from the Congressional Budget Office

[Editor’s Note: Based on the recent election results with Republican control of the USA purse strings, this will become an entertaining discussion for the 114th Congress]

To provide information about its plans beyond the coming year, the Department of Defense (DoD) generally provides a five-year plan, called the Future Years Defense Program (FYDP), that is associated with the budget it submits to the Congress. Because decisions made in the near term can have consequences for the defense budget in the longer term, ….

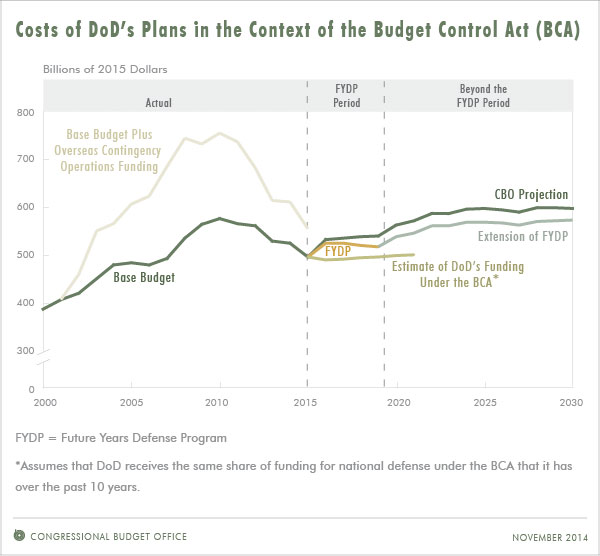

CBO regularly examines DoD’s FYDP and projects its budgetary impact for roughly a decade beyond the period covered by the FYDP. For this analysis, CBO used the FYDP that was provided to the Congress in April 2014; it spans fiscal years 2015 to 2019, and CBO’s projections span the years 2015 to 2030.

For fiscal year 2015, DoD requested appropriations totaling $555 billion. Of that amount, $496 billion was for the base budget and $59 billion was for what are termed overseas contingency operations (OCO). The base budget covers programs that constitute the department’s normal activities, such as the development and procurement of weapon systems and the day-to-day operations of the military and civilian workforce. Funding for OCO pays for U.S. involvement in the war in Afghanistan and other nonroutine military activities elsewhere. The FYDP describes DoD’s plans for its normal activities and therefore generally corresponds to the base budget.

DoD’s 2015 plans differ from its 2014 plans in important ways. For example, in an effort to reduce costs, the current FYDP includes sizeable cuts in the number of military personnel, particularly in the Army.

CBO produced two projections of the base-budget costs of DoD’s plans as reflected in the FYDP and other longterm planning documents released by DoD. The “CBO projection” uses CBO’s estimates of the costs of military activities and the extent to which those costs will change over time; those estimates reflect DoD’s historical experience. The “FYDP and extension” starts with DoD’s estimates of the costs of its plans through 2019 and extends them beyond 2019 using DoD’s estimates if available and CBO’s projections of price and compensation trends for the overall economy if DoD’s estimates are not available. Neither projection should be viewed as a prediction of future funding for DoD’s activities; rather, the projections are estimates of the costs of executing the department’s current plans without changes.

The amount requested for the base budget in 2015 would comply with the limits on budget authority established by the Budget Control Act of 2011 as subsequently modified, hereafter referred to simply as the Budget Control Act (BCA). After 2015, however, the costs of DoD’s plans under both projections would significantly exceed CBO’s estimate of the funding the department would receive under the BCA, which limits appropriations for national defense through 2021. To remain in compliance with the BCA after 2015, DoD would have to make sharp additional cuts to the size of its forces, curtail the development and purchase of weapons, reduce the extent of its operations and training, or implement some combination of those three actions.

The Inflation-Adjusted Costs of DoD’s Plans Would Increase By 1.2 Percent Per Year Through 2030 Under the CBO Projection

The costs to implement DoD’s 2015 plans would increase over the next 15 years in real terms (that is, after adjusting to remove the effects of inflation). Under the CBO projection, the real cost of the plans would start at $497 billion in 2015, jump to $533 billion in 2016, and continue growing thereafter, reaching $541 billion in 2019 and $598 billion in 2030 (see Figure below). The average annual growth rate of the cost from 2015 to 2030 would be 1.2 percent, resulting in a 20 percentincrease over the next decade and a half. CBO projects that the two largest parts of DoD’s budget would increase by different amounts and with very different profiles over that period:

- Operation and support (O&S)—which includes compensation for the department’s military and civilian employees, military health care, and various operation and maintenance activities—accounts for about two-thirds of the cost to implement DoD’s plans in 2015. CBO projects that those costs would rise fairly steadily between 2015 and 2030, with average growth of 1.1 percent a year in real terms and cumulative growth of 18 percent. That growth would occur despite a 6 percent decrease in the size of the military.

- Acquisition—which includes research, development, test, and evaluation as well as procurement of weapon systems and other major equipment—accounts for about one-third of the cost to implement DoD’s plans in 2015. CBO projects that those costs would jump by 42 percent in real terms between 2015 and 2022 but then trend downward through 2030. Costs in 2030 would be 22 percent higher than in 2015.

According to the CBO projection, the average real cost of DoD’s base-budget plans from 2015 through 2019 would exceed average spending for DoD from 1980 to 2014 by $64 billion a year. Moreover, the average real cost of DoD’s plans from 2015 through 2030 would exceed the 1980–2014 average by $105 billion a year.

The growth in DoD’s costs under the CBO projection would be somewhat less than CBO’s projection of the growth of the U.S. economy. Consequently, DoD’s costs as a share of gross domestic product (GDP) would decrease slowly over most of the projection period, from 2.8 percent of GDP in 2015 to 2.5 percent in 2025 and 2.3 percent in 2030.

The Inflation-Adjusted Costs of DoD’s Plans Would Increase By 1.0 Percent Per Year Through 2030 Under the FYDP and Extension

For most categories of DoD’s budget, costs under the CBO projection are higher than the costs estimated by DoD in the FYDP and the extrapolated costs for the extension of the FYDP. In particular, the growth reflectedin the CBO projection for military pay, the costs of developing and buying weapons, and the costs of providing health care is higher than the growth incorporated by DoD in the FYDP and extrapolated by CBO for the FYDP extension:

- Using DoD’s estimates of costs and CBO’s extension of those estimates, the real cost of DoD’s plans would grow at an average annual rate of 1.0 percent between 2015 and 2030, or 0.2 percentage points more slowly than under the CBO projection.

- Real O&S costs would rise by 1.0 percent a year, on average, during that period, or 0.1 percentage points more slowly than under the CBO projection.

- Real costs for acquisition would increase by 32 percent between 2015 and 2022, 10 percentage points less than under the CBO projection. As in the CBO projection, those costs would decline between 2022 and 2030.

The Costs of DoD’s Plans Would Significantly Exceed the Limits Established by the Budget Control Act

Although DoD has scaled back its plans since last year, CBO estimates that the cost of those plans after 2015 would still significantly exceed the funding that would be provided to the department under the BCA, which limits discretionary appropriations through 2021. If DoD continues to receive its historical share of the national defense budget, CBO’s analysis yields three conclusions:

- Under the CBO projection, the cumulative cost of DoD’s base-budget plans for 2015 through 2021 would be $332 billion, or about $47 billion a year, higher in nominal terms than the funding that would be provided to DoD under the limits set by the BCA. The gap would be $308 billion after adjusting for inflation.

- Under the FYDP and extension, the cumulative cost of DoD’s base-budget plans for 2015 through 2021 would be $215 billion, or about $31 billion a year, higher in nominal terms than the funding that would be provided under the BCA. The gap would be $200 billion after adjusting for inflation.

- Under either projection, the costs of DoD’s plans in the 2015 FYDP would be closer to the limits established by the BCA than would the costs of the plans in the 2014 FYDP. For example, between 2015 and 2021, the gap between the BCA’s limits and CBO’s projection for the 2015 plan is about half as large as the gap computed from CBO’s projection for the 2014 plan.

In any year for which discretionary appropriations are subject to the BCA, if the Congress appropriates more for DoD’s base budget than the amount permitted under the law, the difference between the appropriated amount and the BCA limit would be subject to sequestration (the cancellation of budgetary resources after they have been appropriated).