Written by Lance Roberts, Clarity Financial

From last week:

“As we have noted over the past year, we have remained primarily allocated toward equity exposure, but have also worked around the edges hedging risk, raising stop levels, and remaining primarily domestic-focused. Given our outlook for a steeper yield curve earlier this year, we also shorted duration in our bond allocations, increased credit quality, and carried a slightly higher than normal level of cash.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

Currently, that remains the case again this week.

In September, we added exposure to Amazon (AMZN) and the Discretionary Sector (XLY) to participate with a “better than expected retail shopping season.”

Not surprisingly, this past week both surged on headlines from the media that retail sales were strong for the Christmas shopping season. However, this is probably not actually the case judging from real “retail sales” which were weak in November and will likely be weak in December. Nonetheless, the positions have performed well and will take profits as the decade ends.

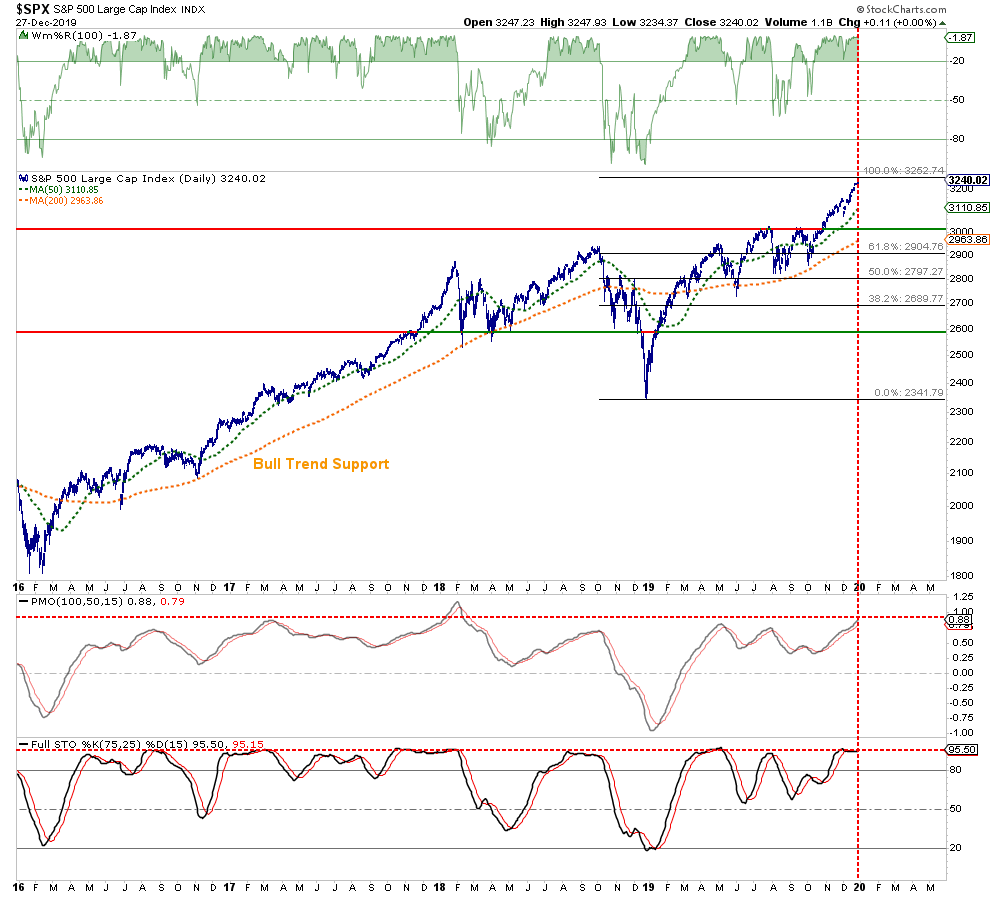

As noted last week, the markets are now even more extremely deviated from long-term trends. Combined with the extreme complacency and excess bullishness (as noted above), the risk of a correction remains high as we move into January or February. (More on this in our MacroView)

As noted below, the market has not been this overbought, extended, and deviated from long-term trends since the peak of the market in 2018. This isn’t necessarily a “bearish” note, but does suggest that the bulk of the gains are currently built into portfolios.

While none of this means the next “bear market” is lurking, it does suggest that a fairly decent 5-10% correction is likely over the next couple of months.

As we head into the final few trading days of the year, it is worth reminding you of “the rules” we penned in last week’s missive. These processes follow our basic rules of portfolio management, which you can apply to your portfolio as well to reduce overall volatility risk.

- Tighten up stop-loss levels to current support levels for each position.

- Hedge portfolios against major market declines.

- Take profits in positions that have been big winners

- Sell laggards and losers

- Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says, “sell everything and go to cash.”

Remember, our job as investors is pretty simple – protect our investment capital from short-term destruction, so we can play the long-term investment game.

Of course, if the Fed fails to “extinguish” whatever “blaze” they are currently battling, then we will begin to have a very different conversation about risk, positioning, and liquidity.