option prices spills over into imprecision of VIX.

In a recent paper, The imprecision of volatility indexes we offer a method for measuring the imprecision of VIX, and find that the measurement noise is economically significant.

VIX is a statistical estimator working on a dataset of option prices. Different estimators exist (e.g. the old VIX vs. the new VIX). Regardless of what estimator is used, the foundation — the option price — suffers from microstructure noise and is shaped by limits of arbitrage. Noise in option prices will induce noise in VIX. The only question is that of understanding how imprecise is the VIX.

For an analogy, consider estimation of LIBOR. Each dealer reports a reading of LIBOR. We recognise that each value obtained is a noisy estimator of the true LIBOR. This is aggregated using a simple robust statistics procedure to obtain an estimate of LIBOR. Bootstrap inference is used to obtain a confidence interval about how imprecise our esitmator of LIBOR is. [Cita and Lien, 1992, Berkowitz, 1999, Shah, 2000].

A similar strategy is relevant for VIX. Each option should be seen as a noisy estimator of the implied volatility. Bootstrap inference can then be used to create a distribution of the vega-weighted VIX (VVIX). This yields a confidence interval for VVIX.

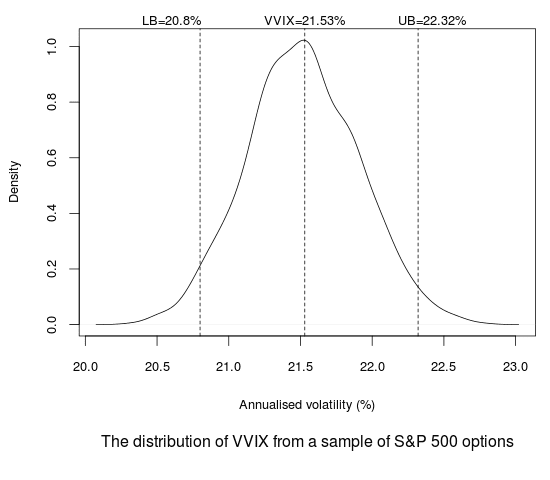

As an example, for a sample of end-of-day S&P 500 options, on 17th September, 2010, the at-the-money (ATM) options with 29 days to expiry show significant variation and take values between 15% and 21%. Our methods yield a distribution of the estimated VVIX:

As the graph above shows, the point estimate for the VVIX is 21.53% and this is what all of us are used to talking about. But the noise in option prices has induced an economically significant imprecision in our estimated VVIX. The 95% confidence band, which runs from 20.8% to 22.32%, is 1.5 percentage points wide. This is an economically significant number, since the one-day change in VVIX is smaller than 1.5 percentage points on 62% of the days. This suggests that on 62% of the days, we know little about whether VVIX went up or down when compared with the previous day.

To conclude, we got a huge step forward when options trading improved our knowledge of the universe by giving us a forward looking estimator of future uncertainty. However, market microstructure noise and the limits of arbitrage hamper our ability to know about the future: VIX is not a hard number. There is significant uncertainty in what we know about VIX. This insight may make a difference to many applications of VIX.