by Keith Jurow, Capital Preservation Real Estate Report

There is widespread consensus that the real estate crisis is over. The possibility of a repeat of the collapse of 2008-2009 is inconceivable to investment advisors and their wealthy clients.

Wealthy investors have been flocking back to real estate with abandon. TIGER 21 – an organization for ultra-high-net worth investors (UHNW) – publishes the results of its asset-allocation survey of its members every quarter. The latest survey for the third quarter illustrates this point very well. Take a good look.

Of the members surveyed for the 12 months ending in the third quarter, the average portfolio allocation to real estate was 25%. That is six percentage points higher than the average reported in the first quarter of last year. It is also as high as the allocation was in 2007, at the height of the real estate bubble.

This percentage allocation to real estate is the highest of any asset class including public equities. Wealthy investors are now as comfortable with the prospects for real estate investments as they were in 2007.

The unseen dangers of complacency

Because of this complacency, wealth management firms and RIAs widely believe that you do not need to talk about risks at all.

Wealthy investors no longer think it is necessary to be vigilant about possible risks to their portfolio. Market risks that would be heeded during less optimistic times are brushed aside or overlooked. Tail risks — like those that surfaced in 2008 — are simply dismissed. Credit risks of default are minimized and often ignored.

The most dangerous problem is that assumptions are taken as facts. What do I mean? The assumption that we are in economic recovery is not questioned by the pundits and Wall Street analysts.

We all know there is a recovery, right? It’s a certainty … so no need to discuss the matter. A classic example of this was the Barron’s article in April 2013 on “What’s the Best Path to Real Estate Profits.” The author began by proclaiming that “The housing crisis that wiped out trillions of dollars of personal wealth and shook investor confidence is finally over.”

Not a word was said about residual risks that remain after the largest real estate collapse in American history. The author’s unstated assumption was that we all know the crisis has ended and that recovery is well underway. If that’s a fact, why would there be any need to discuss possible risks still lurking out there in housing markets?

Herd mentality is insidious. Those analysts and pundits who share this thinking find it exceedingly difficult to see that what they accept as fact is merely an assumption.

Advisors must consider the possibility that what is assumed may not be true. This means challenging common perceptions. While not an easy task, it is absolutely essential for any investment advisor whose clients have large asset portfolios at risk.

High-net worth investors own a lot of real estate

In January 2014, Morgan Stanley released the results of its Wealth Management Investor Pulse Poll. More than 300 investors with over $1 million of investible assets were asked about their holdings of various alternative investments.

By far, the most widely held was real estate, owned by more than 77% of those interviewed. This did not include REITs which was the second most widely owned alternative investment. One third of those millionaires who owned real estate were planning to buy more.

At the end of 2013, giant real estate consulting firm KnightFrank polled more than six hundred private bankers and wealth advisors. They were attempting to learn about the attitudes and portfolios of their UHNW clients.

The results represented the answers of more than 23,000 UHNW investors around the world. For wealthy investors in North America, an average of 20% of their portfolios was allocated to real property. As for 2014, those intending to increase their exposure to real estate outnumbered those intending to shrink it roughly seven to one.

Optimism is at near record levels for private investors according to Marcus & Millichap’s Third Quarter 2014 Commercial Real Estate Investment Outlook. Nearly 50% of those surveyed expect to increase their real estate investments in the next 12 months. Only 5% expect to reduce their position.

This optimism about real estate extends to institutional investors as well. Data provider Preqin’s Investor Outlook for Alternative Assets for the first half of 2014 surveyed more than 400 institutional investors at the end of last year. It found that nearly one-third intended to increase their allocation to private real estate funds. Only 5% planned to decrease their allocation. Nearly half of those surveyed had a positive perception of real estate. Only one out of ten had a negative view.

Wealthy investors are pouring money into commercial real estate

Convinced that real estate recovery is firmly in place, wealthy investors threw money into commercial real estate last year at a pace not seen since the heady days of 2007. According to Real Capital Analytics, private investors purchased more than $244 billion of commercial real estate in 2013.

Why are they jumping back into this market so aggressively? Have they entirely forgotten the debacle of 2008-2009? This is only part of the reason. A survey of high net worth investors taken in February by the Investment Program Association (IPA) found that roughly 83% believe that commercial real estate will post a better performance than the stock market over the next five years.

An article posted on WealthManagement.com at the end of March explored in detail the attraction that commercial real estate now offers to high net worth investors. It featured an interview with Dani Evanson, a managing director at RMA, a real estate investment and advisory company for family offices and wealthy management firms.

Evanson explained that two years ago, she began to get heavy inquiries from new clients looking to “bet” on commercial real estate as well as existing clients looking to increase their holdings significantly. Since then, she said, “the vast majority of our clients have increased their allocations to commercial real estate.”

The entire portfolio of one of her new clients had previously been invested in stocks and bonds. However, because of a negative return in the client’s bond portfolio, the client elected to allocate 5% of the portfolio to “an illiquid real estate portfolio” to obtain a better yield. Evanson believed that this move showed a major change in thinking.

As she viewed wealthy investors, they fell into two distinct camps. One group sought cash-flowing properties that were relatively low-risk. The others were risk-takers – willing to invest in value-added or opportunistic properties with the chance for a much higher return. She believed that wealthy investors wanted either one or the other.

Are we witnessing a 2007 redux?

In numerous articles published over the last several years, I have pointed out that even savvy investors have short memories. As the real estate collapse unfolded in 2007-2008, there was growing fear, angst, panic and terrible decision-making by investors both rich and not-so-rich. Countless investors swore they would never invest in real estate again.

REITs and real estate ETFs – which had soared for several years – utterly collapsed. I have shown the extent of the carnage in several previous articles (see here, for example).

Keep this in mind. The collapse turned around in 2009 only because the bank regulators panicked and decided to let the banks play accounting games. Properties no longer had to be marked-to-market. The banks were rewarded with the role of final arbiter of when a property was non-performing and could no longer accrue interest. So the financial statements that they issued became utterly worthless and their 10-Q quarterly reports to the FDIC little more than a joke.

It was under these make-believe conditions that investors were lured back into the real estate markets. What was originally a trickle in 2010 has become a torrent of both institutional and private investor money.

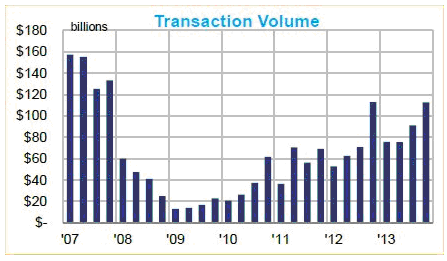

In 2007, an incredible $560 billion in commercial real estate sales were transacted according to Real Capital Analytics. Two years later, that figure had plunged to roughly $70 billion. For a couple of months in the spring of 2009, markets essentially shut down and bids could not be obtained even for good properties.

Source: Real Capital Analytics

Back in 2009, it was inconceivable to me that commercial real estate sales would be on track to hit $400 billion only five years later. I am still quite amazed.

Does this mean that the markets are once again healthy? Were they healthy in 2007? The answer to both questions is a resounding” no.” In 2007, speculative madness gripped investors to an extent which had never before been seen.

The frenzied buying in Manhattan today reminds me of 2007. Purchasers are oblivious to price or to any of the fundamentals. Foolish buyers are out in force in the Big Apple.

However, the situation today is very different from those bubble years. The markets in 2005-2007 were not recovering from a terrible collapse. Real estate markets had been good for nearly 15 years since the awful shakeout from the savings and loan disaster.

Investors who witnessed the unbelievable crash that followed the pricking of the bubble have come to dismiss it as a bad shakeout from excessive speculation. Many analysts and Wall Street economists now refer to it as merely part of the long-term real estate cycle. The only difference is that this last cycle had both higher highs and lower lows.

Can advisors minimize the threat of tail risks to clients?

High-net-worth investors were caught unprepared as the real estate collapse unfolded. Most investment advisors continued to maintain a bullish stance after the stock market peaked in 2007 and commercial real estate markets began to tank.

An example of the shock and dismay felt by wealthy investors was vividly described in an article published by the New York Times in October 2008. One investment advisor to the wealthy explained, “For the [family] office executives, it’s been an exhausting time in terms of hand-holding.” He went on to lament that “The family members are pointing fingers; they can’t believe how it sneaked up on them.”

That does not sound as if any planning for downside risks had been undertaken to protect wealthy investors against a possible tail risk. Without that in place, they were blindsided when markets deteriorated and were unprepared to take decisive action.

The managing partner of consulting firm Family Office Metrics declared in an article published in the summer of 2012, “family offices only deal with risk factors when a crisis presents.” He went on to point out the specifics of the problem:

“They have no practical approach to identifying or addressing deficiencies in their risk management and most do not measure their risk controls through analysis of probabilities and the impact of functional risk.”

In plain English, they have nothing in place to measure the degree of risk in their portfolios or the likelihood that something bad will occur.

In that same article, another head of a family office described the kind of help offered to wealthy investors:

“I heard of one family who paid over $500,000 for a very complex investment strategy based on sophisticated risk analysis by a specialist risk advisor and threw it in the bin within a year as it was useless in practice.”

What are we to make of this? If wealthy Americans are offered expensive risk management tools that are “useless in practice,” how can they prepare for investment risks of which they are unaware?

Another look at risk

In an article filled with wisdom and posted on Advisor Perspectives in early September, Howard Marks of Oaktree Capital explored in depth what risk is really all about.

Taking a swipe at the risk management experts who focus on the probability of loss, Marks stated unequivocally that we can no more measure the probability of loss than we can measure the probability of rain. The future is uncertain and no amount of quantification will enable us to predict what will happen.

Marks also bemoaned the widespread trust in statistical models of risk. Turning over investment decisions to those he calls the “quants,” he wrote, has caused investors to take risks which they would probably not have taken with their “qualitative judgment.”

What would Marks have the investor do? His answer: Use “experience, judgment and your knowledge of the underlying investment.” Also, accept uncertainty and be aware of what you don’t know. A lack of hubris will keep you aware of the risks out there.

Marks warned the reader that, at the time of his writing, the fear of missing out on opportunities exceeds the fear of losing money for most investors. That is the euphoria that I have been discussing. Because we have had several years of what he calls “a benign environment,” what might have been considered a risky investment now passes for “safe.” Once the risks become obvious, it is usually too late to prevent loss.

His advice for these times was simple: Pay more attention to what he called “loss prevention” and focus less on the “pursuit of gain.” I strongly urge you to read or even re-reread his article before the tide goes out and we see who is swimming naked.

Suggestions for Advisors

For four years, I have been consistently arguing that this real estate recovery is an illusion. The evidence I have uncovered and presented is still compelling. With complacency so widespread, I urge you to consider what I have been saying. Your clients trust you to alert them to risks confronting their portfolios. Minefields in front of them deserve your utmost attention.

Keith Jurow is a real estate analyst and former author of Minyanville’s Housing Market Report. His new report – Capital Preservation Real Estate Report – launched a little more than a year ago.