Written by Lance Roberts, Clarity Financial

“Fueling the markets are statements from past and present Fed Governors that are not only dovish but discuss a resumption of QE and negative interest rates. Former Fed Chairman, Janet Yellen, recently said the Fed needs more tools to battle a financial crisis. This is the same Janet Yellen that, in June of 2017, stated that she did not believe we would have a financial crisis in our lifetimes.

The Fed is sounding the alarms.” – Michael Lebowitz, RIAPRO.net (Try it FREE for 30-days)

Please share this article – Go to very top of page, right hand side, for social media buttons.

Last week, we discussed the market’s advance from the lows and why retesting old highs was quite probable. To wit:

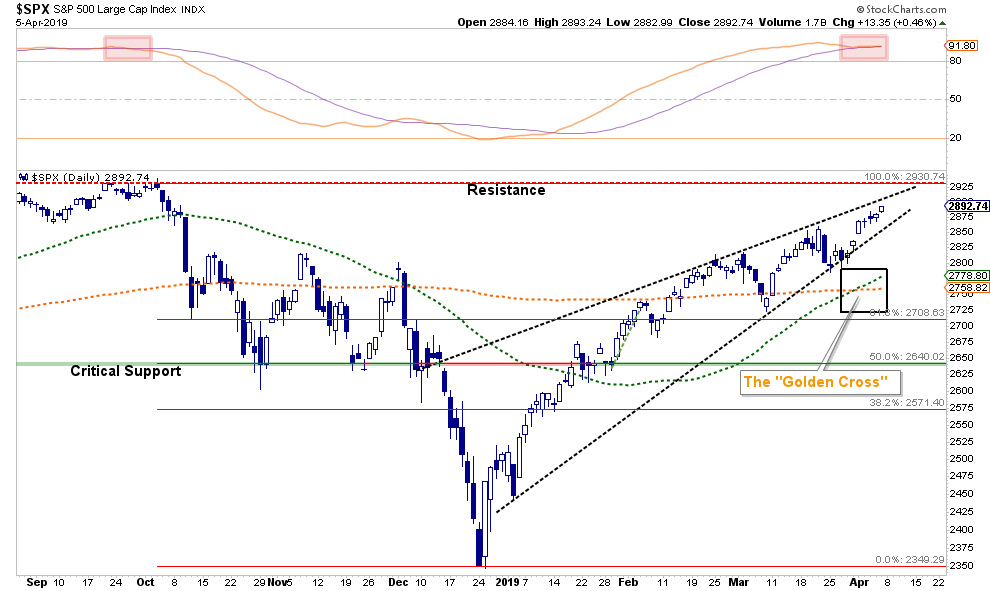

“The markets are close to registering a ‘golden cross.’ This is some of that technical ‘voodoo’ where the 50-day moving average (dma) crosses above the longer-term 200-dma. This ‘cross’ provides substantial support for stocks at that level and limits downside risk to some degree in the short-term.”

Not surprisingly, this headline on Friday:

“S&P Logs Longest Win Streak In 18-Months After Strong Jobs Report.”

Okay, two things are important here:

- If this is the longest “win streak” in 18-months that should tell you we are likely near the end of the run and not the beginning. That doesn’t mean the markets are going to crash, but a short-term correction is likely to provide a better risk-reward entry point.

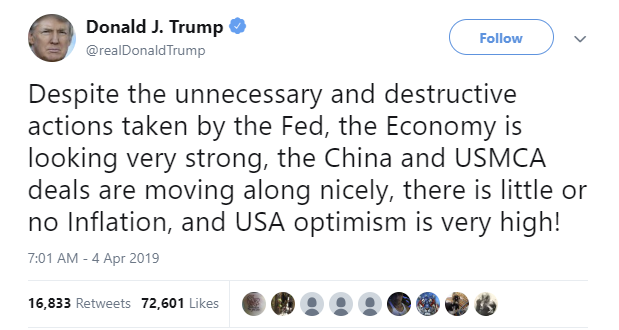

- The employment report wasn’t why the market rallied on Friday. In actuality, it was Trump’s comments about “trade,” the Fed needing lower rates, and the nomination of Herman Cain, another Trump supporter along with Stephen Moore, to the Federal Reserve Board.

So, stocks rallied once again on the same trade deal talk we have had for weeks with both China and the US claiming progress in talks and pushing for a rapid conclusion. While President Trump was talking up prospects for a “monumental” agreement, such will likely be an agreement in “name only” with no actions required until 2025. To wit:

“China would commit by 2025 to buy more U.S. commodities, including soybeans and energy products, and allow 100 percent foreign ownership for U.S. companies operating in China as a binding pledge that can trigger retaliation from the U.S. if left unfulfilled.”

If this turns out to be the case, President Trump may claim a victory for resolving a dispute he started in the first place but the markets will likely quickly see through the fiasco.

The real impetus behind the rally last week was the comments from Trump the Fed should drop interest rates and start more “Q.E.” As my dear Canadian friend, Victor Adair of Polar Futures Group, penned on Friday:

“‘Politics’ is increasingly on a collision course with Central Banks…and that may be become the ‘new’ most important driver of world markets.

On July 7/18 I wrote: Politics has replaced Central Banks as the most important driver of world markets according to Christopher Wood, financial analyst with CLSA, and I agree. It seems that for the last several years it was, ‘All about the Central Banks,’ but since Trump’s election the markets have been buffeted at least as much by political developments as by Central Bank actions. The recent Italian ‘existential crisis’ is a fine example of politics rattling the markets.

Today we have Trump constantly badgering Fed Chairman Powell, now calling for interest rate cuts and the resumption of QE…and proposing to nominate Stephen Moore and Herman Cain to the Fed board. (Not to mention Larry Kudlow calling for the Fed to cut interest rates by 50 bps.)

Is this really a Republican President effectively calling for the Fed to begin monetizing government deficits? We’ve come a long way from Fed Chair William Martin declaring that it was the Fed’s job ‘to take away the punch bowl just as the party gets going.'”

Importantly, and as we will discuss in more detail momentarily, lowering interest rates and introducing QE are tools the Fed will use when real weakness shows up in the economy. While Trump may want further “emergency measures,” he isn’t arguing the “need” for those measures very well.

The infighting though is setting up an serious collision between “Fed Independence” and the White House. Trump wants lower rates and Q.E. to continue to inflate asset prices since he has pegged the “success” of his Presidency on the stock market. (This was a mistake we have argued previously.) However, the Fed is already beginning to leak “hints” about needing to hike rates further due to the same reasons Trump tweets about – a still growing economy. (This is a reversal of the very policy comments which sparked the rebound from the December 24th lows.)

Cleveland Fed President Loretta Mester:

“Could we be done with policy rate increases this cycle? It is possible, but if the economy performs along the lines I think is the most likely case…the fed-funds rate may need to move a bit higher than current levels.”

Philadelphia Fed President Patrick Harker:

“I continue to be in ‘wait-and-see mode‘ with expectations of at most, one hike for 2019 and one for 2020.”

Those comments don’t align with a Fed eager to sit on the sidelines, reduce rates, or begin to inject further stimulus. Furthermore, Fed officials think the economy is in a good place with low unemployment and benign inflation. If they sense a slowdown, Fed officials would first act by trimming their benchmark interest rate.

Then, there is the question of its effectiveness anyway:

“The current belief is that QE4 will be implemented at the first hint of a more protracted downturn in the market. However, as we noted above, QE will likely only be employed when rate reductions aren’t enough. Such was noted in 2016 by David Reifschneider, deputy director of the division of research and statistics for the Federal Reserve Board in Washington, D.C., released a staff working paper entitled ‘Gauging The Ability Of The FOMC To Respond To Future Recessions.‘

The conclusion was simply this:

‘Simulations of the FRB/US model of a severe recession suggest that large-scale asset purchases and forward guidance about the future path of the federal funds rate should be able to provide enough additional accommodation to fully compensate for a more limited [ability] to cut short-term interest rates in most, but probably not all, circumstances.’

In other words, the Federal Reserve is rapidly becoming aware they have become caught in a liquidity trap keeping them unable to raise interest rates sufficiently to reload that particular policy tool. There are certainly growing indications, as discussed recently, the U.S. economy maybe be heading towards the next recession.

Interestingly, David compared three policy approaches to offset the next recession.

- Fed funds goes into negative territory but there is no breakdown in the structure of economic relationships.

- Fed funds returns to zero and keeps it there long enough for unemployment to return to baseline.

- Fed funds returns to zero and the FOMC augments it with additional $2-4 Trillion of QE and forward guidance.

In other words, the Fed is already factoring in a scenario in which a shock to the economy leads to additional QE of either $2 trillion, or in a worst-case scenario, $4 trillion, effectively doubling the current size of the Fed’s balance sheet.”

What investors should realize is that markets will be in a deep bear market, and recession, before QE would be restarted. However, that appears to be a point lost on market participants currently. As Victor concluded:

“The benchmark S+P 500 Index (my bellwether for global risk appetite) had its best Q1 performance in over 20 years and is now only a few percentage points away from All-Time-Highs. Monetary conditions are easy, FOMO and TINA are the key words while DeMark technical indicators and sentiment measures are at extremes. Implied Volatility keeps falling as stocks rally…currently at one month lows.”

He is right, But we are only one-quarter of the way through the year, and while stocks could well reach all-time highs, the potential for a decent correction has been put into place.

“A veteran Chicago trader told me the other day that, ‘stocks are bid because there are no alternatives to lower interest rates.’ He followed that up a few days later with, ‘The only people buying here are people NIT using their own capital.’” – Victor Adair

Risks very much outweighs reward at this juncture and there is no real victory to be had by chasing markets currently.

While we are currently maintaining our long-equity exposure, we did take actions last week to rebalance risk, take profits, and adjust holdings to offset an increase in short-term volatility.

If you don’t know what to do, that is okay.

Cash now has a yield equivalent to inflation with no volatility and no risk of loss. What more could you ask for if you aren’t letting “greed” dictate your investing?