Texas factory activity rose sharply in January, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, rose from 3.5 to 12.9, which is consistent with faster growth.

Other measures of current manufacturing activity also indicated stronger growth in January. The new orders index jumped 13 points to 12.2, its highest reading since March 2011. The capacity utilization index shot up from 2.1 to 14.0, implying utilization rates increased faster than last month. The shipments index rose 9 points to 21.9, indicating shipments quickened in January.

Perceptions of broader business conditions were more positive in January. The general business activity index increased from 2.5 to 5.5, its best reading since March. The company outlook index also rose sharply to 12.6, largely due to a drop in the share of firms reporting a worsened outlook from 10 percent in December to 6 percent in January.

Labor market indicators reflected a sharp increase in hiring but flat workweeks. The employment index jumped out of negative territory to 8.7, with about 20 percent of employers reporting hiring and 11 percent noting layoffs. The average workweek index edged down to a reading of 0.8, which is consistent with unchanged hours worked.

Price and wage pressures increased in January. The raw materials price index moved up from 21.9 to 27.8, indicating input costs rose faster this month. The finished goods price index rose sharply from about zero to 10.2, its highest reading since February 2012. The wages and benefits index rose four points to 19.2, reflecting rising wage pressure, although the great majority of manufacturers continued to note no change in compensation costs. Looking ahead, 44 percent of respondents anticipate further increases in raw materials prices over the next six months, while 25 percent expect higher finished goods prices.

Expectations regarding future business conditions improved slightly in January. The index of future general business activity ticked up from 7.1 to 9.2. The index of future company outlook rose from 15.4 to 20.8. Indexes for future manufacturing activity moved up strongly this month.

Source: Dallas Fed

Summary of all Federal Reserve Districts Manufacturing:

Richmond Fed (hyperlink to reports):

/images/z richmond_man.PNG

Kansas Fed (hyperlink to reports):

/images/z kansas_man.PNG

Dallas Fed (hyperlink to reports):

/images/z dallas_man.PNG

Philly Fed (hyperlink to reports):

/images/z philly fed1.PNG

New York Fed (hyperlink to reports):

/images/z empire1.PNG

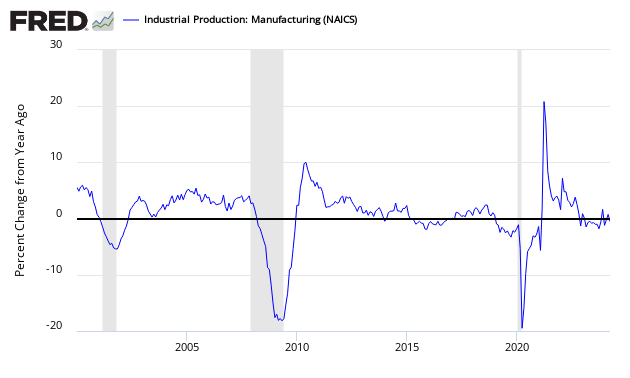

Federal Reserve Industrial Production – Actual Data (hyperlink to report)

Holding this and other survey’s Econintersect follows accountable for their predictions, the following graph compares the hard data from Industrial Products manufacturing subindex (dark blue bar) and US Census manufacturing shipments (lighter blue bar) to the Empire State Survey (green bar).

Comparing Surveys to Hard Data

![]()

/images/z survey1.png

In the above graphic, hard data is the long bars, and surveys are the short bars. The arrows on the left side are the key to growth or contraction.