by Michael Clark

In 2007 Nassim Taleb became famous when he published his book “The Black Swan: The Impact of the Highly Improbable” as a picture of what moves history, art, politics, science: the unexpected ignition.

Taleb considered the 2001 attacks by Muslim extremists as a ‘black swan incident’. I don’t think he considered the global meltdown of stocks and markets in 2008 and the subsequent slide into depression as a black swan incident. We are still sliding, as a matter of fact. Those who have read my writing know that I perceive the sliding into depression began in 2001, with the Twin Towers attack a perfect symbol of the transition from expansion and Day into depression and Night. The slide into depression will not reach destructive satiation until 2019, at which time Destruction will reach its peak, and Creation will reach its bottom.

I hesitate to call the strong Dollar a new Black Swan Event, since by Taleb’s definition, the black swan is an event that cannot be predicted or even expected. The strong Dollar as a deflationary world-crumpling device is quite well-known, in fact — but not recognized publicly, since to recognize this would be tantamount to calling ourselves the Devil and accepting the fact that expansion of wealth and civilization, itself, is a temporary thing at best, always subject to the karmic justice implied by the strong Dollar’s pervasive anti-inflationary bias.

Taleb writes:

What we call here a Black Swan (and capitalize it) is an event with the following three attributes.

First, it is an outlier, as it lies outside the realm of regular expectations, because nothing in the past can convincingly point to its possibility. Second, it carries an extreme ‘impact’. Third, in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.

I stop and summarize the triplet: rarity, extreme ‘impact’, and retrospective (though not prospective) predictability. A small number of Black Swans explains almost everything in our world, from the success of ideas and religions, to the dynamics of historical events, to elements of our own personal lives.

In two major novels I am currently writing, CROSS EXAMINATION and 2 AND 1/2 LOVES, I ascribe the role of the SWAN to Venus, the Goddess of Love — yes, the planet Venus, but much more — who gives us life and body in her aspect as the Morning Star (Venus – Lucifer, DAWN) and takes away that Life in her aspect the Evening Star (Venus-Hesperus, DUSK). She is the White Swan when she brings us Life in physical form (which is also, paradoxically, a spiritual death sentence); and she is the Black Swan when she brings us Death, physical Death, which again also represents a Spiritual Life.

Venus is situated in the zodiac in two planets, in Taurus (where she is the Morning Star) and in Libra (where she is the Evening Star). As the Death Star she is very much unexpected. During my own life she appeared to me twice, in 1976, as a beautiful woman with whom I fell madly in love — married two weeks before we met — which marital status eventually generated the death of me; then again in 2008, when she appeared as an old crone, a landlady, from whom I had been renting since 1992, nearly 17 years, who gave me a month to get out of her house so she could expand it and sell it or rent it at a higher price, agitated by the money-lust sweeping through Eugene, Oregon (and most other US towns and cities) triggered by the devilish US Housing Bubble.

In both cases, these events were unexpected, could not really be predicted, and led to a prolonged death experience (my own), depression, a religious conversion stage and Dantean journey through the very black Inferno or Underworld as a condition of rebirth or resurrection. A descent into the alchemical melting pot, from which I was to go in a base metal and to come out a new-born pure golden soul. The first resurrection did occur; the second is implied, on which I am currently counting.

The white swan in this scenario was the woman who became my wife in 1995 (in Taurus, right on time) in line with the mystical Time-Structure I began to discover in Hanoi, in 2010, after my ‘second death’. My wife gave me back my life, my body, and was, quite literally, the Biblical Tree of Life, as the Black Swans had been, and just as literally, the Biblical Tree of Knowledge of Death (Good and Evil — alienation is the fruit of this Tree of Death).

The dissolution of the Soviet Union Taleb calls a Black Swan Event. Something which could not really be predicted. I’m not certain of this; many writers predicted exactly that, for decades. They did not predict the exact date of that empire’s demise, however; perhaps the date of the collapse is the Black Swan Event’s ‘unpredictability’.

My system ‘predicted’ that the anti-matter Force of Destruction — Eastern Communism in the last cycle — gained power from 1965-1983; 1983 was the apex of the Deconstruction of the World Energy (entropy, with reference to the Creator Energy). 1992 was the point at which the Light and the Shadow were at equal strength, from which the Shadow fell into disarray, through 2001, and was reborn in that year as the Islamic Force of Deconstruction.

The actual ‘wounding’ of the Russian Communists came in the year (roughly the year) 1983 (as the next ‘wounding’ of the Creative Force came in 2001, the year of ‘the light’s’ apex) (remember light is matter — so the creators represent the force of materialism, which to the Russian Communists, to the Fascists in 1929-1947, and to the Islamic Fascists in 2001-2019, and some Western religions also, is as the Demiurge, the Principle of Evil) — and is directly connected with the Russian Air Force’s destruction of a South Korean commercial aircraft (KAL-007, September 1, 1983) killing all 269 people aboard.

Earlier, May 13, 1981, Pope John Paul II, was shot four times and nearly killed in a conspiracy many believed was instigated by Russian agents through Bulgarian agents to punish the Pope for his role in the challenge of Russian/Communist rule in his native Poland.

Western response to these two events was to prepare for a nuclear war with Russia; and the Queen of England even prepared and practiced a radio-broadcast declaration of war against Russia, and the beginning of World War III.

In 1989, the Berlin Wall collapsed, an edifice of the World Destroyer’s fortress mentality, a symbol of its black-hole paranoia.

Predictable? Not by ordinary measures probably. From 1983 to 2001, the Shadow Principle falls apart, as the West, the Substance or Matter Principle fell apart from 1965-1983, and is falling apart today, from 2001-2019.

Isis and other groups of Deconstruction, or Anti-Matter, Forces, Islamic and others, will continue to get stronger and more frightening and threatening to Civilization through 2019. 2019 will be their peak in power. This will be the point at which the West becomes most desperate (from this root for ‘despair’) to wage a war of survival against Islam. If Islam fashions an alliance with non-Islamic Eastern powerhouses, Russia and China, then this war will probably become World War III. I believe Russia will resist being pulled in to such an alliance. Putin seems to understand that the Communist-Capitalist dialectic is the Old World antagonism, for the backward looking. Putin seems to recognize that the next war will be religious, with the religious West taking on the religious East, Islam. China may become aligned with Islam, much to her regret.

It is interesting that Isis, the Egyptian Goddess, or Female Principle, was an earlier name for Venus — Isis being the Black Swan, the Death of the Male Principle, Time, Civilization, the West, the force of World Creation: Isis (or Venus) rises to power throughout the entire Night-Cycle (1965-1983; 2001-2019….): it is symbolically significant that the Islamic extremists, anti-matter warriors as they clearly are, should take the name of ISIS for their Moon-God reaction against the Sun-God Western empire. The Night-Cycle is represented as being begun by the eclipse of the Sun by the Moon; the Day-Cycle, symbolically, is represented by the eclipse of the Moon by the Sun. A specific eclipse returns to the Earth every 18 years (the Saros Cycle, returning every 18 years, 11 days, 8 hours) — and this continues for the entire life of that eclipse, which lasts for 252 years.

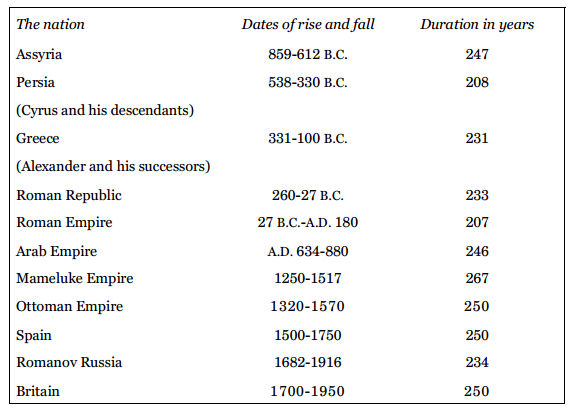

Sir John Glubb in THE FATE OF EMPIRES prescribes the average life of empires as about 250 years (which I round off to 252 years). I’m not arguing that this is true (I wonder at Sir Glubb’s division of Rome into two different empires of 250 years). But it is an interesting comparison.

I am getting off point, which I do often. Digressions are a generally annoying but harmless side-effect of non-linear thinking.

The Black Swan Event is unpredictable and unique. So how can I suggest that the Strong Dollar is a Black Swan Event?

Let’s look again at Taleb’s published criteria. The event is an outlier, or is outside the realm of regular expectations. Clearly a strong Dollar is not outside the realm of regular expectations; however the strong Dollar as a trigger of World Deflation may be outside of regular expectations. I do not think that most business school’s teach that the strong Dollar will destroy the global economy. Few famous economists make this principle a major point in their economic theories. Still, the U.S. Dollar rallied in 1980-83, and Latin America collapsed in a debt crisis; the Dollar rallied from 1998-2003, helping to trigger the collapse of the NASDAQ stock bubble in America, the Asian Currency-and-Debt crisis, and the Russian Debt-Default Crisis.

The Fed subsequently calmed the markets by lowering interest rates in order to weaken the Dollar again. But then in 2008 the Dollar began to march higher again, leading to (triggering?) the collapse of the Global Economy and stock markets the following year.

Today, as the U.S. Dollar climbs, oil crashes, commodities crash, and stocks begin to crash. This is not accidental, and not unpredictable. The FED knows all about the Dollar deflationary impact. That’s what QE was all about. In fact, everything the FED has done since 2000, has been to fight the US Dollar’s deflationary impact.

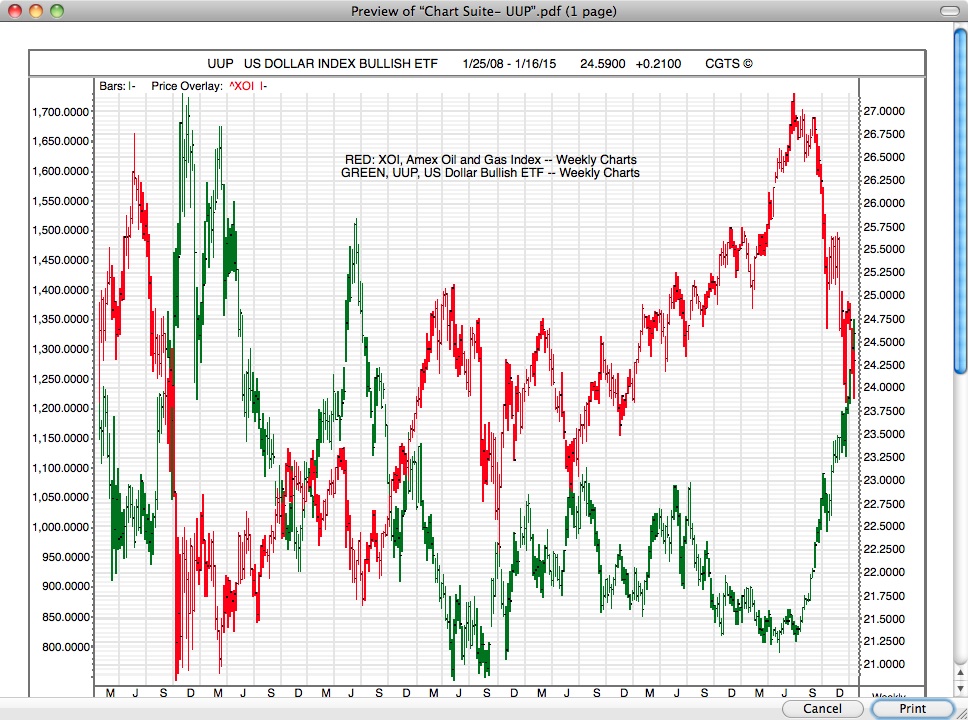

Below one sees the deflationary impact of the strong dollar on oil. As the US Dollar rises (green line) the oil complex (XOI in the chart) falls.

(click to enlarge)

The US Dollar is an outlier; it’s strength brings chaos to the world. However, its weakness brings order and wealth and expansion and surfeit and debt and insolvency to the world. Economists tell us not to worry because we have no inflation. Are they stupid; or are they just counting on us being stupid enough to believe them?

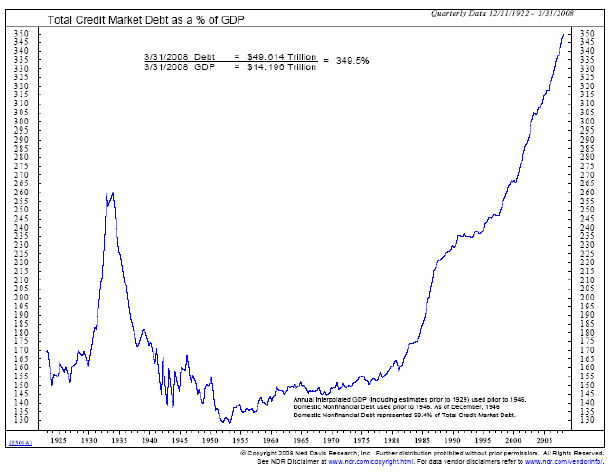

The picture below is a picture of inflation, a picture of debt inflation. When economists argue that inflated debt is not inflation, according to their definition, I say that they need to change their definition.

What does Taleb say? Taleb writes:

“If you hear a “prominent” economist using the word ‘equilibrium,’ or ‘normal distribution,’ [to which I would add the word “inflation”] do not argue with him; just ignore him, or try to put a rat down his shirt.”

Economists are politicians, and should be treated as politicians — listened to with a healthy does of skepticism if not cynicism, and sometimes should be given the ‘rat-shirt’ treatment. Ben Bernanke should have been given the ‘rat-shirt’ treatment on more occasions than one.

The strong Dollar may be accepted as an ‘outlier’ — but to this Taleb adds “nothing in the past can convincingly point to its possibility”. This is clearly not true. I just pointed to two historical periods where the response was quite obvious, which was repeated in 2008-9, and seems to be being repeated today, in 2015. In fact, it was not until QE1, QE2, and QE3 in the US, and ZIRP for good measure, that ‘healthy’ inflation of assets began again.

Of course, such inflation of assets is and was not healthy — it is illusory, deadly, and perhaps criminal. History will perhaps judge on its criminality, if we ever elect a president who wishes to countenance this possibility and fund such necessary investigations.

The second Taleb criteria is that “ it carries an extreme ‘impact“. No question about this. The global economy is a house of cards that always seems to fold when the price of the Dollar increases significantly.

Third Taleb criteria:

“in spite of its outlier status, human nature makes us concoct explanations for its occurrence after the fact, making it explainable and predictable.” Well, that’s what I am doing today, isn’t it?

Here is my prediction. Unless the world, through the FED and other central banks, acts to curb US Dollar strength (can they do that at this point?), the global deflation which we have been pretending wasn’t a necessity, a LAW, which instead perhaps (we pretended) was only a remote possibility, since 2001, one we could defeat through will and monetary inflation hocus-pocus (QE Infinity) will finally be allowed to do its work, and bring us back around on the wheel again toward RESET and eventually toward organic economic growth again.

Be clear: I’m saying the strong Dollar is GOOD and NECESSARY at this point in the cycle, and is needed. Higher interest rates have been needed since 2001. The strong Dollar, deflationary effect and all, is the right path for the world today. But that does not mean it will be painless. Deflation does not generate growth. Deflation is the opposite of growth. But deflation helps to reduce debt, which is an essential ingredient for the re-ignition of growth. How does deflation help to reduced debt? Through defaults and bankruptcies.

Higher interest rates will assist in this process of 1) debt destruction, cleansing, purification of the old sins of fake inflation and theft of public money (jail time will also help here); 2) safe growth of wealth through invested savings and interest rate appreciation.

There are two stages in the Business Cycle: 1) Growth, Inflation of the Global Economy, which is the Spending Cycle; 2) Rest, Deflation of the Global Economy, which is the Saving Cycle. The Saving Cycle is designed to save us from the excesses of the Spending Cycle (and the strong Dollar is essential in this); the Spending Cycle will also, eventually, after the Saving Cycle has run its course, save us from the deflationary devastation of the Saving Cycle. The Spending Cycle is the Day, and is guided by a lowering of interest rates; the Saving Cycle is the Night, which is guided and directed by a raising of interest rates.

We need to honor both cycles. We need to give up our selfish, willful, childish view that Growth can be perpetual, and will follow human power and will. Growth is periodical; always has been; always will be.

The FED is going to have to resist panic from many quarters if it is going to allow the Dollar or even assist the Dollar in appreciating, because the strong Dollar will demolish the Emerging Market first, and then will play havoc with Western banks, who are heavily invested in Emerging Market debt.

The fake inflation supplied by QE and ZIRP was and is a stalling tactic that has gone on much too long. Fake inflation is furthered by a weak Dollar. A strong Dollar will become toxic to fake housing prices, to fake stock prices (eventually), to fake commodity bubbles. Of course, ZIRP and QE are free money given to the richest people in the world, the richest corporations in the world, to buy their own stock and force prices higher even when the underlying businesses are weakening — ZIRP is a massive cover-up for Wall Street to try to keep the floor from caving in, and to try to keep the public in ignorance of what is really happening; ZIRP and QE are a stealing of future earnings from American taxpayers in order to cushion the blow to our comfort today. ZIRP and QE make the richest people in the world even richer. ZIRP and QE keep the US Dollar weak, keep it from doing its job as the guardian of sane monetary policy. This is the key linchpin to this plan: the Dollar needs to remain weak so the Big Lie of Perpetual Growth can continue to trick and betray the world populace. So subverting this weak Dollar conspiracy will not be easy, or without major oppositions.

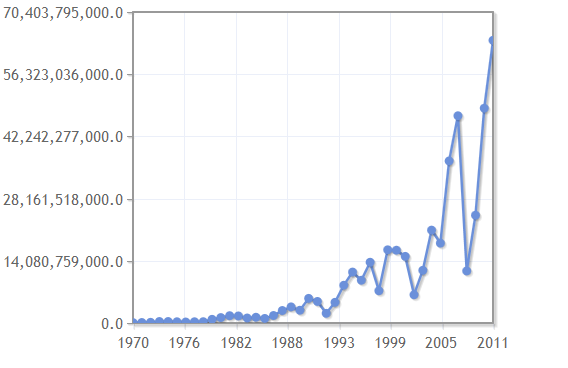

The chart below shows this QE lie.

Asian and other ’emerging’ economies, companies and individuals borrowed massive amounts of US Dollars during the QE pandemonium over the last decade. The chart below gives some picture of this:

(click to enlarge)

The next chart shows “hot money’ flows into Singapore during the weak Dollar ‘exporting of inflation: around the world’ stage triggered by Dollar weakness and later by premeditated weak-Dollar QE-centered FED policies.

How is this weak-Dollar money going to be replaced when the strong-Dollar loans need to be refinanced? Note: debts taken out in weak US Dollars become much more expensive to refinance with more strong-Dollar loans. This is what destroyed Latin America’s economy in 1980-83, the Asian and the Russian economies in 1998-2002, and what is happening today as the Dollar gets stronger.

William Pesek writes for Bloomberg that “Asia’s Next Crisis Is a Flood of Debt“,

The Mercentary Trader published recently an article “The Dollar is the Lawn Mower, the World is the Grass.” The article agrees with my premise that the strong Dollar is the world’s de facto deflation engine.

From that article:

To understand how big the dollar trade is, consider this: The USD is the other side of a carry trade measured in trillions of dollars. That is trillions with a “T.”

Some estimate the USD carry trade to run about three trillion. Others see it as high as five trillion. Regardless, it is absolutely gargantuan. And the rising dollar means a great unwinding is at hand.

In tandem with its role as the world’s reserve currency, the US dollar serves as a “funding currency.” That means that the dollar is used all over the world to facilitate loans and leveraged transactions. Many emerging market economies, for example, will take out loans denominated in dollars rather than their own currency. The widely accepted nature of dollars makes the debts more liquid and palatable to international investors. Commodities, of course, are also priced in dollars. All over the world, transactions are made in dollars where a liquid “go between” medium is needed for parties dealing in less liquid home currencies.

The United States is the wealthiest country in the history of the world. Its economy alone has long represented 25% of global GDP. In stock market terms, this makes the USA like an Apple, Microsoft or Google in a world of small caps. As such, when the United States sends dollars out into the rest of the world – engaging in foreign investment, buying and investing on credit – that provides liquidity to the rest of the world. This liquidity then “greases the wheels” of economic activity for the entire planet. No other single economy is large enough, dominant enough, or diverse enough to provide this essential role. The United States, via the dollar, and via the USA’s highly active investing and borrowing activities, is a sort of first and last resort liquidity provider for the global free market economy.

Most “dollar doomers” don’t understand the macro and never did. They always underestimated the inherent strength of the US balance sheet. They never realized that, compared to the assets, cash flows and intellectual property America holds on its books, along with its long list of superlative “superpower” advantages – military superpower, agrarian superpower, technology superpower, innovation superpower, real estate superpower, now energy superpower, on and on – America’s national debt is about as onerous as a mid-sized car payment for an upper middle class family.

So here is the thing. Because the US dollar is a funding currency for the world, a falling USD is, in general terms, a bullish phenomenon. When the dollar is falling, global credit conditions are loosening, not tightening. A falling dollar means more grease for the wheels – more oil and lubrication for the global economic machine. Emerging markets can borrow more. US-based investors are more incentivized to invest abroad, and provide the funding for dollar-denominated loans in overseas markets. US multinationals are more incentivized to seek overseas profits, which fatten their bottom lines when converted to weakening dollars. A falling dollar also acts as a tailwind for rising commodity prices, which boosts emerging market fortunes and encourages global mining and drilling and exploration activity.

A rising dollar, however, is the equivalent of a broad-blanket tightening of global credit conditions. It takes all the above effects and slams them into reverse.

A sharply rising dollar puts emerging markets in very grave danger, for example. It highlights the perils of borrowing in a currency other than one’s own. When the dollar rises, dollar-denominated debts suddenly become much more expensive in real payment terms, even as emerging market economies face economic slowdown and investor capital flight simultaneously. This is the equivalent of a highly leveraged business suddenly seeing the real cost of interest payments rise, even as sales slow dramatically and credit lines are being yanked – all at the same time.

And we have already seen what a brutal rise in the dollar does to commodity prices and commodity producers. It absolutely destroys them.

This week the Swiss National Bank short-circuited European fake recovery efforts. The Swiss, three years ago pegged, their currency to the Euro in an attempt to devalue the Swiss Dollar. But as the Euro sank, and then sank even more as the Dollar raced higher, the Swiss spent massive amounts of money buying Euros to defend their artificial peg to the Euro. Speculation about a coming EU QE spending binge — or perhaps intimate knowledge of its coming — forced the Swiss to end their peg to the Euro. Swiss officials feared EU QE would drown both the Euro and its artificially-attached Swiss Dollar, costing the Swiss even more to continue financing this insane fake recovery that gives away billions to the richest people in the world.

Swiss manufacturing has benefited from this currency meltdown, making Swiss products cheaper for other countries to import. But the cost on the other end (the continual purchasing of weakening Euros to defend the peg) was devastating; and the SNB’s balance sheet began to approach the level of Switzerland’s annual GDP. So the Swiss cut the cord, freeing the Swiss currency, and sinking the Swiss stock market — which the costly devaluation had helped to inflate. The Swiss also cut their interest rate, instituting negative interest rates, in an attempt to cushion the Swiss Dollar’s market gain after the announcement of the peg’s removal.

This did not work, at least not immediately. The Swiss Franc soared 30% against the Euro on Thursday, 25% against the US Dollar, costing hedge funds and investment banks and individual investors billions, causing at least two large currency brokerages to go out of business. Swiss stocks fell 10%. (Of course, if someone lost, someone gained.)

I bring this up because it also fits into the specter of a rising Dollar, and its deflationary impact. The Swiss jumped off the sinking boat. They are not going down with Europe. The Swiss are going to defend themselves: to hell with the EU and the Euro.

This is what the currency war looks and feels like. This is the stage to which economists refer as the ‘beggar thy neighbor‘ stage, protectionism…or the aforementioned “Currency Wars“, which the U.S started with its QE policies, but which is heating up even more now with the Swiss “Non” vote on further fake policies of inflation and more debt.

Economists tend to define this stage as the great mistake we made in the past deflations, which must be avoided this time around at all costs. But this is not a mistake; it is simply a necessary stage that countries must attempt to go through and survive in order to make it all the way around the Big Circle and get back to “GO” so they can start over again, without debt, collecting $200 to start the game over again.

Switzerland wants to join America as being the land of high bond prices (low yields) and strengthening currencies. Switzerland is voting to be with America, and not to be with Europe. This is NOT a vote of confidence for Mario Draghi and his central bank of followers. The Swiss vote was a vote against central bank illusions of perennial growth through cheap debt and currency devaluation. This is the beginning of the end for QE and for Keynes’ modern day usurpers.

How long before Germany decides they want to do what the Swiss just did? It is possible that the Germans will kick the Greeks out of the EU (and the Greeks will kick themselves out of the Euro) and then decide to leave the EU and Euro themselves. Would that be so surprising?

Keynes wrote in 1920:

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency.”

Has the Greenspan-Bernanke-Yellen team ever read this quote from Keynes? Has it been their intention to destroy the Capitalist system? Do they really grasp the possible repercussions of what they are doing?

Keynes continued:

“By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security, but at confidence in the equity of the existing distribution of wealth.”

This is a perfect description of what central bank policies since 2001 have done.

Keynes concludes:

“Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become “profiteers,” who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuates wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery.”

This is the essential writing of an economist who is aped by the very men and women who became the architects of the cheap debt, low interest rate policy that is now ravaging the entire world — and which could very well bring to power again in devastated European capitals the nationalistic right-wing movements that forced murder and destruction on the European continent not 80 years ago?

Deflation is at hand. The strong Dollar will break the theology of Inflation and will trigger the great destruction of debt that should have been begun in 2001, fourteen years earlier. Any thought that the Great Deflation can be avoided should be banished for ever from the minds of anyone calling him- or herself rational. An international policy to fight massive insolvency with more debt should be branded for ever an insanity, the production of a one-sided mind having neither balance nor sophistication nor common sense.

The central banks’ regressive policies are generating CHAOS in slow-motion. Perhaps this is their glory. That they are generating CHAOS in slow-motion. That ‘s what they have done in Japan. Still, Chaos is the result. We all remember what they say about good intentions.

For every Inflation there is an equal and opposite Deflation. For every Boom there is an equal and opposite Bust. Get ready for the real pain to begin. But, in this context, as in many contexts, pain is the beginning of learning a vital lesson about life. Don’t borrow what you can’t afford to pay back.