by Edward Harrison, Credit Writedowns

I was on the Daily Ticker with Lauren Lyster talking about Japan last week. My view is that there is no material negative change in Japan’s sovereign debt outlook nor will there be in the medium term because of Abenomics. The video is at the bottom of this post.

I was on the Daily Ticker with Lauren Lyster talking about Japan last week. My view is that there is no material negative change in Japan’s sovereign debt outlook nor will there be in the medium term because of Abenomics. The video is at the bottom of this post.

Before you watch it let me say a little bit about why I take this view on Japan and speak more generally about government debt and deficits. Mike Konczal wrote a post that is getting a lot of buzz on high government debts and Reinhart and Rogoff that will be a good jumping off point for discussion.

Here’s what Mike had to say:

In 2010, economists Carmen Reinhart and Kenneth Rogoff released a paper, “Growth in a Time of Debt.” Their –

“main result is that…median growth rates for countries with public debt over 90 percent of GDP are roughly one percent lower than otherwise; average (mean) growth rates are several percent lower.”

Countries with debt-to-GDP ratios above 90 percent have a slightly negative average growth rate, in fact.

This has been one of the most cited stats in the public debate during the Great Recession. Paul Ryan’s Path to Prosperity budget states their study –

“found conclusive empirical evidence that [debt] percent of the economy has a significant negative effect on economic growth.”

The Washington Post-editorial board takes it as an economic consensus view, stating that –

“debt-to-GDP could keep rising — and stick dangerously near the 90 percent mark that economists regard as a threat to sustainable economic growth.”

Is it conclusive? One response has been to argue that the causation is backwards, or that slower growth leads to higher debt-to-GDP ratios. Josh Bivens and John Irons made this case at the Economic Policy Institute. But this assumes that the data is correct. From the beginning there have been complaints that Reinhart and Rogoff weren’t releasing the data for their results (e.g. Dean Baker). I knew of several people trying to replicate the results who were bumping into walls left and right – it couldn’t be done.

In a new paper, “Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff,” Thomas Herndon, Michael Ash, and Robert Pollin of the University of Massachusetts, Amherst successfully replicate the results. After trying to replicate the Reinhart-Rogoff results and failing, they reached out to Reinhart and Rogoff and they were willing to share their data spreadhseet. This allowed Herndon et al. to see how how Reinhart and Rogoff’s data was constructed.

They find that three main issues stand out. First, Reinhart and Rogoff selectively exclude years of high debt and average growth. Second, they use a debatable method to weight the countries. Third, there also appears to be a coding error that excludes high-debt and average-growth countries. All three bias in favor of their result, and without them you don’t get their controversial result…

I haven’t had time to take a look at the paper so I don’t want to wade into the wonkish part of debate on Reinhart and Rogoff’s methodology but I do want to say a few words about this that relate to Japan and government deficits.

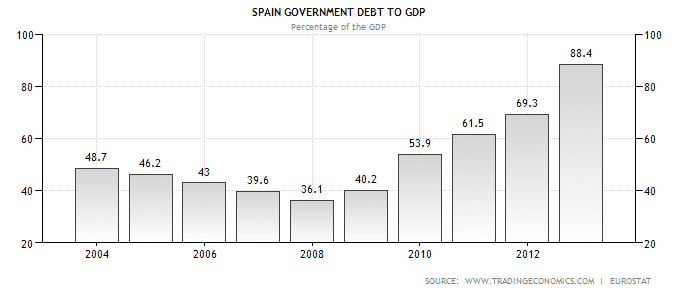

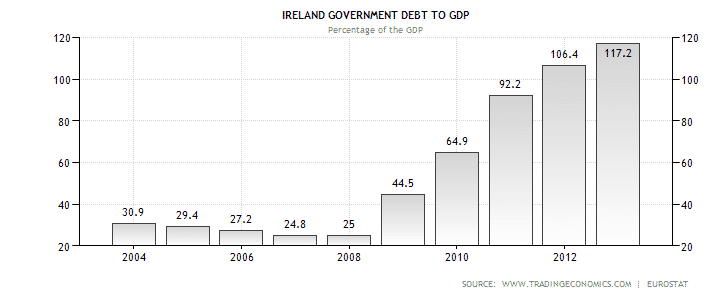

First, it has to be said right from the outset that the financial crisis – and everything that has led from it – is due to private sector debt problems in the first instance. It is private debt that caused the subprime crisis. It is private debt that sent Fannie, Freddie, Lehman and AIG down. It is private debt which almost vaporized the global credit system. And even today as we are embroiled in the Euro crisis, private debt plays the crucial role in countries like Spain and Ireland that had no deficit problems pre-crisis and low levels of public debt as well.

First, it has to be said right from the outset that the financial crisis – and everything that has led from it – is due to private sector debt problems in the first instance. It is private debt that caused the subprime crisis. It is private debt that sent Fannie, Freddie, Lehman and AIG down. It is private debt which almost vaporized the global credit system. And even today as we are embroiled in the Euro crisis, private debt plays the crucial role in countries like Spain and Ireland that had no deficit problems pre-crisis and low levels of public debt as well.

Click to enlarge

Click to enlarge

So that’s the first point here. This fixation on public debt at the expense of tackling private debt problems is completely misguided and actively contributes to the worsening of the crisis. Only in the euro zone where the fiscal space is severely limited – even in Germany – should the public debt situation be a prevailing policy worry.

Second, there’s the age-old problem with causation and correlation when you look at works like Reinhart and Rogoff’s. I think Tyler Cowen is right about one of the central problems in this debate when he wrote about his view of the crisis earlier today, saying that,

“the primary mechanism is slow growth causing high debt/gdp ratios, not vice versa. In any case this is by far the most important issue, whether or not you agree with my take on it.”

100% correct. If slow growth were to cause high government debt to GDP, you are going to have a different policy prescription than if it works the other way around.

So, right from the start here, you should realize that one should never have been able to use this Reinhart and Rogoff study as an excuse for immediate and front-loaded austerity. As Cowen says, “the case for austerity rests not on the Reihnart and Rogoff work but on the concept that dawdling on adjustment” is bad. Ultimately, I believe dawdling on adjustment leads to the Japanese scenario, in which the Japanese have by far the highest government debt to GDP in history of any industrialized nation accumulated in peace time and a serious case of deflation to boot. The Japanese have been in a policy cul-de-sac for years and their predicament is the direct outgrowth of misguided economic ideology that has alternated between austerity and stimulus as the deflationary crisis took hold. That’s the real story for policy makers

Let me reach into my archives for a few ways to frame this.

OK, here’s how I want to start this. Last February I wrote a post on government deficits as far as the eye can see. I recommend you read that post because the points I make there are critical to the background debate about public and private debt. My conclusion here was that there is no reason whatsoever for so-called structural deficits – i.e. government budget deficits in excess of nominal GDP growth over the course of the business cycle. But I come out of that post with three main points on deficits beyond this:

- Cyclical deficits are not important. An economy goes through business cycle peaks and troughs that cause deficits to rise and fall. Setting up an arbitrary line in the sand as the Europeans have done with the Maastricht 3% deficit hurdle only makes things worse because it creates pro-cyclicality and makes crisis more likely. Raising taxes or cutting spending before you reach full employment is likely to increase these cyclical deficits as we now see in Europe.

- The government budget constraint is fictitious. The whole deficit sustainability concept is an artificial construct for fiat currency issuers. The concept is usually based on a flawed view that taxes fund government expenditures when every dollar, euro, or pound in your pocket is an IOU created by government out of thin air aka fiat currency. Hello? That’s why everyone is mad at the Fed – because Ben Bernanke has been using this fact to try to stimulate the economy. You know the helicopter speech: “The government has a printing press to produce U.S. dollars at essentially no cost” and all that. You may not like it but that’s how it works, folks. Debt-to-GDP constraints like Reinhart and Rogoff’s are better at framing sustainability. But even these are artificial.

- The real fear with government deficits and debt is waste, corporatism and corruption. I actually wrote extensively about this after another interview with Lauren Lyster last year. We should just spell it out for people instead of making things up. That’s what this is all about. People are concerned that government is a poor allocator of capital and that allowing it to deficit spend on a large scale and add net financial assets to the private sector is going to lead to economic underperformance. Think about the bailouts for example: don’t they lead to some companies that couldn’t make the grade getting a second go at competing with companies that could? How is that good for growth? A bailout is a risk shift, a socialization of losses. It takes private losses of some economic agent in the private sector and shifts them onto the public balance sheet. This keeps that economic agent in business and keeps jobs in place. But I would argue it lowers long-term growth. That’s what is wrong with large-scale deficit spending (and easy money): it helps keep zombies alive either explicitly though direct bailouts or implicitly through reflationary policies that goose GDP or lower the cost of capital of marginal enterprises, shifting capital investment toward those marginal companies and projects.

This is the takeaway in Japan: stimulus without reform leads to a policy cul-de-sac. Monetary and fiscal stimulus is not a cure-all for economies or Japan would be the model and it most assuredly is not the model. If you want to use stimulus at all, then you need to have reform policies as well. It’s a three-pronged approach. The supply side matters. And that is the promise of Abenomics, isn’t it: fiscal and monetary stimulus as bridges to sustainable growth due to economic reform. Supposedly, this is what Abenomics is all about. And the Wall Street Journal told us yesterday that this reform, the third leg of this stool is now being put into place. Be sceptical, of course. Let’s just see what happens.

So, while I am sceptical, I am not bearish on Japan if that’s where this is headed. This is why stocks should be up in Japan and also why the currency is down. Of course, if Japan doesn’t follow through, all bets are off. But, at a minimum, the country can continue to keep policy rates at zero percent and ‘print money’ for the indefinite future as the UK did in reducing its mountainous debt load after World War 2. The key is growth. The UK did use currency depreciation and inflation to pare its sovereign debt. But they also had considerable growth too – attracting a flood of immigrants during the 1950s and 1960s. Japan’s demographics, on the other hand, are ugly. It has a shrinking population. And I don’t see waves of immigrants washing over Japan’s shores. How are you supposed to get nominal GDP growth above the deficit under that scenario?

Major industrialized countries with nonconvertible fiat currencies i.e not using the gold standard or in the euro zone should take the right lessons away from the Reinhart and Rogoff study and from Japan’s experience.

Take a cue from Japan. The lesson is not to stimulate and deficit spend like mad and hope this succeeds in reflating the economy. That’s just a risk shift onto the public balance sheet. And the Japanese experience shows that people are uncomfortable with these kinds of deficits and will always work to reduce them irrespective of the consequences. You need supply side fixes too.

Take a cue from the euro zone. The lesson is also certainly not to undergo painful – and front-loaded – austerity like the euro zone. The Europeans have tied their hands with the euro. There is no currency sovereignty there and the ECB is legally forbidden to be politically aligned with any national government. The threat of insolvency is real. But Britain doesn’t have to go down this path. If Britain were broke, then it’s been broke for most of the last 300 years. The UK has a lot more policy space. The bond vigilantes are a myth.

Ideologically-speaking, Kyle Bass and I have a lot in common. And he is a great fund manager to boot. I know he is looking for asymmetric bets of the subprime crisis variety. That makes a lot of sense if you are seeking alpha. So I have great respect for him. I simply disagree with him on the likelihood that this bet can pay off anytime in the near to medium-term. Where he sees insolvency, I see money printing and currency depreciation. Talk to me when there’s a global oil shock like there was in the 1970s, when inflation is a real and present danger. Until then, the widowmaker trade will continue to make widows.

Click on graphic to watch the interview.

Source: Why Japan Bears Are Wrong And Retail Investors Should Stay Away – Yahoo! Finance)

Also do read this on central banks and bond vigilantes. It is important: The Fed exerts a dominant influence across the yield curve, not just on the short end.

Editor’s note: Edward Harrison writes a premium financial newsletter. Sign up here for a free trial.