by John Mauldin, Thoughts from the Frontline

Vizzini: He didn’t fall?! Inconceivable!

Inigo Montoya: You keep using that word. I do not think it means what you think it means. – From The Princess Bride“A tariff is a scale of taxes on imports, designed to protect the domestic producer against the greed of his consumer.” – Ambrose Bierce

“Vast possibilities matured into realities before their very eyes. Nevertheless, they saw nothing but cramped economies struggling with ever-decreasing success for their daily bread.” – Joseph Schumpeter on the Industrial Revolution

The usual thrust of this letter is economics, finance, and investing. Lately, however, the political process has been invading my normal domain – sometimes to the dismay of some of my readers. I get that politics comes with the territory; and I think everyone, no matter their political persuasion, will agree that taxes, which are political in nature, have a major impact on economics, finance, and investment. And thus commenting on taxes is fair game.

My original intention for this letter was to do an analysis of the Republican tax reform proposals. My associate Patrick Watson and I spent two weeks doing a really deep dive into the proposed reforms. I had the privilege of talking taxes with the chairman of the House Ways and Means Committee, fellow Texan Kevin Brady, as well as his staff. The chairman was kind enough to allow his remarks to be on the record – but his staff made it clear that they were to be on background. We have also talked with numerous think tanks and other experts across the political spectrum. We’ve actually been able to get information on some of the proposed reforms that, as far as we can tell, isn’t available in anything that’s already out there on the Internet.

A few observations from 30,000 feet –

- This is a far more sweeping proposed tax reform than Reagan’s. Not even in the same league. When I tell you that it touches everything, I mean that it touches EVERYTHING. And not just in the US. When you begin to think it through, the global implications are truly staggering. If you think you can be in Europe, Asia, or Africa and just be an unaffected observer of these changes, you are not paying attention. They will have profound implications for currency valuations and global trade. Thus what I have for you today is not a one-and-done letter on the proposed tax reform. This is the first part of a series (my guess is that it will run to at least three parts) on the implications of the proposed reform. I keep using the word proposed, as there is a great deal of contention around this legislation. What actually comes out of the sausage-making machine otherwise known as Congress is still hard to predict. But we’re going to explore the key proposals coming out of the Ways and Means Committee, which are what will be debated on the floor.

- There are parts of this tax proposal that I really like; there are parts I’m okay with; and there are parts that I think have potentially serious negative implications for some people and countries. There will be very clear winners and losers. But as one insider told me, there are always winners and losers in any major tax reform. If we leap ahead seven years, I think we’ll find the overall economic climate much improved by what I am seeing proposed today. It is the transition to that outcome that concerns me. The ride from here to there could get rather bumpy.

- At the heart of the proposed reform is the very serious objective of creating new jobs. But which jobs, what kind of jobs, and where? At the top of the letter I quoted Montoya from The Princess Bride (come on, you have to admit that you watched it at least once): “I do not think that word means what you think it means.” As we will see today, I am not sure that job creation means what the Republicans think it means.

We are going to look at the proposed tax reform on a philosophical level first and then drill down into the nitty-gritty of the actual proposals. As noted above, almost every person that I talked to about tax reform agreed that the first objective must be to create jobs.

I was told of a private conversation between Steve Bannon and Elon Musk. Bannon was laser focused on creating jobs. “How do we get solar jobs in West Virginia?” he demanded of Musk. The entire transition team’s number one objective is creating jobs. Good jobs, American jobs. That was the heart and soul of Trump’s campaign. Even Paul Krugman will tell you that the way to get out of our current malaise is economic growth through job creation. While there are serious disagreements on the path, everybody agrees on the objective.

Except.

I am not so sure that everyone understands the nature of the terrain we must cross in our quest to create jobs, let alone the changing characteristics of the objective.

The Amazonian Jungle

Let’s start with a story to illustrate my concern. There is a company in the United States that began by offering a few products directly to consumers, and then quickly expanded its offerings until they included almost everything a person could want. This company went directly to the consumer, bypassing local brick-and-mortar stores, and became enormously successful, meeting the needs of its customers all over the country. Of course, the local stores were often (as economists will say) “disintermediated,” which is a fancy way of saying they couldn’t compete on price and selection, let alone delivery and convenience, and went belly up. And with them went the jobs of the people they employed.

Recently I’ve been using that story in my speeches and conversations, and everyone nods their heads and says, either out loud or mentally, “Amazon.” Except that I’m not talking about Amazon. I’m talking about another icon of American retailing called Sears, Roebuck & Co.

In the late 1800s, Richard Sears began to sell watches by mail order. He sold that company, but a few years later he started another mail order business to sell clothing and other products. The initiation of rural free delivery in 1896 and parcel post in 1913 enabled Sears to send its merchandise to even the most isolated customers. The Sears catalog became a staple of American family life. By the 1960s one out of 200 US workers received a Sears paycheck, and one out of every three carried a Sears credit card. The Sears catalog was a book of dreams that allowed those of us who grew up in rural America to access products that were either not available or were very high-priced in our local general store.

It’s hard for the younger generation to understand, but the Sears catalog coming to our mailbox was a big event in my youth. The Montgomery Ward catalog was a close second. The whole family perused those catalogs page by page to mull over what we needed or wanted. I’m sure I was not the only kid who circled a few toys that he hoped Santa would bring him for Christmas.

It’s hard to believe, but Sears didn’t really have a physical store until the 1920s, by which time the company was the largest retailer in the world. But Sears’ experience enabled Sam Walton, who didn’t start until 1962, to surpass Sears by 1990; and by 2000 Walmart’s sales were six times those of Sears.

Fast-forward to 2017. The 178,000 current employees of Sears are an endangered species. Sears had 3555 stores in 2010, and today it has 1503 and will close another 10% of those this year. Additional stores will be closed sooner rather than later. Unless hedge fund genius Eddie Lampert can pull yet another rabbit out of his seemingly bottomless hat, Sears will pass the way of Blockbuster and Kodak.

Remember Blockbuster? Founded in 1985, at its peak in 2004 Blockbuster had 60,000 employees and 8,000 stores. By 2010 it was bankrupt. There are only about 50 Blockbuster franchise stores still left.

But what do these sober tales have to do with tax reform? Tax reform, at least the Republican version, is predicated on creating jobs in the United States. In his campaign and since, Trump has focused on how Americans are losing jobs to foreign competitors. A seemingly straightforward trend, right? Jobs leave here and go to China and Mexico.

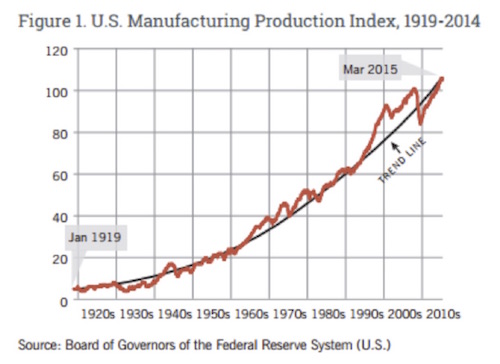

The truth is a little more complex. The simple fact of the matter is that United States is producing more manufactured goods than ever before. And the growth trend in manufacturing, which was established in the 1920s, has shown no signs of slackening, even through recessions. The chart below is from a study done by two professors at Ball State University. It’s a fabulous analysis that shows that 80% of the jobs that have been lost in American manufacturing have been lost due to technology. American workers are now dramatically more productive than they were in just the year 2000. The authors point out that our 12 million manufacturing jobs today produce the same amount of goods as 21 million manufacturing jobs did in 2000.

That trend is not going to change. Technology is going to continue to increase the productivity of American (and global!) manufacturing. With companies like Foxconn in China creating robotic production lines, the cost of labor is truly becoming a rounding error in manufacturing.

Prediction: Apple will soon be manufacturing the iPhone 9 or 10 in the United States. But producing those iPhones here won’t create that many jobs, because the work will be done on a robotic assembly line. If the border adjustability tax, which is part of the proposed tax reform happens, Apple will onshore that production even faster. Why? Because the most tax-advantaged country in which to produce products will be the US. True, other countries might offer zero tax as well, but they don’t have the infrastructure and available talent that the US does.

I hear my friends in Europe protesting, but the proposed Border Adjustable Tax (BAT) is significantly different from the VAT (value-added tax) that is used in over 160 countries. That tax simply increases the cost of manufacturing in those countries. (As we will see next week, the BAT is both a feature and a bug of the tax proposal.)

We can all argue over the efficacy of supply-side economics, but the reality is that Reaganomics created a marvelous boom of both productivity and employment. Bill Clinton had the advantage of that wind in his sails, and when coupled with Newt Gingrich’s reforms, it allowed him to balance the federal budget. (It helped, too, that Ross Perot siphoned off enough votes to allow Clinton to become president. Timing is everything, and Bill Clinton had nothing if not remarkable timing.)

The current tax proposal would make Reagan proud. And the expectations of everyone I am talking to are that the planned tax reforms will have the same effects that reforms did in the ’80s and ’90s. Problem is, now it’s 2017.

I am worried that the future won’t see us losing manufacturing jobs so much as service jobs. Losing 178,000 Sears workers is a big deal. But Amazon is slowly putting small businesses out of work, too: we’re losing 5 jobs here and 10 jobs there.

Some of the biggest mall owners in the world (according to a Wall Street Journalcover story) are simply turning the keys over to the bondholders who financed the mall mortgages. They can no longer make money on their properties. If Sears closes down, that takes the anchor store out of hundreds of malls, making them less viable. Stores in the mall that depend on Sears building the traffic go away as well.

If you are in the market for a diamond, do you go to the mall to look in jewelry stores? Not if you’re a smart shopper. You might go to the mall to see what you like, but you buy at Blue Nile, which is a kind of eBay for diamonds and other jewelry.

Personal story: Some of my friends know that I am now actually engaged, so I was in the market for a nice diamond. I called two friends who turn up their noses at having to pay retail or even wholesale. I wanted to buy my diamond wherever they would go. They both said that the diamond market has completely changed. Go to Blue Nile, they said; you can get practically anything you can imagine, and it gets delivered quickly. Diamonds are typically sold at about a 3% margin, but that is not a margin that mall jewelry stores can survive on.

Amazon and Walmart did just fine last Christmas. Many other retailers, not so much. Online sales grew by 14% last holiday season, the fastest growth in five years. In-store sales grew by only 1.4%, not even keeping up with inflation. And that trend is going to continue. Amazon and its online cohorts are clearly the wave of the future. One of the last great catalog companies, U-Line, sends their catalog out as a spur to online purchasing, not so much as an alternative method. I have recently been in one of their million-square-foot warehouses, and they were literally shipping orders the same day.

As longtime readers know, I’m writing a book about what the next 20 years will look like. And as I’ve mentioned before, the most difficult chapter is on the future of work.

In the coming weeks, we are going to see that the proposed tax reform is going to turn the finance world on its head. That world – what we think of as traditional banking and investment –puts only about 15% of its investment money into new-business development. The rest goes to financialization and the buying and selling of existing companies (share buybacks, etc.).

In the proposed tax reform, 100% of investments will be allowed to be written off in the first year. Build a factory? Forget amortization: write it all off this year. Everything but the land will be a 100% write-off. Not only will that policy create construction jobs; it will create jobs for people who make the equipment that goes into the production lines, as well as jobs for people who work in those plants.

The current tax proposal works well for traditional businesses. And it will certainly kindle whatever animal spirits are out there in nascent form.

(Preview: I started asking the staff who are tasked with coming up with a myriad of rules that will be used in the tax proposal, Will we be able to write off this or that? How will you treat offshore service income? On and on I went. Their stock answer was, “We haven’t decided that yet.” But their thrust was to do everything they possibly could to spur investment today and create jobs now!)

Upon reflection, I am not sure that you could create more retail and service jobs with any other tax reform than what is proposed, but that reform may not be enough. As more and more retail jobs succumb to online sales, robots, artificial intelligence, and other technologies, it may be increasingly difficult to counter the losses with new job gains. Not this year or next year but sometime in the future we are going to have to consider what we as a society are going to do in a post-employment world.

By that I don’t mean that work will disappear, but there will be ever fewer jobs for workers who are “down the food chain.” Between 2022 and 2030 we are going to see the loss of roughly 3 million truck and taxi driver jobs. Where will those people find other work? And that is just one industry.

What happens when we have a silver bullet for cancer? Which we will, hopefully sooner rather than later. All those hospitals, all those healthcare workers, all those pharmaceutical companies that depend on a steady supply of cancer patients will be out of work. And we are talking hundreds and hundreds of thousands of workers, who are generally highly paid. What happens when we beat Alzheimer’s? Or any one of another dozen diseases that are terribly debilitating and that cost enormous amounts of money to take care of and require the services of hundreds of thousands of caregivers.

I’m going to stop here and pick up our discussion next week. But I’m going to leave you in the capable hands of my good friend Charles Gave, who will talk about yet another problem that could become a global issue because of the border adjustment tax (BAT). Rather than restate his brilliantly outlined concerns, I’ll share them with you in their original form. (I thank my friends at GaveKal for letting me use Charles’s work so freely.) At the end he offers what he calls a modest proposal to save the world. In one of the upcoming parts of this series I will offer my own version. And make no mistake, we are talking about saving the world. When I say this tax proposal touches everything, I mean everything.

Next week we will look at other problems surrounding the BAT. I get the concept and even agree with the basic proposition, but the proposal comes with some serious potential unintended consequences. For now, though, let’s consider what has Charles worried: the end of the US dollar’s reign as the world’s reserve currency.

The End of the Dollar Standard

By Charles Gave

I find myself in the strange situation of cheering Donald Trump’s nascent program of economic renewal for the US, while worrying deeply about the domino effect that may topple a dollar-based global financial system whose health has relied greatly on benign neglect by the United States.

The good news is that since the fall of the Berlin Wall I have never seen a president or prime minister of the right come into power with an agenda that so squarely opposes the doxa of left-leaning elitist circles. Whether in education, regulation, taxes, ecology, energy production, culture, justice, military strategy or national security, most of the president-elect’s cabinet nominees have for decades fought a flabby intellectual orthodoxy.

Yet, while I welcome Trump’s attack on a credo which has done much to enfeeble the Western world, I am not blind to the violent economic and financial dislocation which may mark the transition from one reserve currency order to another. At the end of this paper, I offer a modest suggestion for avoiding a scenario which has the potential to morph into a 1930s-style beggar-thy-neighbor episode on steroids.

The starting point is that the US dollar has been the world’s reserve currency since the end of World War II, with 1971 marking the transition to a pure fiat regime. Markets, institutions and investor habits have developed according to this basic building block. Yet there is nothing immutable or inevitable about the US sponsoring such a currency arrangement. Indeed, Trump’s core economic platform of trade protection points to the US pursuing an objective which is guaranteed to kill the existence of the US dollar as the sole reserve currency – namely the US’s apparent pursuit of a current account surplus.

The Double Pyramid of Credit

To explain my point, I will use Jacques Rueff’s powerful framework for thinking about the US dollar’s international relationships, namely the “double pyramid of credit”. Rueff was an economist and senior civil servant who between 1923 and 1969 was France’s chief negotiator at international monetary conferences, and a sophisticated observer of the international payments system. Rather like his archrival John Maynard Keynes, Rueff was both a theoretician and a practical man of action who was involved in actually building the global financial system.

One of his key ideas was that in the post-gold standard era, a side effect of one country controlling the reserve currency would be an end to the zero sum game of credit expansion associated with an independent specie-based system. Instead, Rueff’s double pyramid of credit idea described a new order that would likely be characterized by inflation, over indebtedness, capital misallocation, and episodic financial crises.

By way of a simplified example, consider a Rueffian take on the relationship between the US and Japan under the post-1971 US dollar reserve system. Say the US went through a big credit expansion, causing it to run a large current account deficit with its East Asian trade partner. The corresponding current account surplus in Japan would spur creation of new Japanese bank deposits, and with them a credit expansion.

Under the gold exchange standard, such credits in Japan would have been offset by reduced money supply in the US due to the physical transfer of gold from the US to Japan by way of deficit settlement. As a result, the global system of payments was a zero sum affair; and credit expansion did not, on balance, change over time.

This was upended in 1971 when the US stopped settling its current account deficit in gold (Charles de Gaulle, on Rueff’s advice, catalyzed this shift by demanding that the US settle with a physical transfer of gold ingots). Subsequently, US dollars earned by Japanese firms have not been exchanged against gold, but rather “redeposited” at the Federal Reserve via a process of foreign exchange reserve accumulation. As a result, the US has not faced higher interest rates from its deficit with Japan and by extension from its habitual global current account deficit.

It was this ability for credit to keep growing in both the US and its creditor nations that led Rueff to coin his double pyramid moniker. In the above example, both Japan and the US were able to sustain credit growth, although the ultimate source for both was “excess” US money supply.

This money creation machine has only properly broken down during periods of high US inflation which have necessitated sustained tightening by the Federal Reserve. Experience has shown that the US central bank has kept obsessively focused on consumer price inflation and disregarded events in asset markets, even if stocks were surging, the dollar exchange rate was plunging and property prices were going stratospheric. The Fed has proven willfully blind to effects from the double pyramid of credit by responding only to US price and growth data. In short, it may be the world’s central banker, but the Fed has resolutely only followed US rules.

The Problem of Divergence

The problem with this double expansion of credit is that it tends to compound economic divergence, rather than convergence, which for all its faults was the logic of the old gold exchange standard. Consider the experience of Japan and the US over the last 30 years. The former proved unable to manage twin objectives of limiting yen appreciation and keeping control of its money supply. The upshot was a huge asset bubble in the late 1980s, which turned into a bust from which Japan has never fully recovered.

Fast forward to the early 2000s when two new beneficiaries of this double pyramid of credit started to take off. One was China and the other, what we have called “platform” companies, or firms which outsource much of their production and working capital needs to dispersed supply chains in places such as East Asia, Eastern Europe and Mexico.

The rational actions of these two “actors” following Rueff’s double-pyramid-of-credit logic has resulted in violent asset price cycles – Chinese financial repression led to surging property prices, oil experienced an epic boom-bust cycle and US equities have been pumped up on the promise of permanently cheap money. The flip side has been acute deindustrialization in the US as firms have shifted production to China and other low cost production centers. Put simply, the double pyramid of credit phenomenon hugely exacerbated the hollowing out of the US industrial sector, and so is the proximate cause of Trump’s rise to power.

Indeed, it is ironic that US automobile firms are making cars in Mexico for sale to US buyers who can’t – by any normal measure – afford to buy them, as they don’t have a proper job. Luckily US auto firms have organized credit lines for their buyers, even though it is obvious that much of this debt will never be repaid.

As with the US-Japan relationship, the US automobile ecosystem has been on a trajectory of divergence rather than convergence. The double increase in leverage (both in Mexico and through vendor financing offered by US auto finance firms) has replaced demand that comes from an organic rise in US living standards. The logical end result would be for car production in the US to be eliminated, and displaced “workers” given government handouts so they can buy Mexican-made vehicles from firms that can declare splendid earnings guaranteed by Uncle Sam.

I exaggerate for effect, but this example shows that the US’s “exorbitant privilege” has little to do with free market principles as it means the US (i) lacks a foreign trade constraint, and (ii) can force other countries to accept payment in dollars. Should either of these conditions end then the credit pyramid would implode. And indeed for decades commentators have fretted that the rest of the world may one day lose confidence in the US dollar as a store of value, resulting in soaring US interest rates and an economic crash – the Japanese, Chinese and a Brazilian supermodel have, at different times, all been touted as potential liquidators.

I never believed such scare stories so long as the US remained a superpower capable of corralling international respect. What worried me was a situation where the US, for domestic political reasons, pulled up the drawbridge and chose to pursue a current account surplus. Such an outcome was always going to be driven by Americans at large concluding that the global production system was being run against their interests.

The Emergence of Trumponomics

This was the backdrop for the emergence of “Trumponomics” and the fact that the US apparently wants to challenge China and Germany to become a surplus economy. To this end, US policymakers hope to tax imports at 20% and subsidize exports by a similar amount (i.e. what many export-focused economies do through VAT systems). Returning to Rueff’s monetary construct, Trump may just as well have said that he wanted to destroy the double pyramid of credit, which has grown relentlessly outside of the US since the mid-1960s.

Whatever the rights and wrongs of the global economic status quo, dismantling such a huge pyramid of credit threatens havoc for the financial system. Should the US return to a current account surplus, the rest of the world will move to an aggregated current account deficit. Since all other countries have a trade constraint, the system will inevitably start to contract, led by those nations already running a current account deficit. Such economies will have to tighten policy almost immediately, resulting in a big decline in domestic demand and so reduced imports.

The consequence will be that even “surplus” economies will move into a current account deficit and be forced into a tightening cycle. Those with an eye for history will have recognized a pattern as this chain of events was roughly what happened in the 1930s when another big pyramid of external credit collapsed – in this period, Britain was unable to regain its primacy at the center of the old gold standard system and the US was not willing to assume an economic leadership role. When the US sought a reflationary devaluation of the dollar in 1934 by constraining the sale of gold, it did so despite running a current account surplus. That decision aided the US’s economic recovery, but helped tip the German and French economies into a depression, ensuring the onset of World War II.

Fast forward to today and in some ways the ambition of US policymakers exceeds that of the 1930s. In addition to trade protection measures, Trump wants to ensure that dollars held outside of the US, especially those controlled by US multinationals, are sent back home. On the basis that history rhymes rather than being repeated, it is worth recalling that in the 1930s US banks aggressively recalled German loans, leading to the collapse of the German banking system.

There Is Nothing Immutable About a Dollar Standard

It is worth remembering that seemingly fixed elements of the global credit system developed in a haphazard fashion and can easily be reversed. For example, the Eurodollar market evolved after 1963 when John F Kennedy acted to reduce a growing US balance of payments deficit by taxing US investors who took dollars abroad to buy foreign securities. Subsequently, US dollars held outside of the US were mostly taxed at a lower rate than onshore dollars, and it was this “arbitrage” that allowed the City of London to develop and the external pyramid of credit to grow. If the tax system which encouraged US dollars to stay outside of the US disappears, then the US$1.2trn or so owned by US multinationals – the backbone of international credit markets – may be about to move back onshore. For the City of London, where most external dollars are managed day to day, the blowback could end up being far more serious than the loss of European Union passporting rights due to Brexit.

As a result, the future of international capital flows looks pretty gloomy. Indeed, on a flow basis the US dollar may increasingly become a collector’s item. This matters because many countries rely on US dollars being readily available to plug balance of payment deficits – according to a Bank of International Settlements report from 2015 the preceding decade saw non-US entities borrow some US$10 trillion.

Since the US can seemingly no longer be relied on to play the global shock absorber by expanding its current account deficit, the key headache for emerging economies may become servicing their stock of US dollar debt. So long as US short rates stayed low and the dollar exchange rate did not appreciate unduly (i.e. the situation since 2008), this was a manageable task. Yet in the event of the US current account starting to improve markedly (or even going into surplus), borrowers will find it impossible to repay principal as the US currency will have effectively been cornered, and there will not be enough dollars available to satisfy demand.

This situation will be exacerbated if the borrowed dollars were used to build factories whose output is sold in the US. The threatened imposition of a 20% surcharge on foreign-made imports to the US will render such factories unprofitable, but the debt will still have to be repaid. In short, the external part of the double pyramid of credit could involve subprime-type write-offs, only much larger.

Postscript: A modest proposal to save the world

If somebody were to ask my advice on how President-elect Trump should pursue his perfectly legitimate objectives without wrecking the global economy (and thereby ensure failure), I would suggest the following:

• The US should adopt market-friendly policies that boost the economy’s structural growth rate as is clearly the case with the program being put forward by Trump and the House Republicans.

• More difficult, but far more important than the first goal, Trump needs to pursue policies for which he was not elected; namely to prevent a collapse in the growth rate outside of the US.

The transmission mechanism for a bad cycle to unfold will be a far stronger US dollar; the inevitable result of ROIC in the US rising sharply. Such a situation will quickly hurt those fellows detailed above with heavy dollar debts as they never expected the US to actively reduce ROIC in the rest of the world. Should an acute dollar squeeze develop of a type last seen in the early 1980s then the exchange rate will soar, and ultimately the US will suffer due to US firms experiencing a sharply lower return on invested capital. For their part, US lenders will face huge defaults by stressed foreign borrowers.

To avoid such a scenario, the US should stand ready to buy, outright, the currencies of those countries facing payment difficulties. This will leave the US with huge foreign exchange reserves and the rest of the world with enough dollars to service their debts and meet payment obligations. As such, an implosion of the foreign pyramid of credit need not mean a collapse in the non-US money supply. Put another way, the US authorities should stand ready to build reserves in foreign currencies equivalent to the sum that vanishes through the credit contraction it has engendered.

The new US administration should thus launch a strategic fund ready to buy any foreign currency each time it becomes two standard deviations undervalued as measured by the OECD. Funding should come from the Federal Reserve at a market rate of interest and a stipulation should be made that the program is wound up as soon as the “new” foreign exchange reserves reach a level equal to about six months of US imports. The profits that will almost certainly accrue from such a program should be used directly to offset budget deficits that Trump’s fiscal expansion is likely to deliver.