by Doug Short and Steven Hansen

The February 2014 Consumer Price Index (CPI-U) year-over-year inflation rate moderated fueled by a fall in energy commodity prices.

The Consumer Price Index (CPI-U) year-over-year inflation rate fell from 1.6% to 1.1% . Core inflation (CPI less food and energy) was unchanged to 1.6%. The market expected month-over-month CPI-U growth at 0.1% to 0.4% (consensus 0.1%) versus 0.1% actual, with the core inflation (less food and energy) expectations at 0.0% to 0.2% (consensus 0.1%) versus 0.1% actual.

Unadjusted CPI-U – Year-over-Year Change (blue line, left axis) and Month-over-Month Change (red line, right axis)

The Producer Price Index showed finished goods fell from 1.2% in January 2014 to 0.9% in February 2014. The CPI rate of inflation is generally higher the PPI.

As a generalization – inflation accelerates as the economy heats up, while inflation rate falling could be an indicator that the economy is cooling. However, inflation does not correlate well to the economy – and cannot be used as a economic indicator.

Energy by far was the major influence on this month’s CPI.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.1 percent in February on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 1.1 percent before seasonal adjustment.

An increase in the food index accounted for more than half of the all items increase in February. The food index rose 0.4 percent in February, driven by a 0.5 percent increase in the index for food at home, with four of the six major grocery store food group indexes increasing. The energy index declined, with a decrease in the gasoline index more than offsetting sharp increases in the fuel oil and natural gas indexes.

The index for all items less food and energy also rose 0.1 percent in February. An increase of 0.2 percent in the shelter index was the major contributor to the rise, but the indexes for medical care, airline fares, personal care, recreation, and new vehicles also increased. In contrast, the indexes for household furnishings and operations, apparel, used cars and trucks, and tobacco all declined in February.

The all items index increased 1.1 percent over the last 12 months; this compares to increases of 1.5 percent in December and 1.6 percent in January. The index for all items less food and energy rose 1.6 percent over the last 12 months. The energy index declined 2.5 percent over the same period, while the food index has increased 1.4 percent.

Historically, the CPI-U general index tends to correlate over time with the CPI-U’s food index. The current situation is putting an upward pressure on the CPI countering the downward pressure on the CPI by the Producer Price Index.

CPI-U Index compared to the Food sub-Index of CPI-U

Notice the gap in the above graphic between the CPI and Food – historically this gap has always closed when the knock-on effect from higher food prices into other CPI components moderates.

The Federal Reserve has argued that energy inflation automatically slows the economy without having to intervene with its monetary policy tools. This is the primary reason the Fed wants to exclude energy from analysis of consumer price increases (the inflation rate).

In the above chart – the green boxes are elements moderating inflation, while the red boxed items are fueling inflation.

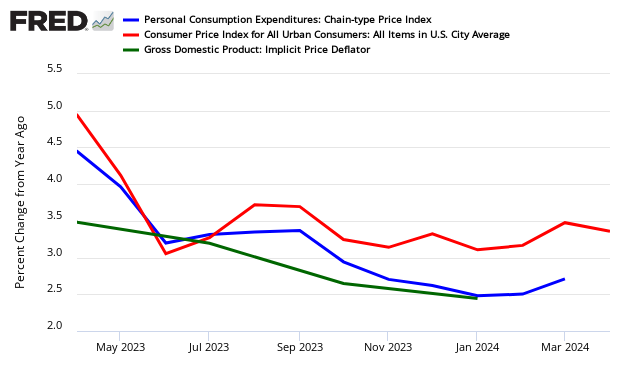

The graph below looks at the different price changes seen by the BEA in this PCE release versus the BEA’s GDP and BLS’ Consumer Price Index (CPI).

Year-over-Year Change – PCE’s Price Index (blue line) versus CPI-U (red line) versus GDP Deflator (green line)

Detailed Analysis

The first chart is an overlay of Headline CPI and Core CPI (the latter excludes Food and Energy) since 1957. The second chart gives a close-up of the two since 2000.

On the chart below I’ve highlighted 2 to 2.5 percent range. Two percent has generally been understood to be the Fed’s target for core inflation. However, the December 12 FOMC meeting raised the inflation ceiling to 2.5% for the next year or two while their accommodative measures (low Fed Funds Rate and quantitative easing) are in place.

Federal Reserve policy, which has historically focused on core inflation, and especially the core Personal Consumption Expenditures (PCE), will see that the latest core CPI is below the near-term target range of 2 to 2.5 percent, and the more volatile headline inflation, further below the target range.

Caveats on the Use of the Consumer Price Index

Econintersect has performed several tests on this series and finds it fairly representative of price changes (inflation). However, the headline rate is an average – and will not correspond to the price changes seen by any specific person or on a particular subject.

Although the CPI represents the costs of some mythical person. Each of us need to provide a multiplier to the BLS numbers to make this index representative of our individual situation. This mythical person envisioned spending pattern would be approximately:

The average Joe Sixpack budgets to spend his entire paycheck or retirement income – so even small changes have a large impact to a budget.

The graph above demonstrates that fuel costs, medical care, and school costs are increasing at a much faster pace than the headline CPI-U.

The Bureau of Labor Statistics (BLS) has compiled CPI data since 1913, and numbers are conveniently available from the FRED repository (here). Long-term inflation charts reach back to 1872 by adding Warren and Pearson’s price index for the earlier years. The spliced series is available at Yale Professor (and Nobel laureate) Robert Shiller’s website. This look further back into the past dramatically illustrates the extreme oscillation between inflation and deflation during the first 70 years of our timeline. Click here for additional perspectives on inflation and the shrinking value of the dollar.

The chart below (click here for a larger version) includes an alternate look at inflation *without* the calculation modifications the 1980s and 1990s (Data from www.shadowstats.com).

Because of the nuances in determining the month-over-month index values, the year-over-year or annual change in the Consumer Price Index is preferred for comparisons.

Econintersect has analyzed both food and energy showing that food moves synchronously with core.