by James Preciado and Jeff Baron , U.S. EIA

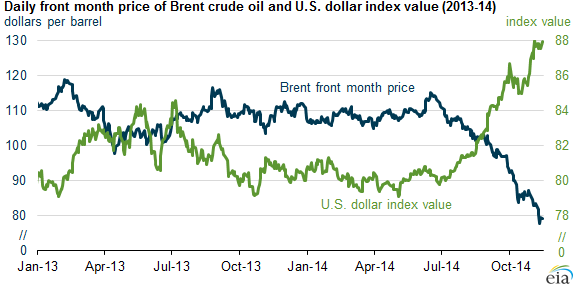

Since August, both crude oil and currency markets have been influenced by lower economic growth expectations in countries outside the United States. Prices in both markets recently broke out of established trading ranges, driven by concerns about weaker future global demand. The current situation, with the dollar index and oil prices moving in opposite directions, presents a sharp contrast to one in which crude oil supply disruptions or geopolitical risks would cause both the dollar index and crude prices to rise.

Source: U.S. Energy Information Administration, based on Bloomberg

Source: U.S. Energy Information Administration, based on Bloomberg

Note: The U.S. dollar index measures the value of the U.S. dollar against a basket of six currencies’ exchange rates: the euro, Japanese yen, British pound, Canadian dollar, Swiss franc, and Swedish krona. An increase in the index means the dollar is appreciating against these currencies. March 1973=100. Front month = the near-month contract for Brent crude oil energy futures prices.

Although the U.S. economy showed robust growth in the third quarter of 2014, recording an estimated 3.5% growth rate, economic data from Europe and China have led to expectations of potentially weaker demand for crude oil. Eurozone gross domestic product (GDP) growth was 0.2% in the third quarter, and inflation was low at 0.3% and 0.4% in September and October, respectively. In China, third-quarter GDP growth was 7.3%, the lowest annual growth rate since first-quarter 2009.

The divergence of growth expectations between the United States and the rest of the world is also reflected in currency markets. As economic growth slows in countries other than the United States, it increases the likelihood that their central banks will implement further steps to stimulate growth, like the recent announcement of rate cuts and quantitative easing by the European Central Bank and the Bank of Japan. In the United States, stronger economic growth led the Federal Reserve to end its quantitative easing program and raises the possibility of increases in interest rates next year. These opposing shifts in monetary policy had the combined effect of increasing the value of the U.S. dollar against other world currencies (as measured by the U.S. dollar index) by 8.1% from August 1 to November 17.