Written by Lance Roberts, Clarity Financial

As I penned last weekend:

“If the market corrects, OR the economy hits a speed bump, OR something happens in the Eurozone, OR…OR…OR…the covering of short positions in bonds will cause an extremely fast drop in yields.

Sure, anything can happen. If yields on the 10-year Treasury break above 3% it will be coincident with a sharp rise in consumer spending, wages, inflationary pressures that are broad based and surging economic growth. In such a case it will make sense to reduce bond holdings in favor of equities.

However, given the fact we are already in the 3rd longest economic expansion in history, combined with the second highest levels of valuation on stocks, the odds of such an outcome are extremely low.”

But here is another reason to stay long bonds.

Currently, as noted by ZeroHedge last Friday:

“With political and economic policy uncertainty at record highs and equity market valuations near record highs, we have one question: which market – interest rates or stocks – is right about ‘risk’ ahead?”

Currently, there are record shorts on volatility which suggest there is little expectation of a market correction currently. In other words, everyone is now on the long-side of the proverbial “boat.”

So, why own bonds?

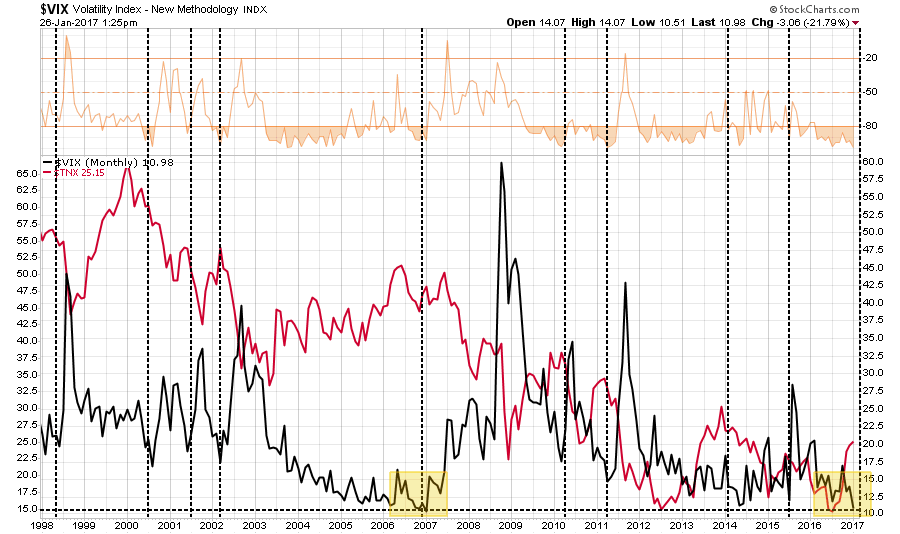

As shown in the chart below, interest rates are negatively correlated to the volatility index. With the extreme net short positioning in bonds, a market correction would spark a rotation from “risk” to “safety” pushing rates towards 2%. However, such a reversal would also trigger a panic-driven short-covering trade which would likely push rates even lower towards 1.5%.

That thought was also discussed recently at the Macro Man blog:

“We still think that Mr. Bond will have a soft landing this time. In fact, now that the Inaugural is behind us, with all of its ‘Sound and Fury signifying nothing’, Mr. Market will likely undertake a more cerebral evaluation of the likelihood of 4, 5 and 6% US GDP in 2017.

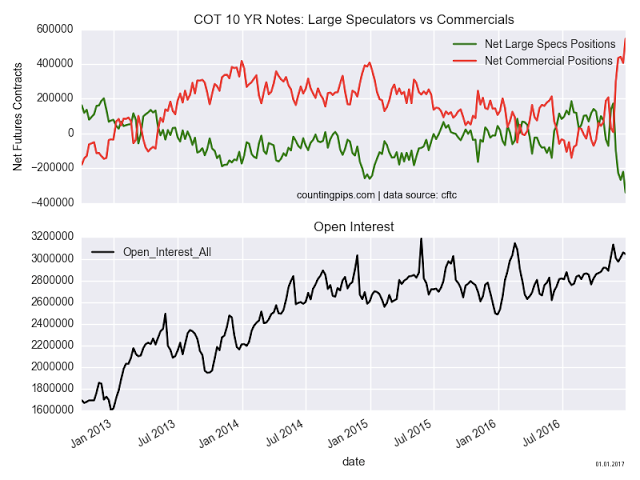

A renewed safe haven bid for Mr. Bond and other fixed income assets seems certain before long, as Real Money and commercials have increased their net longs. The speculative community remains extremely short bonds, providing a mechanism to accelerate any recovery in fixed income once it gathers speed, eventually forcing a surprising number of concealed shorts to return to a more neutral positioning in Treasuries.”

Currently, we remain long bonds as a hedge until the abnormalities are reversed.