Written by Lance Roberts, Clarity Financial

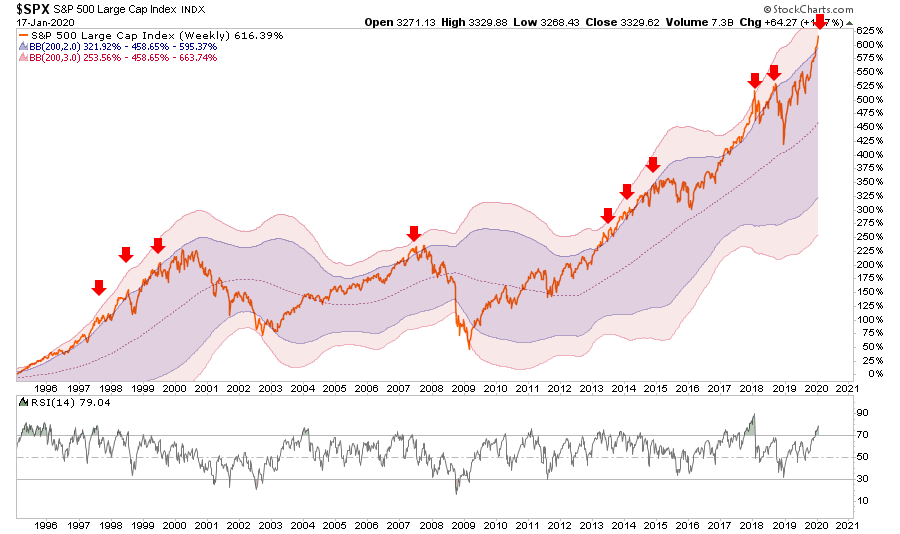

In last week’s missive, I discussed a couple of charts which suggested the markets are pushing limits which have previously resulted in fairly brutal reversions.

Please share this article – Go to very top of page, right hand side, for social media buttons.

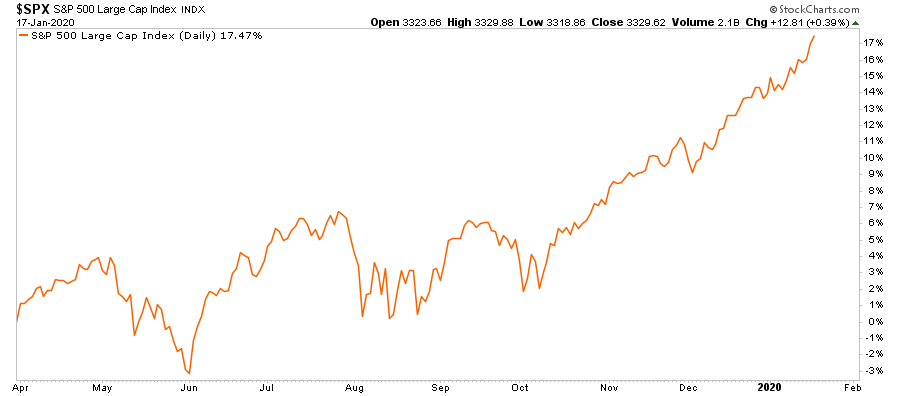

This week, the market pushed those deviations even further as the S&P 500 has now pushed into 3-standard deviation territory above the 200-WEEK moving average.

There have only been a few points over the last 25-years where such deviations from the long-term mean were prevalent. In every case, the extensions were met by a decline, sometimes mild, sometimes much more extreme.

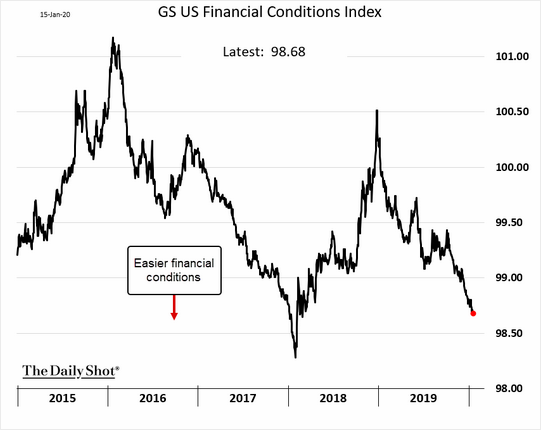

The defining difference between whether those declines were mild, or more extreme, was dependent on the trend of financial conditions. In 1999, 2007, and 2015, as shown in the chart below, financial conditions were being tightened, which led to more brutal contractions as liquidity was removed from the financial system.

Currently, the risk of a more “substantial decline,” is somewhat mitigated due to extremely easy financial conditions. However, such doesn’t mean a 5-10% correction is impossible, as such is well within market norms in any given year.

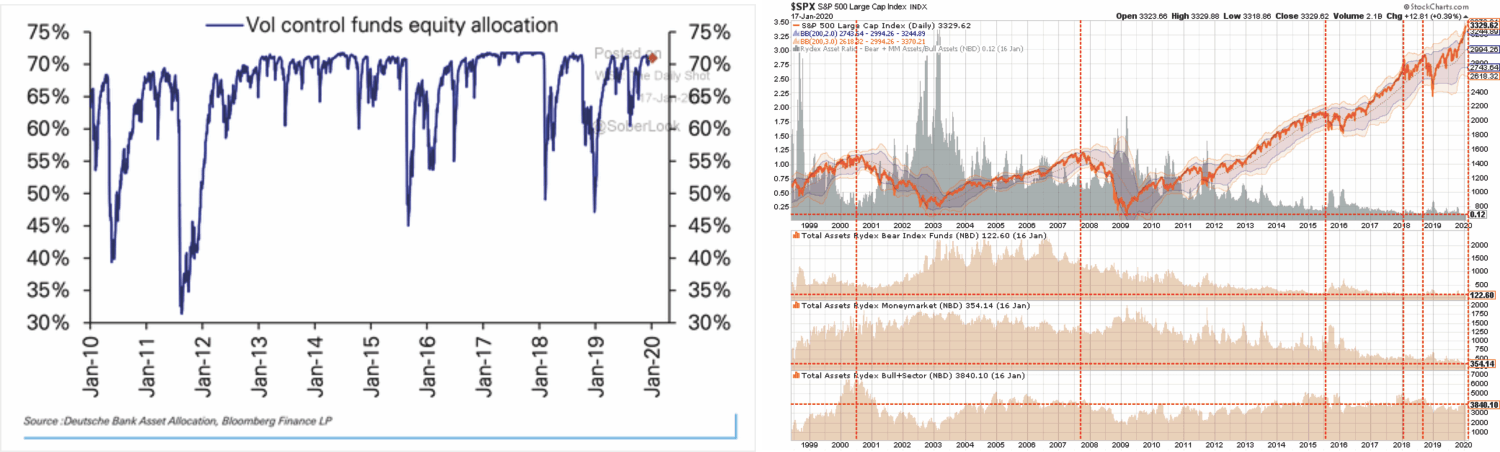

This is particularly the case given how extreme positioning by both institutions and individual investors has become. With investor cash and bearish positions at extreme lows, with prices extremely extended, a reversion to the mean is likely and could lean toward to the 10% range.

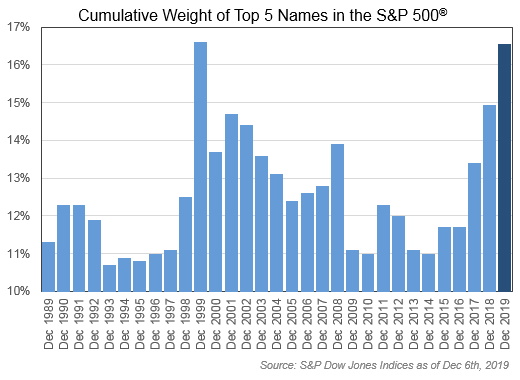

One of the other big concerns remains the concentration of positions driving markets higher. Lawrence Fuller analyzed this particular extreme in the market. (H/T G. O’Brien)

“One similarity between the Four Horseman of 2000 and the mega-caps of 2020 is their tremendous influence on the overall market, as can be seen below by their cumulative weightings. The weighting of today’s top five names is now 17.3%. I’m not suggesting that history is going to repeat itself, but often it rhymes.

If you lived and invested through the 1990s, as I did, then you’ll understand what I am talking about when I say that the dot-com boom was a sentiment-driven rally. I’m starting to see the same explanation for the current rally, as there really haven’t been any concrete fundamental developments to explain or validate it. The momentum stocks are rising in price day after day on hopes and expectations, and Wall Street analysts are happy hop on board for the ride, as usual.”

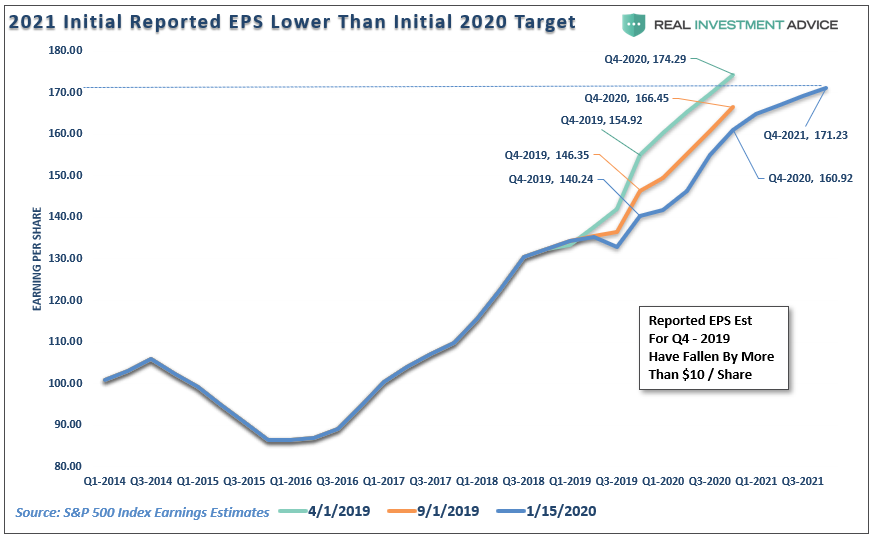

Lawrence is correct. There has not been a fundamental improvement to support the rise in the market currently. As shown in the chart below, S&P just released its 2021 estimates for the S&P 500, which is estimated to come in at $171/share.

What you should notice is that estimates for 2021 are now $3 LOWER than where estimates for the end of 2020 stood in April 2019. Importantly, between April 2019 and present, as earnings estimates were continually ratcheted lower, the S&P 500 index rose by 17.5%

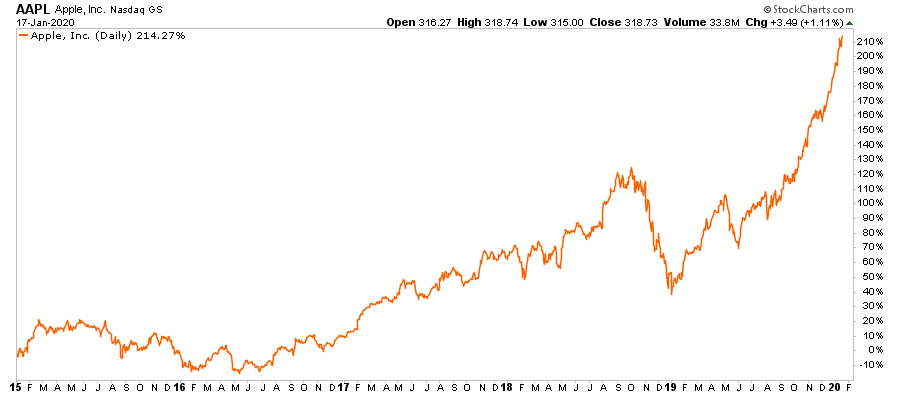

While Apple, which we own, is the “cheapest” of the “4-horseman” currently, it is only “cheap” because of rather aggressive share repurchases. Here are some interesting stats:

In the 5-years from 2015:

- Earnings per share (EPS) grew by just $2.69 per share or $0.53 per share annually.

- Sales only grew by $26.45 billion or $5.29 billion/year.

- Shares outstanding, however, declined by 1.13 billion

However, during that same 5-year period, Apple’s share price has risen by 210%.

The only reason Apple “appears” to be cheap is because of the massive infusion of capital used to reduce the number of shares outstanding. As a business, it is a great company, but it is a fully mature company, which is struggling to grow revenues. With a P/E of 27 and price-to-sales (P/S) ratio of 5.36, investors are grossly overpaying for the earnings growth and will likely be disappointed with future return prospects.

So why do we still own Apple? Because “fundamentals don’t matter” currently as the momentum chase, fueled by the Fed’s ongoing liquidity interventions, has led to a “runaway train.” But, understanding that eventually fundamentals will matter, is why we have taken profits out of our position twice since January 2019.

Just remember, “price is what you pay, value is what you get.”