Written by Lance Roberts, Clarity Financial

My old friend David Rosenberg has an interesting comment this a week ago.

“The January high in the S&P 500 will prove to be the peak of the bull market and a U.S. recession may start in the next 12 months. Cycles die, and you know how they die? Because the Fed puts a bullet in its forehead.”

Please share this article – Go to very top of page, right hand side, for social media buttons.

He is right. The only question is the timing.

One thing this market has become known for is its resilience. Regardless of the event, “hope” combined with a lot of Central Bank activity has kept the markets pushing higher. But, all good things do come to an end, and history shows the Fed has always led the “last charge of the light brigade.”

For those unfamiliar with the story, the “Charge of the Light Brigade” was a charge of British light cavalry led by Lord Cardigan against Russian forces during the Battle of Balaclava in 1854, during the Crimean War. Lord Raglan, the overall commander of the British forces, had intended to send the Light Brigade to prevent the Russians removing captured guns from overrun Turkish positions, a task well-suited to light cavalry. However, due to miscommunication in the chain of command, the Light Brigade was instead sent on a frontal assault against a different artillery battery, one well-prepared with excellent fields of defensive fire.

Although the Light Brigade reached the battery under withering direct fire and scattered some of the gunners, the badly mauled brigade was forced to retreat immediately. Thus, the assault ended with very high British casualties and no decisive gains. War correspondent William Russell, who witnessed the battle, declared:

“Our Light Brigade was annihilated by their own rashness, and by the brutality of a ferocious enemy.”

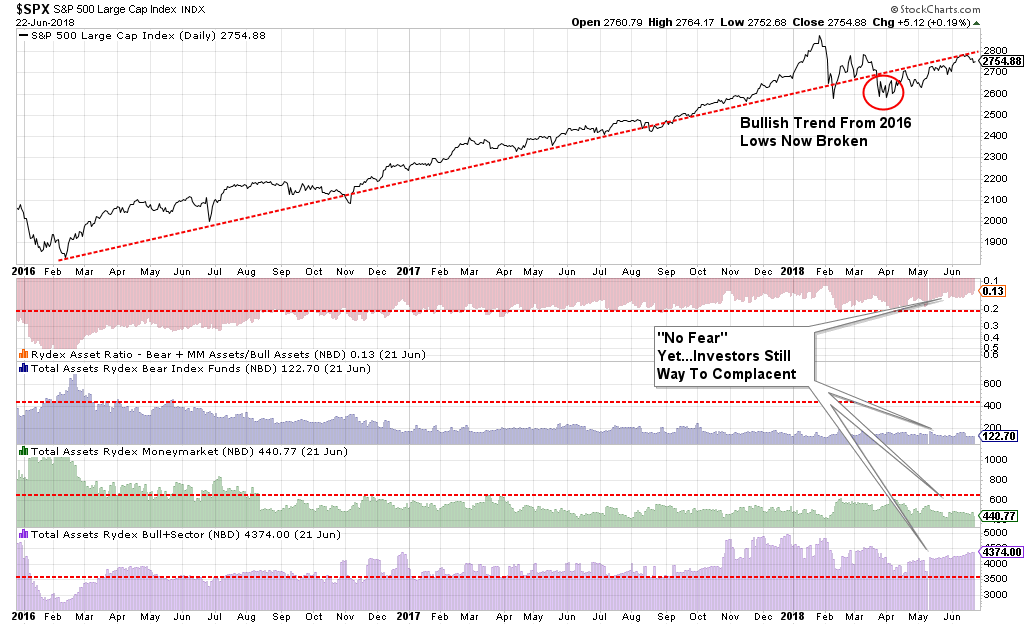

This current set up is very much like what faced the British Calvary. A market that is overly bullish, overly complacent and overly valued has already had horrible outcomes for those that charged headlong into it when similar conditions previously prevailed. As the chart below shows, “bears” have gone into complete hibernation.

The backdrop of the market currently is vastly different than it was during the “taper tantrum” in 2015-2016, or during the corrections following the end of QE1 and QE2. In those previous cases, the Federal Reserve was directly injecting liquidity and managing expectations of long-term accommodative support. Valuations had been through a fairly significant reversion, and expectations had been extinguished.

None of that support exists currently and, in our opinion, investors are largely ignoring the extreme conditions which currently exist. As David Rosenberg noted:

“We are seeing a significant shift in the markets. The Fed was responsible for 1,000 rally points this cycle so we have to pay attention to what happens when the movie runs backwards.”

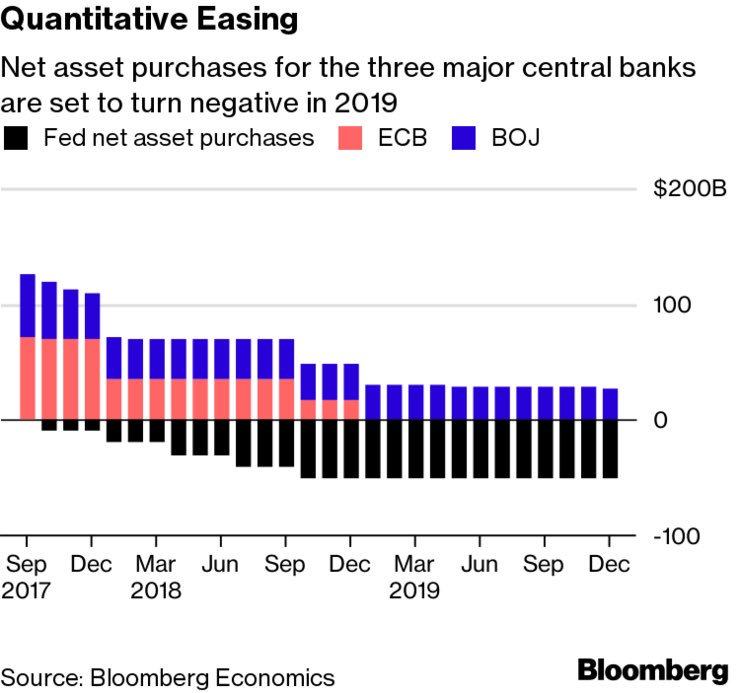

This was a point I made last week, that it isn’t just the Fed extracting liquidity and removing accommodation, it has now gone global.

“Combine a “trade war” with a Federal Reserve intent on removing monetary accommodation, both through higher rates and reduction in liquidity, and the market becomes much more exposed to an unexpected exogenous event which sparks a credit-related event. (Of course, it isn’t just the Fed, but also the BOJ and ECB.)”

There is a reasonably high possibility, the bull market that started in 2009 is coming to an end. We may not know for a week, a month or even possibly a couple of quarters. Topping processes in markets can take a very long time.

If I am right, the conservative stance and hedges in portfolios will protect capital in the short-term. The reduced volatility allows for a logical approach to further adjustments as a correction becomes more apparent. (The goal is not to be forced into a “panic selling” situation.)

If I am wrong, and the bull market resumes, we simply remove hedges and reallocate equity exposure.

“There is little risk, in managing risk.”

Whether it is sooner, or later, the current run-up in stocks will end very much the same as they always have with investors “annihilated by their own rashness and the brutality of a ferocious enemy.”

For now, investors race forward with swords drawn, shouting the “bull market” battle cry in the face of insurmountable odds solely with a conviction of invincibility.

But such is the nature of every bull market cycle in throughout history.

Invest accordingly.