by John Mauldin, Thoughts from the Frontline

“Economic stimulants produce Bridges to Nowhere. Strategic investment in infrastructure produces a foundation for long-term growth.”– Roger McNamee

“Our American ancestors prioritized growth and investment in our nation’s infrastructure.”– Cory Booker

“There are two Americas – separate, unequal, and no longer even acknowledging each other except on the barest cultural terms.”– David Simon

I, along with about 80 million of my fellow US citizens, watched the Clinton/Trump debate last Monday night. I am sure that we all have our own takeaways, and I won’t add my own thoughts on who won. But today’s letter is going to be about one of the few things the candidates agreed on: they both believe we need more infrastructure spending.

I am often asked to provide a summary to open my letter, and for this letter it really does make sense to offer one. I am going to make the following points herein:

- The next president is likely to face a recession early in his or her term; and the current, status-quo monetary and fiscal policy will ensure that it is a fairly serious recession with an even slower recovery than last time.

- The fiscal deficit will swell to at least $1.3 trillion and likely more. That will leave little room for fiscal spending and stimulus, and certainly not much for the usual infrastructure spending that is called for.

- The state of US infrastructure is appalling. It needs at least $3.6 trillion worth of repairs, and that does not even include what we need to do to prepare us for the 21st century. We have dug ourselves a very deep hole of massive failures on infrastructure upkeep, and we are continuing to dig. During Speaker of the House John Boehner’s tenure, one of the annual features was a speech by the speaker in which he would decry the state of our infrastructure, acknowledge that we needed to do something about it, and then once again say that we hadn’t figured out where to get the money.

- I offer a solution on where to find the money and actually give our children the tools they will need for 21st-century life, not to mention provide multiple millions of jobs and help to more evenly distribute the benefits of globalization and modernization – maybe even help bring back the middle class.

- I will offer a very brief summary of what we need to do on tax reform and regulatory reform and then note that if we do none of the above but stumble along doing what we have been doing, the investment environment is going to be exceedingly stressful; and pension funds and insurance companies are going to have massive difficulties staying in business, not to mention meeting the needs of tens of millions of retirees.

Coming: The Next Recession

I have touched on this subject several times in the recent past, but let’s do a quick recap.

The odds that the next president will face a recession during his or her first four years in office are quite high. Maybe not in the first year, but it is highly unlikely he or she will get more than two to three years without one. Given the fiscal reality that our next president will confront and the dwindling number of arrows left in the Federal Reserve’s monetary policy quiver, the administration is going to have a hard time dealing with the fallout from a recession.

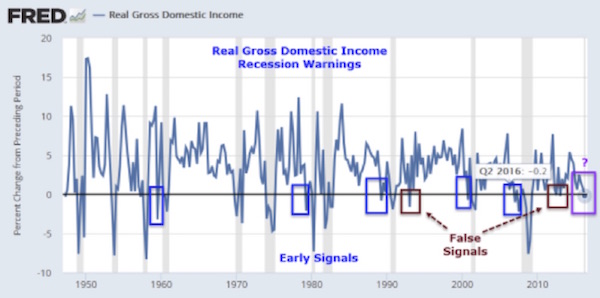

My friend Mike Shedlock (known as Mish in the world of bloggers [https://mishtalk.com/] and always a fascinating read) recently pointed out an interesting discrepancy between the gross domestic product (GDP) and the gross domestic income (GDI). Theoretically, they more or less measure the same thing, but from time to time there are discrepancies in the data. (Source: https://mishtalk.com/2016/09/30/real-gdi-provides-strong-recession-warning/)

The third estimate for second-quarter GDP was bumped up to 1.4%. However, GDI was marked down to -0.2%. That is a rather large discrepancy. Because the data sources for the two measures are different, GDP and GDI can diverge from time to time (even though they merge over the long term). Many economists actually prefer to look at GDI, though you would never know that from the mainstream media. So why do they look at GDI? Let us do a little quoting from Mish:

The basic difference between the two is that GDP measures what the economy produces – goods, services, technology, intellectual property – while GDI measures what the economy makes, tracking things like wages, profits, and taxes.

There are substantive reasons for economists and market participants to focus on GDI rather than the traditional GDP number. In theory, the two numbers should be the same, as both are designed to measure the aggregate growth of the economy. GDP measures what the economy produces, GDI measures what it takes in.

But because they use different data sources, these readings are subject to measurement error, though the BEA notes they tend to follow similar paths over time. A main difference in their inputs is tax receipts, with GDI taking into account taxes on production and imports, as well as subsidies, net interest, and miscellaneous payments.

Since the financial crisis, first-quarter GDP has consistently lagged growth during the second, third, and fourth quarters. And the whole point of the government “seasonally adjusting” the data is to smooth out these variances and give markets and the public a more reliable, consistent picture of the country’s economic health. Given the repeated failures of the first quarter to be anything other than a disappointment, it seemed that something was off.

As currently tabulated, GDP was a big disappointment in the first quarter. As currently tabulated, GDI showed an economy that is still growing.

And with lingering issues around how the government adjusts its GDP data, Deutsche Bank Securities Chief US Economist Joseph LaVorgna argued in a note on Friday, “The drop-off in estimated Q1 GDP growth has not altered our view that the underlying fundamentals of the economy remain on firm footing.”

However, Mish notes that GDI may now be signaling that a recession is impending. Please note that he points out that while a negatively growing GDI is not an infallible indicator, it is on balance right more often than wrong, and thus we should at least have our antennae up. He then gives us a chart for GDI, which he has helpfully marked up:

Whereas real GDP was revised up 0.3 percentage points, real GDI was revised lower by 0.4 percentage points, to -0.2%.

A quick glance at the recession bars in the above chart shows what negative GDI numbers traditionally mean.

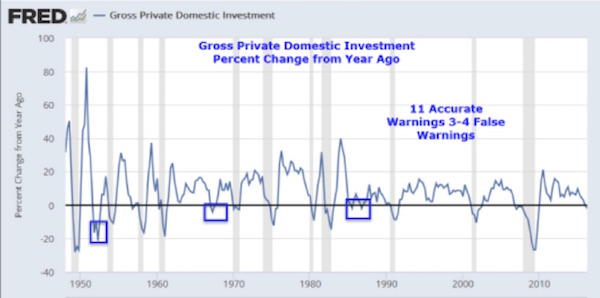

And then he goes on to note that this signal is being confirmed by the data for real private gross domestic investment.

Real private investment (not to be confused with income) is a measure of investment in the real economy, not under the influence of massive amounts of government spending. The numbers are not pretty.

There are numerous other indicators that show the economy is getting softer, even as you can find additional indicators (generally financially oriented) that lead you to have a more sanguine, if not overly optimistic, view. But the point is that the economy is running at stall speed, and any shock that comes from outside the US – from Europe or Japan or China – or from an actual honest-to-God initiation of interest rate hikes by the Fed, which would force a repricing of bonds and equities, could set off a recession that would become self-reinforcing.

Pay attention to Deutsche Bank. The bank is deeply connected with the entire global banking market, and just as Lehman Brothers triggered a rolling wave of panic, Deutsche Bank has a similar potential. Even though Merkel swears she is not going to bail out Deutsche Bank, she will have no choice. They will probably have to wipe out shareholders and maybe even some subordinated debt, but they cannot let the bank itself go under, because it is at the center of a massive financial spiderweb. Which means that the German central bank will have to be at the center of the rescue, and it gets its capital from the ECB. Watch how quickly Italy, Spain, and the rest of Europe demand that the ECB bail out their banks, too. So the last thing Germany will want to do is bail out Deutsche Bank. This is a very complicated theater plot in Europe, and it is hard to follow all the disparate plot lines, but we have to try. Now back to the US and the coming recession…

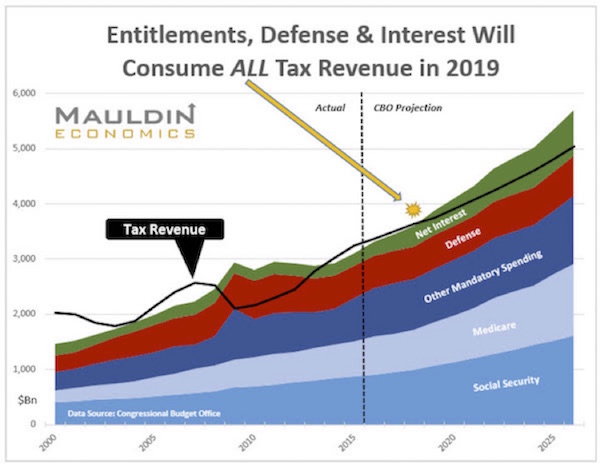

Let’s look at fiscal reality. Sometime in the first year of the next presidential term, the US national debt will top $20 trillion. The deficit is running close to $500 billion, and the Congressional Budget Office projects that figure to rise. Add another $3 trillion or so in state and local debt. As you may imagine, the interest on that debt is beginning to add up, even at the extraordinarily low rates we have today.

Sometime in 2019, entitlement spending, defense, and interest will consume all the tax revenue collected by the US government. That means all spending for everything else will have to be borrowed. The CBO projects the deficit will rise to over $1 trillion by 2023. By that point entitlement spending and net interest will be consuming almost all tax revenue, and we will be borrowing to pay for our defense. Let’s look at the following chart, which comes from CBO data:

By 2019 the deficit is projected to be $738 billion and rapidly approaching $1 trillion. Almost every president wants to run for a second term. To forge any hope of being successful with that second run, a president needs to able to say that he or she made a difference on the budget. There are only three ways to reduce the deficit: cut spending, raise taxes, or authorize the Federal Reserve to monetize the debt (or some combination of the three). At the numbers we are now talking about, getting rid of fraud and wasted government expenditures is a rounding error. Presidents since McKinley in the 1890s have been talking about cutting waste and fraud. It is not as though Reagan, Bush, Clinton, Bush 2, and Obama have not tried to cut waste and fraud. But for the sake of the argument, let’s say you could find $100 billion here or there. You are still a long, long way from a balanced budget.

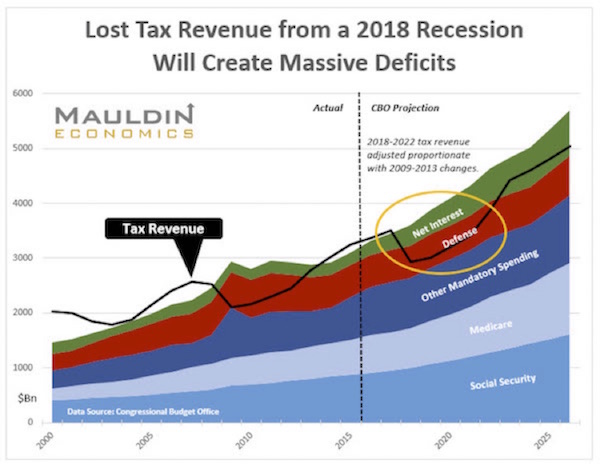

But implicit (and this is critical!) in the CBO projections is the assumption that we will not have a recession in the next 10 years. Plus, the CBO assumes growth above what we’ve seen in the last year or so. Let’s contemplate what a budget might look like if we have a recession. I asked my associate Patrick Watson to look at past recessions and determine what level of revenue losses occurred because of them and then to assume the same average percentage revenue loss for the next recession. We more or less randomly decided that we would hypothesize our next recession to occur in 2018. If it happens in 2017 or 2019 instead, the relative numbers are the same, and so is the outcome: it would blow out the budget. Here’s a chart of what a recession in 2018 would do. Entitlement spending, defense, and interest would greatly exceed revenue.

The deficit would balloon to a minimum of $1.3 trillion, and if the recovery occurs along the lines of our last (ongoing) recovery, then unless we reduce spending or raise revenues, we will not see deficits below $1 trillion over the ensuing 10 years. The deficit will climb to $1.5 trillion just as the president dives into the thick of a second campaign in 2020. Not exactly a great campaign platform. And that is the known budget deficit. Off-budget additions to the national debt could be as much as one-half trillion dollars.

Bluntly, in such an environment there will be very little room to do any sort of infrastructure or stimulus spending.

However, we desperately need to repair and replace a vast part of our national infrastructure. We have legions of former manufacturing workers and young people whom we need to put to work. And we need to remove as many impediments to economic growth as possible. We can do all three with an aggressive, Federal Reserve-funded infrastructure program.

Failing Grades

You might respond that the roads and bridges are just fine and we don’t need more boondoggle spending. That may well be true wherever you live. It is certainly not true for the nation as a whole. The needs vary, but they definitely exist.

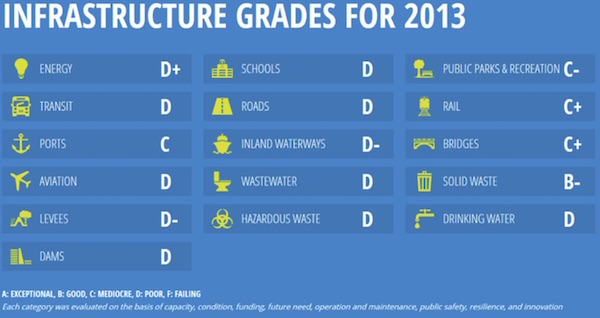

The American Society of Civil Engineers has been preaching this message for a long time. They publish a national Infrastructure Report Card every four years. The last one was in 2013, so it’s a bit dated now, but I feel confident that few of the problems have disappeared. And enough new ones have probably emerged to replace whatever we’ve taken care of since 2013.

Here is your report card, America:

I haven’t seen grades this low since the 2nd grade when I got a D in penmanship. I was not smart enough at the time to point out that that qualified me to be a medical doctor. We voters aren’t holding our legislators to account – maybe because many of these problems aren’t very exciting. “Fix the Levees!” isn’t exactly a vote-winning slogan unless the water is rising on election day. If you build something new, you get to cut the ribbon and look like you did something.

ASCE concludes we need to invest $3.6 trillion by 2020 in order to bring the national infrastructure up to par. Is that a lot of money? Yes. But we need to spend it, or our infrastructure will continue to crumble. Negligence will take us ever closer to a Blade Runner type of world.

You can drill down to state level in the ASCE site to see what your part of the country needs. I can remember when visitors from other states envied our Texas highway system. Now we earn a D grade for highways. Texas ranks 43rd in the nation for per capita highway spending. According to the Federal Highway Administration’s Bridge Inventory, 146,633 out of 604,474 bridges in the United States are structurally deficient or functionally obsolete. That’s a whopping 24.3 percent of all bridges in the country. Bridges are typically built to last 50 years, and today’s average bridge is 45 years old. See the problem?

Ironically, the federal money for highways comes from the gas tax, which has not increased since 1993, which means it is not keeping up with inflation. Our gas taxes have lost at least a third of their purchasing power since then. Further, our cars get more miles per gallon than they did, so we are using less gas to go farther. Which is a good thing except that it means we have less money to repair roads. Friday night I went to dinner with a friend who drove us in his new Tesla. He does not pay any gas taxes to help fund the roads that we were driving on. I know we think of the gas tax as a tax, but it is more of a user fee for people who use roads. If you do not use the roads, then fine. If you do, you should be willing to pay for them.

Most people think of roads and bridges when we use the term infrastructure. (Interestingly, the word infrastructure only came into common use in the 1980s. Prior to that it was called “public works.”) We really should think of infrastructure as the things that allow us to move food, energy, water, products, people, and information. It is our rail and trucking systems. It is our electric grid. It is our telephone system, internet, and other information systems. To some degree it is our school systems. It is the things that make it possible for businesses and governments to provide the services and goods we all expect. We all assume that when we flip the switch, the light will go on; and when we set the thermostat, the heat or air-conditioning will turn on. We assume these things are automatic, but they have to be maintained, and we are not maintaining them well.

Let’s look at a few items that may not be on your radar screen. In my backyard, Texas has 1,046 non-federal dams rated “high hazard.” That means their failure would bring a probable loss of life. Will they fail? No one knows because most of them have no regular inspections or maintenance. We have about one inspector for every 1,400 dams in Texas. Alabama has no inspectors for their dams. The average dam has a life of about 50 years, and many of the dams in the United States are much older than that. They need to be repaired before they become a disaster for those downstream.

According to the Center for American Progress, there are 240,000 water main breaks every year, and as much as 25% of the treated water that enters the distribution system is lost through leakage. There are 75,000 overflows every year in the US from our sewage system, and they dump something like 900 billion gallons of untreated sewage into our lakes, rivers, streams, and bays. The American Water Works Association estimates it will take $1 trillion to repair and replace the drinking water system over the next 25 years. It takes $3 billion a year just for emergency repairs.

I could spend an entire letter on how antiquated our electrical grid is. It was designed long ago in a galaxy far away to meet needs that were much more simple and limited than those it must meet today, yet we are still stuck with it. One estimate is that we lose about $49 billion a year to power outages. The solution is something called a Smart Grid, but you are talking tens of billions of dollars, and nobody wants to put up the money to fix the whole system, so every jurisdiction functions more or less on its own without much coordination.

Think about our ports (which nobody really does). They need a massive upgrade rather than the piecemeal efforts that are underway now. Many of our ports can no longer handle the latest technologies. And while some airports are being upgraded, others are embarrassing.

And while few people thinks of it as infrastructure, our information system is the very backbone of modern society; and with a little pressure from Congress the FCC could open up some more bandwidth and we could provide high-speed, nearly free internet services throughout most of the US.

And to get all science fiction on you, there are close to half a dozen major maglev train projects that have serious funding in the United States. It is not just Elon Musk – and it is not clear that he will be the winner. And while I wouldn’t suggest that we have public funding for them, at least not initially, maglev trains could become a reality within 5 to 10 years if existing prototype systems can be built out.

Finding the Money for Infrastructure

If the ASCE estimated $3.6 trillion to repair our infrastructure in 2013, care to take the over or the under that the figure will top $4 trillion the next time they do an estimate? And that is just to repair and rework what we have; that is not what will be needed to actually propel us into the 21st century. The total could be a multiple of that over the next 10 to 15 years. Now we are starting to talk serious money. But if we pay our dues and do that work, then the next generation will get something worthwhile for their tax money rather than the close to $20 trillion worth of debt that we have now, which has produced damn little.

So where do we get the money? Before tuning me out before the end of the next sentence, read my whole proposal, down to where I get into how to control the actual disbursement of the funds.

First, I would propose that Congress authorize something along the lines of a Ginnie Mae bond for infrastructure spending. Ginnie Mae bonds have the full faith and credit of the US government behind them but are paid for by the homeowners who pay their mortgages. But the bonds allow them to get cheaper mortgages. After that authorization, strongly suggest, or even require, that the Federal Reserve put those bonds on its balance sheet, selling Ginnie Mae bonds if the Fed wants to maintain its total asset base. The Ginnie Mae (and Fannie and Freddie) bonds would be readily bought back by the market if they were available..

The bonds would fund projects pursued by cities, counties, and states that have a tax base or other resource to pay for the bonds. (I do not want to go into this in detail here, but there are some legal prohibitions on certain types of government infrastructure spending.)

It is clear that you could put a small surcharge on a local water bill to pay for rebuilding and modernizing the local water system. Ditto for the electric grid. Roads are a little trickier as there has to be a tax base willing to carry the load. But an infrastructure bond guaranteed by the US government would carry a much lower interest rate. And there are ways to make that interest rate even lower.

US 30-year bonds are at 2.3% as I write. If you allowed local and state governments to borrow only for new infrastructure at 2.3% and created willing markets for their bonds, we would see a lot of infrastructure being built.

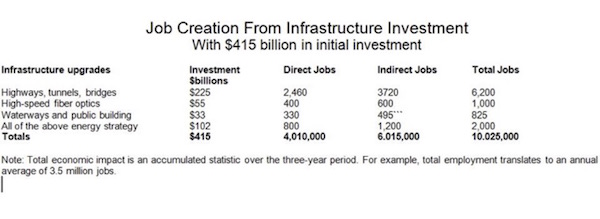

The following chart shows that an investment of $415 billion could create more than 10 million jobs. Frankly, we would be lucky to be able to deploy $500 billion a year in infrastructure spending. The Forbes article from which the chart came did not cite its source, and my guess is that the spending would not really create 10 million jobs; but even half that number of jobs would change the nature of employment for middle-class Americans who are losing manufacturing and other jobs and who would have the skills to build what we need. I do not particularly agree with Forbes’ allocation of dollar resources, but the point here is that an infrastructure program would create a large number of jobs that would be a huge boost to an economy struggling through a recession. If the program were started early enough in the next administration, it might even keep us out of one.

Now, the tricky part. I can hear half my readers objecting that this has the potential to be a massive boondoggle. I totally agree, so structures have to be built in to keep it from becoming one. I would create an independent commission of 10 to 12 people who are actually businesspeople and have not been elected politicians for at least 10 years. No “community workers,” no activists, nobody who has not had responsibility for a payroll, just people with more than a few years of experience in the real world. This is not a commission that tries to fix political problems or correct whatever injustices people see in our country but rather tackles physical infrastructure problems. Their role is to sift through the proposed projects and make sure they are real-world projects with long-term benefits and not just somebody’s pet project.

The commission members would have to recuse themselves from any vote on a project in their home state. Their mandate would be to make sure that each proposed project makes sense and that there is at least a 95% probability that the local or regional tax base could pay for the project.

No investments in any companies for research. If Congress wants to authorize that sort of work separately, that is up to them. With the exception of DARPA and to some extent the National Science Foundation, investments in research by government have not been very good. (As an aside, if it were up to me, I would triple DARPA’s budget and try to figure out what it is they’re drinking and give it to more government agencies.)

Likewise, this program would not be a piggy bank for education programs or training programs or anything else the Congress wants. This is infrastructure, which needs to be clearly defined in the authorizing legislation. No projects that would replace private industry in favor of government control. Just roads and bridges and ports and dams and water systems and the like.

I would require that every entity that borrows money, whether it is a local jurisdiction, county, or state, actually hold a vote to approve the bond, with language clearly indicating that taxpayers or users of the service will be responsible for paying for it. If the funding to repay the bond is determined by independent auditors to be suspect, then local taxpayers would have to agree to a special tax to pay for the bonds. Toll highways move to the front of the line.

My personal preference would be that low bid wins and no requirement for union labor, at least in states that are right-to-work states. If taxpayers want to pay extra for union labor, that is their choice.

Now, since I have ventured into the realm of the controversial, let me really get out over my ski tips. The US has spent hundreds of billions of dollars trying to fix Iraq and Afghanistan and God knows how many more hundreds of billions of dollars over the years on other projects around the world. What if we renewed the focus on our own needs?

If the US government subsidized these infrastructure bonds by 2%, then local governments would be paying, at today’s rate, only something like 0.3% in total interest. Tack on an extra 10 or 20 basis points for servicing and the cost of the commission and losses, and a local government would be able to borrow at about 0.5%. If cost ends up being higher, then the servicing cost goes up by 10 basis points. The point is to make local governments pay for their projects, less the subsidy from the government for interest rates. Essentially, that subsidy is a rounding error in the total cost, and it would allow governments to start infrastructure projects today and have 30 years to pay them back.

I would provide the subsidy only for a limited period of time (say four years), in order to encourage infrastructure projects to get off the ground now and thus kick-start employment. This program would go a heck of a lot further to reduce income inequality than any ridiculous transfer system that takes money from the rich and tries to give it to the poor.

Let us say that by some miracle we could actually deploy $3-4 trillion in infrastructure spending over the next 10 years. We would be lucky to actually spend $2 trillion in the first 4 years, but let’s assume that we get all industrious and do it. If we assume a subsidy cost of 2% for the bonds, then 2% of $2 trillion is $40 billion a year. That is about 1% of our total federal expenditures. It is only about 7% of our defense budget.

Rebuilding our water systems – which, if estimates are correct, would save up to 20% of the water we are using as well as massive costs for emergency repairs – would actually pay for itself.

If you combine this type of program with massive tax reform, you could reposition the country to be the most powerfully competitive nation in the world. (I apologize to my international readers, but I am being a total home fanboy here. There is no reason that the same thing wouldn’t work in your country as long as there was a demand for your government bonds.)

I have written about my suggested tax reforms elsewhere, in a piece I co-authored with Steve Moore. Basically, we proposed a maximum 15% corporate tax with absolutely no loopholes. Every penny above $100,000 is taxed. Income earned offshore is taxed at 10%, period, so you might as well bring it back in and put it to work here. I believe it is possible to make the tax look like a VAT rather than an income tax or to structure it so that the purpose would be the same, so that companies exporting products would basically pay no taxes on their exports, which is what happens in Europe and the rest of the world. It puts our corporations on an even basis.

Cap the income tax at 20% with no deductions for anything. Institute a VAT tax, which would allow for us to eliminate Social Security taxes, which would be an immediate boost in income to the middle class. Adjust the VAT tax to allow for a reasonable safety net, and go back to Bill Clinton-style welfare reform. Remember when President Clinton proudly stood up and said, “We are ending big government as we know it”? Who knew Republicans would someday be nostalgic for Bill Clinton? (Although I would point out that my friend Newt Gingrich was a big reason that Clinton’s programs were so successful. Their partnership – the last truly successful example of bipartisanship – resulted in a completely balanced budget within a few years. And that was after Ross Perot ran on a platform warning that we were facing total disaster as a nation. That time – the early ’90s – was not unlike the situation we face today, but I am not so hopeful now of bipartisan working relationships.)

Change the regulatory environment to one designed for the 21st century rather than the 19th century and set our companies free to compete and create jobs. Ah, but I dream…

What Happens If We Do Not?

If we do not do something like this when we go into recession, especially if Hillary Clinton wins, the same central bankers who are running the system today will give us the same tired monetary programs, which will have the same lack of results, except this time unemployment will be higher and the recovery will leave us looking more like Europe and Japan. Retirement plans and pension plans, which are based on long-term historical performance, will be devastated, and the Boomer generation will not be able to retire as they had hoped.

It is getting close to time to hit the send button, but over the next few months we will get into what your investment responses should be to the situation I’ve described.