by Congressional Budget Office

The federal program that provides insurance against the risk of terrorism expired at the end of 2014. Without such a program, taxpayers will face less financial risk, but some businesses will lose or drop their terrorism coverage and economic activity might slow if a large terrorist attack occurs. Last year, the Congress considered legislation to reauthorize the program but shift more risk to the private sector. Other options include limiting federal coverage to attacks using nonconventional weapons, and charging risk-based prices for federal coverage. CBO has examined the likely effects of different approaches on the private sector and on the federal government.

The September 11, 2001, terrorist attacks resulted in nearly 3,000 deaths and roughly $44 billion of insured losses (in 2014 dollars). In light of the unexpected and unprecedented losses from the attacks, as well as the heightened uncertainty surrounding future losses, private insurers subsequently reduced the availability of terrorism coverage for businesses and commercial properties sharply. Policymakers were concerned that without terrorism insurance, commercial developers in high-risk areas would not be able to finance their projects, which would reduce new construction and job creation and thereby slow economic growth.

In response, lawmakers enacted the Terrorism Risk Insurance Act (TRIA) in 2002 as a temporary measure to provide catastrophic federal reinsurance for terrorism risks without charging premiums up front. Although no major terrorist attacks have occurred in the United States since 9/11, and thus the government has paid no claims, the threat of terrorist attacks persists, and lawmakers reauthorized TRIA in 2005 and in 2007. The program ensured that primary insurers continued to offer terrorism coverage on business and commercial policies (including workers’ compensation insurance), and it might have reduced the need for federal disaster assistance if an attack had occurred. But, as structured, the program exposed the government to a significant amount of financial risk and subsidized policyholders (many of which were large businesses).

How Did the Federal Terrorism Risk Insurance Program Work?

TRIA required all property and casualty insurers to offer terrorism coverage to their commercial policyholders. (Property and casualty insurance covers businesses against losses from property damage, workers’ compensation claims, business interruption, and most liability claims.) The federal government provided reinsurance to private insurers by agreeing to reimburse them for a portion of their terrorism-related losses of up to $100 billion on commercial policies after an attack. Losses above that amount would be uninsured.

Under TRIA, all types of losses from events certified as major terrorist attacks by the Secretary of the Treasury were covered unless such losses were excluded by the underlying property and casualty policies. Nuclear, biological, chemical, and radiological (NBCR) risks are typically excluded from property and casualty policies because they are difficult to estimate and potentially much larger than conventional risks (such as large truck bombs). The important exception to that exclusion is workers’ compensation policies: Almost all states require employers to purchase coverage for workers’ compensation and require insurers to cover losses from all causes, including NBCR attacks. Many policies also exclude cyber risks, such as those associated with deliberate interruptions of computer systems, payment systems, and power grids.

TRIA lessened the risk of losses to primary insurers by shifting responsibility for some insured losses to all commercial property and casualty policyholders and, in some cases, to the federal government. Insurers paid no premiums for TRIA coverage but bore some of the risk of losses through an initial deductible and then through a copayment above the deductible (the government would have paid the remainder). For the first $27.5 billion in insured losses (known as the aggregate retention amount), the government would have been required to recoup its outlays after an attack by imposing a tax on commercial property and casualty policyholders, including those without terrorism insurance.

CBO estimated the effects of TRIA on the federal budget on an expected-value basis, taking into account the estimated probabilities of losses of all sizes, including the substantial likelihood that losses in any year would be zero. In 2007, when TRIA was last reauthorized, CBO estimated that total federal spending resulting from the seven-year extension would be about $7.7 billion and that the net budgetary cost after accounting for recoupment would be about $1 billion—small relative to the total exposure of losses. The net costs were projected to be positive because CBO estimated that attacks causing losses greater than the aggregate retention amount were possible—although they would be very rare—and did not expect that the Treasury would exercise its discretion to recoup federal outlays for additional losses above that amount.

What Were TRIA’s Effects?

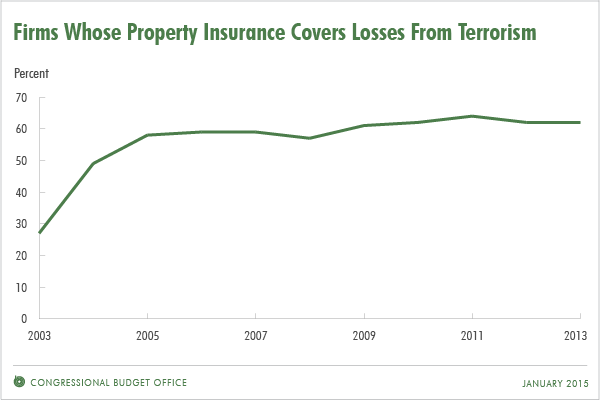

Until it expired, TRIA was one factor that enhanced the availability of terrorism insurance. Prices for terrorism coverage fell steadily during the years TRIA was in force, partly because of the program itself but also because of changing perceptions of terrorism risks and a growing supply of insurance in general. With the lower prices and TRIA’s requirement that insurers offer terrorism coverage, about 60 percent of large commercial businesses and owners of large properties purchased such coverage in 2013, compared with less than 30 percent in 2003 (see figure below). Terrorism coverage for workers’ compensation insurance, which almost all employers buy, accounted for about 40 percent of total premiums for terrorism insurance in 2013.

The broader economic effects of TRIA are unclear. By facilitating insurance for new construction and business operations in general, TRIA may have helped speed the recovery in the New York City area after the attacks on September 11 and may have benefited the national economy as well. However, any benefits to the national economy were probably small in recent years, in part because at least some of the development that occurred in higher-risk areas under TRIA would have occurred in lower-risk areas in TRIA’s absence, and in part because many private insurers probably would have included terrorism coverage—albeit at reduced policy limits and higher rates—in their policies even without TRIA’s coverage. (Insurers that chose not to offer terrorism coverage without TRIA’s coverage might have lost valuable long-term relationships and other business with policyholders who wanted terrorism coverage.) The program might have yielded more significant benefits to the economy if another large-scale attack had occurred, because insurers and others might, in TRIA’s absence, have reacted very strongly to the new evidence of risk and reduced their economic activity.

The TRIA program also had some economic drawbacks. Its reliance on recoupments after an attack reduced the premiums charged for terrorism insurance, especially for policyholders with high-risk properties. The spreading of risk among all commercial property and casualty policyholders that occurred through the rules for recoupments dampened incentives for insured businesses to mitigate risks—for example, by relocating activities to areas of lower perceived risk or by spending more on safety features—because the expected reduction in losses would not be fully reflected in the premiums those businesses paid. However, great uncertainty about terrorism risk makes the benefits of mitigation intrinsically hard for businesses to assess, and there is little evidence about how the change in incentives caused by TRIA affected mitigation efforts. The government’s role in terrorism insurance under TRIA also reduced the opportunity for private reinsurers and participants in capital markets to insure against terrorism risks and left taxpayers bearing most of the catastrophic risk. Although reinsurers’ ability and willingness to price and bear terrorism risk have increased, they cannot compete effectively against federal coverage that is available to insurers at no cost.

What Are the Expected Effects of TRIA’s Expiration?

The short-term effects of TRIA’s expiration on December 31, 2014, are expected to be modest: Insurers currently have adequate capital (defined as assets minus liabilities) to meet regulatory requirements and standards set by credit-rating agencies; more important, both insurers and reinsurers have shown in recent years an ability and a willingness to raise additional capital when presented with profitable opportunities to cover more terrorism risk. For most insurers, current potential exposures to losses from a terrorist attack are between 8 percent and 12 percent of their capital; they generally try to keep that exposure to less than 20 percent. Because the subsidies that accompanied the federal program have been lost, policyholders will face higher premiums. However, most effects on policyholders will not be felt until their policies come up for renewal, which will occur throughout 2015.

Looking forward, if new legislation providing terrorism risk insurance does not replace TRIA, most insurers will probably still offer terrorism coverage for conventional risks—even though there would be no federal mandate to do so—lest they lose business on other property and casualty lines. Even under TRIA, insurers faced considerable risk exposure through that program’s deductibles and copayments; facing greater risks, insurers will probably make more use of private reinsurance and perhaps capital-market approaches to reducing risk (such as securities that pay off if a specified insurance loss occurs) as well.

However, the supply of private reinsurance and risk-bearing capital will probably not expand enough to fully offset the loss of federal reinsurance, in part because of the challenges in pricing the risk that was previously borne by the government. As a result, policyholders will probably have fewer insurers to choose from and will face higher premiums and lower coverage limits. Some businesses will lose or drop their coverage. The effects on policyholders will probably be felt more acutely in high-risk areas, and economic activity (particularly construction) in such areas may be reduced. The decrease in risk sharing resulting from reduced insurance coverage might be less efficient economically.

The resulting higher insurance premiums and increased involvement of private reinsurers and capital markets are expected to have a number of effects on the distribution of risk and on the behavior of insurers and businesses:

- Risks to taxpayers will fall. But taxpayers will retain some risk because, in the event of a future terrorist attack, there would be tax deductions for uninsured losses and there would probably be demand for postattack assistance resulting from uninsured losses, as occurred after 9/11.

- Risks to private insurers and businesses will increase.

- Private insurers will probably try to take more account of policyholders’ risk levels in setting their premiums and in offering discounts for mitigation measures. However, the large uncertainties associated with terrorism risk will limit insurers’ ability to charge risk-based prices.

- Some policyholders who would pay lower premiums or receive higher discounts if they took actions to mitigate their risk will do so. Consequently, the expected losses from terrorist attacks probably will be smaller, although the magnitude of that effect might be quite small.

- Businesses that drop their policies (or are dropped by their insurers) and self-insure instead will also have incentives to mitigate their risk. Conceivably, bearing responsibility for their risks instead of sharing them through insurance might lead businesses to mitigate excessively from a societal perspective. Alternatively, some self-insured property owners might do less mitigation than they would if they went through the insurance underwriting process and learned more about their risks and ways to reduce them.

- If a terrorist attack causes large losses, insurance will probably be less available afterward than it would have been under TRIA. (The inherently speculative nature of predicting future terrorist attacks will limit the amount of private capital that would be put at risk.) Consequently, new commercial construction and credit flows might be impaired, which in turn could weaken the economy.

- Private insurers will probably provide less workers’ compensation coverage because private reinsurers will probably continue to be unwilling to offer coverage for NBCR attacks (which cannot be excluded from workers’ compensation policies) and because state regulations—such as those limiting risk-based pricing and diversification of risks—will hinder other market adjustments. Instead, more employers will probably be covered in the involuntary (or “residual”) market.

If lawmakers choose not to reenact TRIA or create a new reinsurance program, they could enact alternative policies to help businesses manage terrorism risk. For example, lawmakers could revise the corporate tax code to allow insurers to set aside tax-free reserves to cover expected claims from terrorist attacks, which could increase the availability of terrorism insurance. However, doing so would reduce federal tax receipts, particularly if regulatory oversight was insufficient to limit insurers’ use of tax-free reserves to the purpose that lawmakers intended.

The expiration of TRIA will not lead to any change in CBO’s budget projections. The projections made since TRIA’s last reauthorization in 2007 reflected the fact that the authorization extended only through 2014. Consequently, the lapse of the program’s authorization has no additional effect on the budget under current law.

What Would the Effects Have Been of S. 2244?

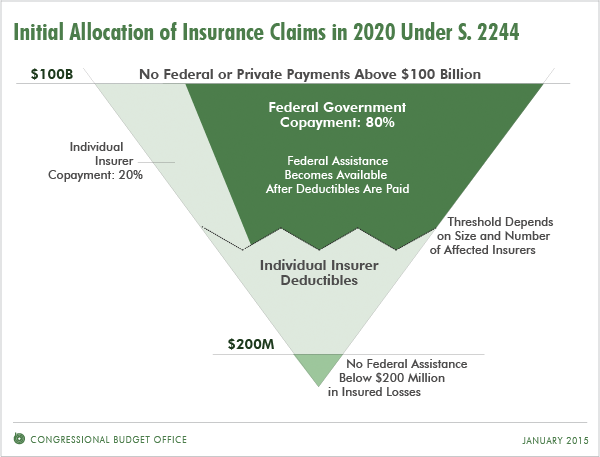

Before the 113th Congress adjourned, House and Senate negotiators reached a compromise that would have extended TRIA for six years. Under the version of S. 2244 (the Terrorism Risk Insurance Program Reauthorization Act) passed by the House of Representatives on December 10, 2014, insurers’ deductibles would have remained at 20 percent of premiums they received for coverage in the previous calendar year. Several other changes would have been phased in over the six years of the reauthorization (see figure below):

- The amount of losses triggering payments under the program would have increased by $20 million per year from a base of $100 million in the first year to $200 million in the sixth year;

- Insurers’ copayments for losses above those deductibles would have increased by 1 percentage point per year from a base of 15 percent in the first year to 20 percent in the sixth year; and

- The industry’s aggregate retention amount would have increased by $2 billion per year from a base of $29.5 billion in the first year to $37.5 billion in the fifth year; in the final year of the authorization, the retention amount would have risen to an amount equal to the average of insurers’ deductibles over the previous three years (about $50 billion, CBO estimated).

S. 2244 would have retained the mechanism for recouping some or all federal outlays through a surcharge (or tax) assessed on all commercial property and casualty policyholders. The tax rate would have increased from 133 percent to 140 percent of the difference between total losses (up to the annual industry retention amount) and the total amount paid by the insurance industry through its deductibles and copayments.

Effects on Insurance Markets and the Economy

Because S. 2244 would have retained the basic structure of the previous TRIA program, its effects would have been broadly similar. Terrorism insurance would have continued to be widely available, insurance markets would probably have faced less disruption after a terrorist attack than they would have otherwise, and the economy might have stabilized more quickly after such an attack. Insurers and their policyholders would have borne most of the risk of losses from terrorist attacks through their deductibles, copayments, and recoupments, unless those attacks had resulted in losses significantly larger than those on 9/11. By relying on the recoupment mechanism, the government would have avoided having to set premiums for its coverage. However, that approach would have distorted insurance markets by recouping costs from all commercial policyholders, many of whom have limited exposure to terrorism risk.

S. 2244 differed from TRIA in two key respects. First, increases in the copayments would have shifted more liability to the industry for initial payments on losses. That shift would have given insurers somewhat greater incentive to charge premiums that reflected policyholders’ individual risks, thus giving policyholders somewhat more incentive to adopt mitigation strategies, such as adding safety features to buildings. Consequently, losses from future attacks and spending on federal aid after an attack probably would have been slightly smaller than under TRIA. The higher copayment rate would also have allowed a somewhat larger role for private insurers.

Second, the higher aggregate retention amount would have increased the federal outlays to be recouped after a terrorist attack that caused more than $27.5 billion in insured losses; indeed, raising the retention amount over time to $50 billion would have led the government to recover all of its outlays in almost all cases, at least in principle. However, the taxes required to achieve the recoupment targets after a big attack could have been significantly higher than under previous law. The recoupment mechanism has yet to be tested, and after a very large attack, policymakers might be hesitant to tax all commercial policyholders, including those without terrorism insurance, especially if the economy was weak.

Budgetary Effects

In line with estimates made by some commercial catastrophe modelers, CBO’s estimates of expected losses from terrorist attacks have fallen since 2007. CBO currently estimates that expected losses from potential attacks that would be covered under TRIA if it was extended would be about $2.1 billion in 2015 and would rise each year with projected growth in the economy. Those expected amounts incorporate a wide and unevenly distributed set of possibilities, ranging from no attacks in a year to highly unlikely catastrophic attacks.

In 2014, CBO estimated that the six-year extension of TRIA under S. 2244 would have increased federal spending by $3.0 billion over 10 years and increased net revenues by $3.5 billion over that same period. (Estimated assessments exceeded projected claims over 10 years in part because claims can take several years to settle.) On net, CBO estimated, S. 2244 would have reduced the deficit by $450 million between 2015 and 2024. However, the 10-year estimates provide an incomplete picture. An additional $330 million would have been spent after 2024, CBO estimated, producing a total reduction in the deficit of about $120 million (leaving aside any potential effect on spending for disaster relief).

Changes in either the recoupment scaling factor or the pace of recoupment would have affected CBO’s estimates. If policymakers had set recoupment at 100 percent of the government’s outlays under the industry’s aggregate retention amount while keeping the bill’s requirement that all outlays be recouped by 2024, revenues would have been lower and the program would have had an estimated net budgetary cost of about $900 million. If, instead, policymakers had set recoupment at 140 percent, as in the bill, but allowed losses to be recouped over the 10 years following an attack rather than by 2024, the estimated net cost over the 10-year budget period would have been about $1 billion higher (because less of the expected recoupment would be received within the next 10 years). The projected net budgetary cost over all years would have been roughly the same.

What Other Policies Would Change the Distribution of the Financial Risks of a Terrorist Attack?

Some other approaches could leave the expected net budgetary cost of insurance for terrorism risk roughly the same as it would be under an extension of TRIA but would change how risks are shared between insurers, commercial policyholders, and the government. One such option would replace TRIA with a similar program that covered only NBCR attacks. Another option would charge risk-based prices for federal reinsurance, an approach that could be implemented in different ways. CBO evaluated those two options—as well as current law (the expiration of the program) and the option of extending and modifying TRIA as in S. 2244—on the basis of their effects on the availability of private insurance; on the amount of risk borne by the government (apart from any postattack assistance); on the demands for postattack assistance; on mitigation incentives; and on the economy.

Limiting a federal program to NBCR coverage would have various benefits and drawbacks compared with both the expiration of TRIA and a broad extension of TRIA. Without a federal program, private insurers are unlikely to provide much coverage for NBCR risks. By some estimates, a nuclear attack could result in losses of thousands of lives and hundreds of billions of dollars, particularly through workers’ compensation insurance. Losses of that size would pose solvency risks for insurers, and private reinsurance coverage for NBCR risks is largely unavailable because there is little basis for estimating the risks with confidence. Thus, limiting the federal program to NBCR coverage would have less effect on the availability of insurance in workers’ compensation markets than would terminating the program. It also would expose the government to greater risk than terminating the program but significantly less risk than extending the program broadly. By limiting the program to NBCR coverage, demands for assistance after an attack would be less than if no program existed but somewhat higher than under TRIA. Policyholders would have a greater incentive to mitigate conventional terrorist risks, but insurance markets would be more prone to disruption after a conventional attack than under TRIA and the economy would be likely to recover more slowly.

Charging prices for federal coverage that reflected the insured risks would encourage a bigger role for private reinsurers and would increase policyholders’ financial incentives to mitigate risks by reducing or eliminating the subsidies they received. That option would lower the risk to the government by diminishing its reliance on recoupments, which could be reduced, eliminated, or delayed. Implementing the option—that is, setting prices that accurately reflect the value of federal coverage—would be challenging, though various market-based approaches could be helpful. For example, the government could obtain an indication of the market value of its coverage by buying private reinsurance to backstop a portion of that coverage, as is done by Australia’s terrorism risk insurance program. (In contrast, the United Kingdom’s program charges insurers a percentage of their premium collections in exchange for the government’s financial backstop, requiring the government to determine the appropriate percentage. The percentage in the United Kingdom’s program was recently raised from 10 percent to 50 percent.)