Written by Lance Roberts, Clarity Financial

Continue To Prepare

While we await a better entry point, assuming the recent bullish action is maintained, it is important to continue to prepare portfolios for further action.

I have often equated portfolio management to tending a garden in the past. Like a garden we must:

Prepare the soil (accumulate enough cash to build a properly diversified allocation)

Plant according to the season (build the allocation given the right “season”)

Water and fertilize (add cash regularly to the portfolio for buying opportunities)

Weed (sell loser and laggards, weeds will eventually “choke” off the other plants)

Harvest (take profits regularly otherwise “the bounty rots on the vine”)

Plant again according to the season (add new investments at the right time)

So, with this analogy in mind, here are the actions to continue taking to prepare portfolios for the next set of actions:

Step 1) Clean Up Your Portfolio

Tighten up stop-loss levels to current support levels for each position.

Hedge portfolios against major market declines.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.

Step 2) Compare Your Portfolio Allocation To The Model Allocation.

Determine areas requiring new or increased exposure.

Determine how many shares need to be purchased to fill allocation requirements.

Determine cash requirements to make purchases.

Re-examine portfolio to rebalance and raise sufficient cash for requirements.

Determine entry price levels for each new position.

Determine “stop loss” levels for each position.

Determine “sell/profit taking” levels for each position.

(Note: the primary rule of investing that should NEVER be broken is: “Never invest money without knowing where you are going to sell if you are wrong, and if you are right.”)

Step 3) Have positions ready to execute accordingly given the proper market set up. In this case, we are looking for a pullback to reduce the extreme overbought condition of the market without violating any major levels of support.

IMPORTANT NOTE: Taking these actions has TWO specific benefits depending on what happens in the market next.

If the market pulls back to support and confirms the recent breakout is indeed a continuation of the bullish long-term trend, the actions have cleared out the “weeds” and allowed for “new planting” to benefit from the next advance.

If the recent breakout turns out to be a “head fake,” then the reduction of “risk” protects the portfolio against any substantial decline.

No one knows for sure where markets are headed in the next week, much less the next month, quarter, year, or five years. What we do know is that not managing risk in portfolios to hedge against something going wrong is far more detrimental to the achievement of long-term investment goals due to the inability to recover the “time” lost getting back to even.

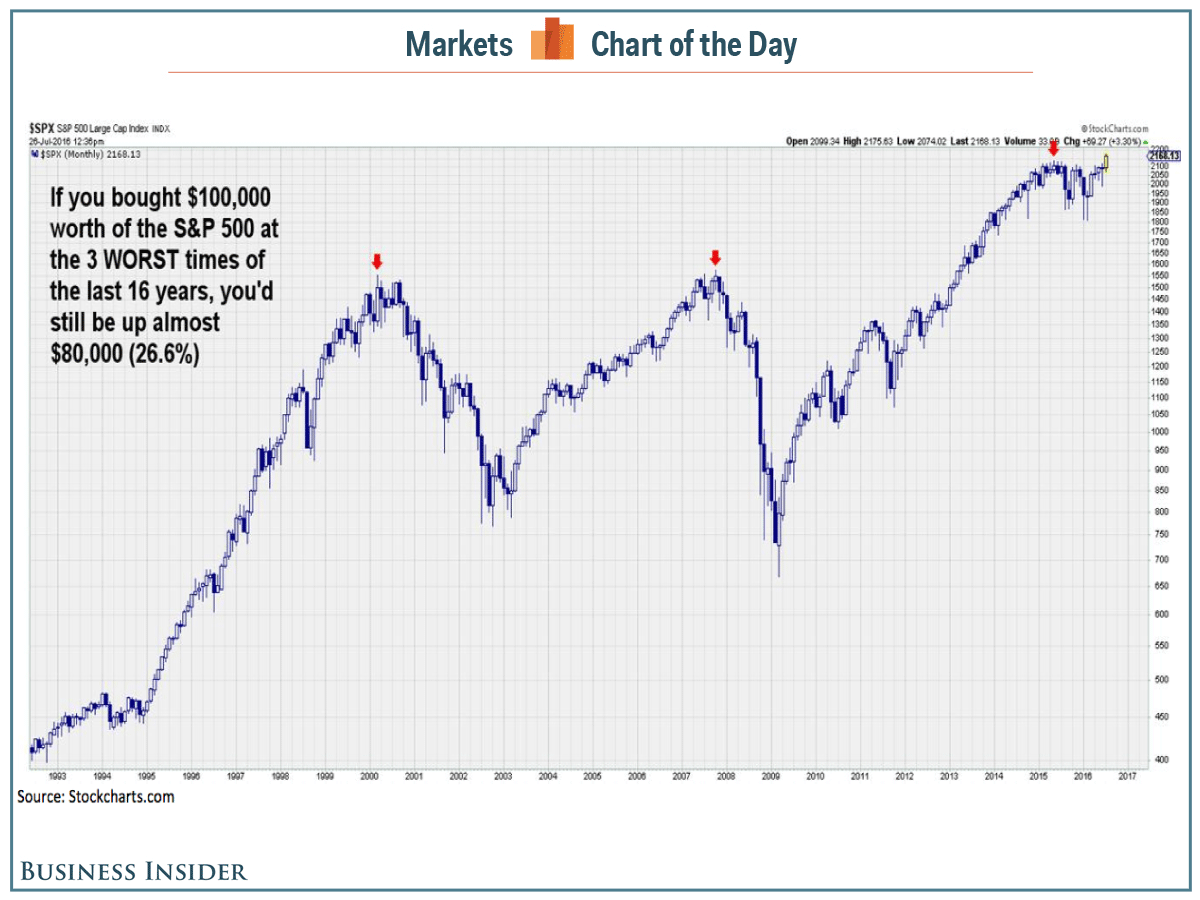

This fallacy was clearly pointed out this past week in probably what ranks as the worst bit of financial analysis put out this year by Myles Udland via BI

“But even if you bought stocks only right before the 2000 and 2008 market tops – and then bought stocks again only when they got back to May 2015 highs – you’d still be making money.

This chart, which comes to use from Raymond James analyst Andrew Adams, shows that $100,000 spent on the S&P 500 at each of these three most recent tops still nets investors an $80,000 gain (or 26.6%) over this period.”

Okay. Let’s make a couple of real-world assumptions. Most people, by the time they enough to effectively invest and actually start doing so, is about 45 years of age. This gives them about 20-years to their retirement goal.

Here’s the problem, since most people “assume” the markets return 8% a year, a myth previously debunked here, a 26% return over 16-years is just 1.625% annually. Buying a bond fund would have yielded in excess of a 150% rate of return or 9.375% annually with substantially less volatility.

“Getting Back To Even” never has been, and never will be, a successful investment strategy.

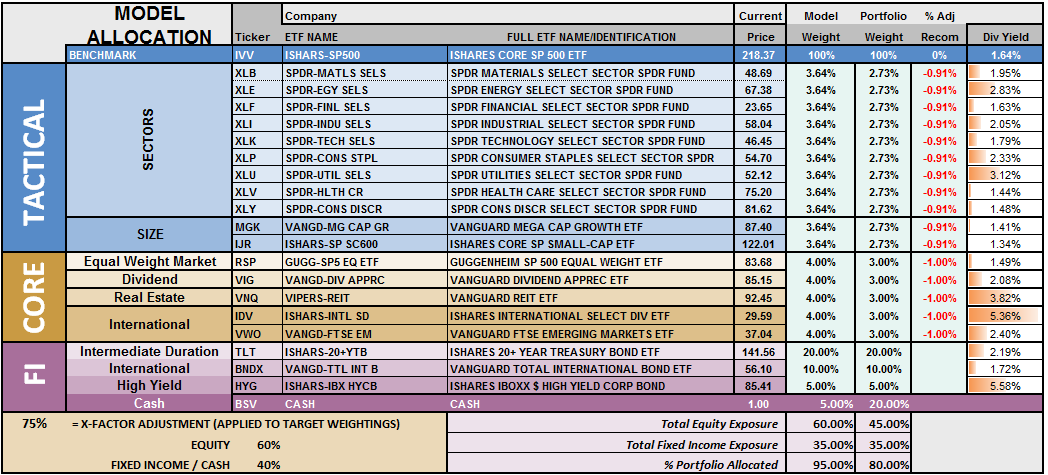

S.A.R.M. Sector Analysis & Weighting

The current risk weighting remains at 50% this week but will increase to 75% given appropriate market conditions.

Again, we must be given the right “set up” to increase equity allocations. Begin by “averaging up” in existing holdings to match model allocation and weights. When, and IF, the market confirms the continuation of the “bullish trend,” then begin adding new holdings to the model.

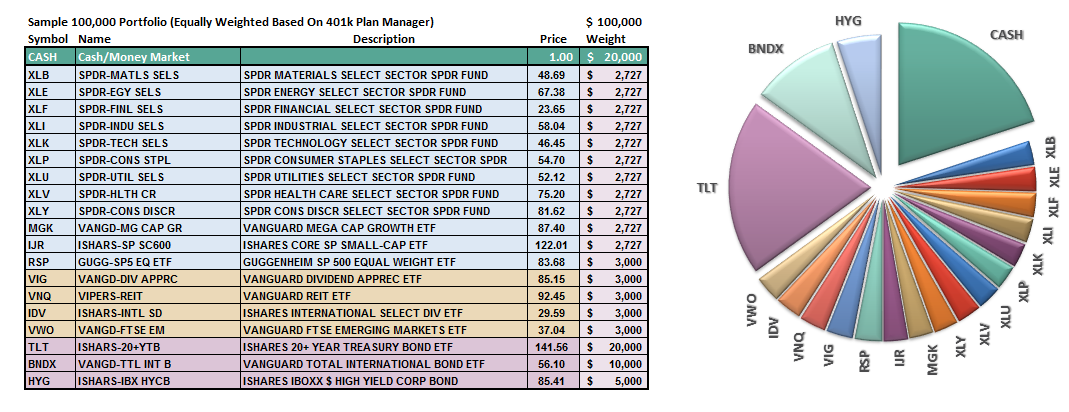

(Note: This is an equally weighted model example and may differ from discussions of overweighting/underweighting specific sectors or holdings.)

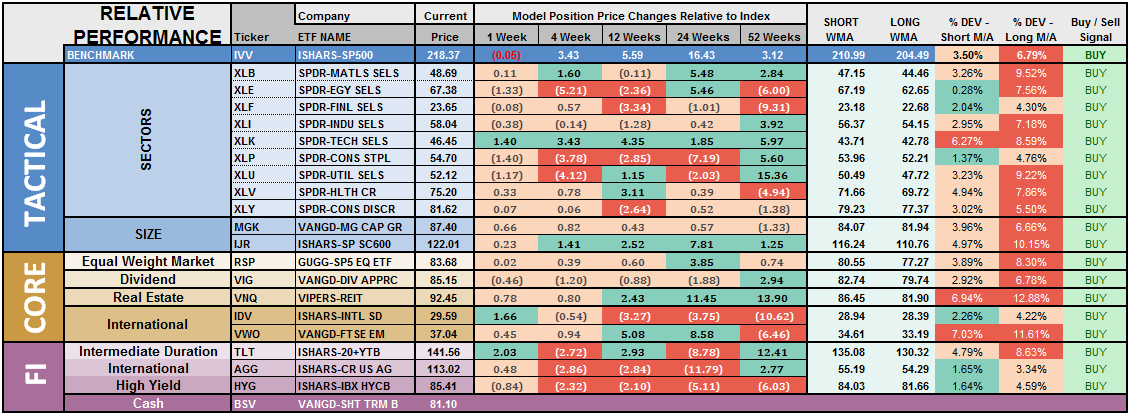

Relative performance of each sector of the model as compared to the S&P 500 is shown below. The table compares each position in the model relative to the benchmark over a 1, 4, 12, 24 and 52-week basis.

Historically speaking, sectors that are leading the markets higher continue to do so in the short-term and vice-versa. The relative improvement or weakness of each sector relative to index over time can show where money is flowing into and out of. Normally, these performance changes signal a change that last several weeks.

The last column is a sector specific “buy/sell” signal which is simply when the short-term weekly moving average has crossed above or below the long-term weekly average. The number of sectors on “buy signals” has improved from just 2 several weeks ago to 19 this past week.

The risk-adjusted equally weighted model has been increased to 75%. However, as stated above, a pullback in the markets is needed before making any changes.

Such an increase will change model allocations to:

20% Cash

35% Bonds

45% in Equities.

As always, this is just a guide, not a recommendation. It is completely OKAY if your current allocation to cash is different based on your personal risk tolerance, time frames, and goals.

For longer-term investors, we still need to see improvement in the fundamental and economic backdrop to support the resumption of a long-term bullish trend. Currently, there is no evidence of that occurring.