by John Mauldin, Thoughts from the Frontline

“Retirement is like a long vacation in Las Vegas. The goal is to enjoy it to the fullest, but not so fully that you run out of money.”– Jonathan Clements

“In retirement, only money and symptoms are consequential.”– Mason Cooley

Retirement is every worker’s dream, even if your dream would have you keep doing the work you love. You still want the financial freedom that lets you work for love instead of money.

This is a relatively new dream. The notion of spending the last years of your life in relative relaxation came about only in the last century or two. Before then, the overwhelming number of people had little choice but to work as long as they physically could. Then they died, usually in short order. That’s still how it is in many places in the world.

Retirement is a new phenomenon because it is expensive. Our various labor-saving machines make it possible at least to aspire to having a long, happy retirement. Plenty of us still won’t reach the goal. The data on those who have actually saved enough to maintain their lifestyle without having to work is truly depressing reading. Living on Social Security and possibly income from a reverse mortgage is limited living at best.

In this issue, I’ll build on what we said in the last two weeks on affordable healthcare and potentially longer lifespans. Retirement is not nearly as attractive if all we can look forward to is years of sickness and penury. We are going to talk about the slow-motion train wreck now taking shape in pension funds that is going to put pressure on many people who think they have retirement covered. Please feel free to forward this to those who might be expecting their pension funds to cover them for the next 30 or 40 years. Cutting to the chase, US pension funds are seriously underfunded and may need an extra $10 trillion in 20 years. This is a somewhat controversial letter, but I like to think I’m being realistic. Or at least I’m trying.

The Transformation Project

But first, let me update you on the progress on my next book, Investing in an Age of Transformation, which will explore the changes ahead in our society over the next 20 years, along with their implications for investing. Our immediate future promises far more than just a lot of fast-paced, fun technological change. There are many almost inevitable demographic, geopolitical, educational, sociological, and political changes ahead, not to mention the rapidly evolving future of work that are going to significantly impact markets and our lives. I hope to be able to look at as much of what will be happening as possible. I believe that the fundamentals of investing are going to morph over the next 10 to 15 to 20 years.

I mentioned a few weeks ago at the end of one of my letters that I was looking for a few potential interns and/or volunteer research assistants to help me with the book. I was expecting 8 to 10 responses and got well over 100. Well over. I asked people to send me resumes, and I was really pleased with the quality of the potential assistance. I realize that there is an opportunity to do so much more than simply write another book about the future.

What I have done is write a longer outline for the book, detailing about 25 separate chapters. I’d like to put together small teams for each of these chapters that will not only do in-depth research on their particular areas but will also make their work available to be posted upon publication of the book. We’re going to create separate Transformation Indexes for many of the chapters, which will certainly be a valuable resource and a challenge for investors.

If you are interested in getting involved, drop me a note with your resume to [email protected]. I will send you the book outline, and you can decide what area you would like to work in or whether you are willing to go where we need you.

And now let’s look at what pension funds are going to look like over the next 20 years.

Midwestern Train Wreck

Four months ago we discussed the ongoing public pension train wreck in Illinois (see Live and Let Die). I was not optimistic that the situation would improve, and indeed it has not. The governor and legislature are still deadlocked over the state’s spending priorities. Illinois still has no budget for the fiscal year that began on July 1. Fitch Ratings downgraded the state’s credit rating last week. It’s a mess.

Because of the deadlock, Illinois is facing a serious cash flow crisis. Feeling like you’ve hit the jackpot through the Illinois lottery? Think again. State officials announced Wednesday that winners who are due to receive more than $600 won’t get their money until the state’s ongoing budget impasse is resolved. Players who win up to $600 can still collect their winnings at local retailers. More than $288 million is waiting to be paid out. For now the winners just have an IOU and no interest on their money (Fox).

As messy as the Illinois situation is, none of us should gloat. Many of our own states and cities are not in much better shape. In fact, the political gridlock actually forced Illinois into accomplishing something other states should try. Illinois has not issued any new bond debt since May 2014. Can many other states say that?

Unfortunately, that may be the best we can say about Illinois. The state delayed a $560 million payment to its pension funds for November and may have to delay or reduce another contribution due in December.

Illinois and many other states and local governments are in this mess because their politicians made impossible-to-keep promises to public workers. The factors that made them so impossible apply to everyone else, too. More people are retiring. Investment returns aren’t meeting expectations. Healthcare costs are rising. Other government spending is out of control.

Nonetheless, the pension problem is the thorniest one. State and local governments spent years waving generous retirement benefits in front of workers. The workers quite naturally accepted the offers. I doubt many stopped to wonder if their state or city could keep its end of the deal. Of course, it could. It’s the government.

Although state governments have many powers, creating money from thin air is, alas, not one of them. You have to be in Washington to do that. Now that the bills are coming due, the state’s’ inability to keep their word is becoming obvious.

Now, I’m sure that many talented people spent years doing good work for Illinois. That’s not the issue here. The fault lies with politicians who generously promised money they didn’t have and presumed it would magically appear later.

On the other hand, retired public workers need to realize they can’t squeeze blood from a turnip. Yes, the courts are saying Illinois must keep its pension promises. But the courts can’t create money where none exists. At best, they can force the state to change its priorities. If pension benefits are sacrosanct, the money won’t be available for other public services. Taxes will have to go up or other essential services will not be performed. This is certainly not good for the citizens of Illinois. As things get worse, people will begin to move.

What happens then? Citizens will grow tired of substandard services and high taxes. They can avoid both by moving out of the state. The exodus may be starting. Crain’s Chicago Business reports:

High-end house hunters in Burr Ridge have 100 reasons to be happy. But for sellers, that’s a depressing number. The southwest suburb has 100 homes on the market for at least $1 million, more than seven times the number of homes in that price range – 14 – that have sold in Burr Ridge in the past six months. The town has the biggest glut by far of $1 million-plus homes in the Chicago suburbs, according to a Crain’s analysis.

“It’s been disquietingly slow, brutally slow, getting these sold,” said Linda Feinstein, the broker-owner of ReMax Signature Homes in neighboring Hinsdale. “It feels like the brakes have been on for months.”

We don’t know why these people want to sell their homes, of course, but they may be the smart ones. They’re getting ahead of the crowd – or trying to. Think Detroit. I have visited there a few times over the last year, and the suburbs are really quite pleasant (except in the dead of winter, when I’d definitely rather be in Texas). But those who moved out of the city of Detroit and into the suburbs many decades ago had a choice, because Michigan’s finances weren’t massively out of whack.

I’ve been to Hinsdale. It’s a charming community and quite upscale. It is an easy train commute to downtown Chicago.

Look at it this way: with what you know about Illinois public finances, would you really want to move into the state and buy an expensive home right now? I sure wouldn’t. That sharply reduces the number of potential homebuyers. The result will be lower home prices. I’m not predicting Illinois will end up like Detroit… but I don’t rule it out, either.

Further, more and more cities and counties around the country are going to be looking like Chicago. Wherever you buy a home, you really should investigate the financial soundness of the state and the city or town.

Pension Math Review

Political folly is not the only problem. Illinois and everyone else saving for retirement – including you and me – make some giant assumptions. Between ZIRP and assorted other economic distortions, it is harder than ever to count on a reasonable real return over a long period.

Small changes make a big difference. Pension managers used to think they could average 8% after inflation over two decades or more. At that rate, a million dollars invested today turns into $4.7 million in 20 years. If $4.7 million is exactly the amount you need to fund that year’s obligations, you’re in good shape.

What happens if you average only 7% over that 20-year period? You’ll have $3.9 million. That is only 83% of the amount you counted on.

At 6% returns you will be only 68% funded. At 5%, you have only 57% of what you need. At 4%, you will be only 47% of the way there.

This math works the same way no matter how many zeroes you put behind the numbers. Each percentage point of return makes a huge difference. Missing your target just slightly can have big consequences.

Keep in mind these need to be real, after-inflation returns. Inflation is not a problem right now. How much will you bet that it will stay under control for the next two decades? You might be right – and then again you might be wrong, so you really need to aim even higher. Retirement incomes are not something that should be gambled with.

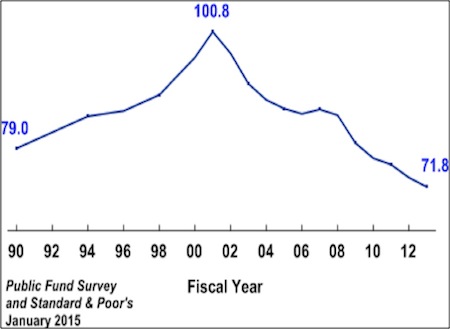

Pension managers know this, of course. The National Association of State Retirement Administrators has some good data on its member’s activities. Their Public Fund Survey has data on public retirement systems covering 12.6 million active workers and 8.2 million retirees and beneficiaries. At the end of FY 2013 (the latest data they show), members had $2.86 trillion in assets. That is about 85% of all state and local government retirement assets. This data is comprehensive, though a little outdated.

The average public retirement system funding level in FY 2013 was 71.8%. That number has been trending steadily downward since the survey began. In 2001, it was a healthy 100.8%.

This is not a good trend. What is the problem? Here is how NASRA explains it.

Figure B [shown above] presents the aggregate actuarial funding level since 1990, measured by Standard & Poor’s from 1990 to 2000 and the Survey since 2001. This figure illustrates the substantial effect investment returns have on a pension plan’s funding level: investment market performance was relatively strong during the 1990s, followed by two periods, from 2000–2002 and 2008–09, of sharp market declines. Other factors that affect a plan’s funding level include contributions made relative to those that are required, changes in benefit levels, changes in actuarial assumptions, and rates of employee salary growth.

The average state and local retirement system can pay only roughly 72% of its obligations as of now. That means state and local governments need to come up with an additional $1 trillion or more. Some states, of course, are 100% funded. Some have barely half the needed funding. That is a lot of money for financially strapped states to come up with. I can’t think of any reason to believe the situation will get better. I can imagine quite a few scenarios in which it will get worse.

Looking at the assumptions, the median plan in the Public Fund Survey assumed 7.9% annual investment returns and 3.0% inflation. The average asset allocation was 50.7% equities, 23.2% fixed income, 7.2% real estate, and 15.1% alternatives, with the rest in cash and “other.”

I’ve played with those numbers using what I think are reasonable return expectations. I can’t find any combination that would bring the real return after inflation up to the 5% area that the plans need. That means the 71.8% funding ratio is too optimistic. It is somewhere below that level. How far below? We’ll know in 20 years. (We will look at some scholarly projections of future portfolio potentials in a moment.)

If you are a state or city worker in one of these severely underfunded systems, or a recently retired one, now is an excellent time to develop your Plan B. Your chance of getting the full amount you were promised is somewhere between slim and none. The money simply isn’t there.

Private Plans No Better

If you are a corporate worker and think your plan is better than those managed by politically driven bureaucracies, you may want to rethink your position.

First, you should (probably) thank your lucky stars if you have some kind of defined benefit plan. Such plans are an endangered species outside of government and union-run plans. Most workers now are lucky to get a 401K that shifts responsibility off the company’s shoulders and onto theirs.

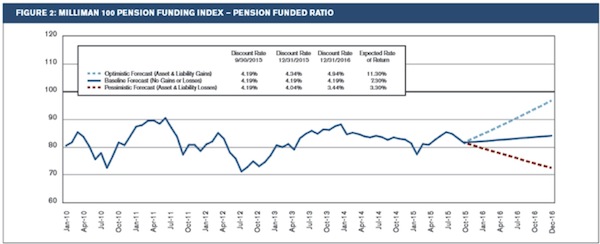

On the off chance that you do have a defined benefit pension, on average that pension plan is likely to be in the same boat as the governmental plans discussed above. Actuarial firm Milliman, Inc., tracks these plans and has a handy “Milliman 100 Pension Funding Index.” It tracks the 100 largest corporate defined benefit plans.

As of September 2015, Milliman data shows these 100 plans had a funded percentage of 81.7%. They are collectively $312 billion below where they ought to be. This is actually better than where they began 2015. The chart below shows this figure monthly since 2010.

The dotted lines are Milliman’s optimistic, baseline, and pessimistic forecasts. The baseline scenario’s expected rate of return is 7.3%. I would call that excessive, for the same reasons we will discuss in a moment. I think their optimistic 11.3% return is very unlikely to pan out, and the pessimistic 3.3% is not pessimistic enough.

In short, the suggestion I made for public workers applies to private workers, too. If you don’t have Plan B, start working on one now.

Central Banks Print Money – Pension Funds Assume Money

Pension fund boards are typically populated by political appointees and representatives from the various pension groups. In an effort to make sure they are making realistic projections (and after they have been on the board for a few months, when they understand how serious the task is), they hire outside consultants. The pension-consulting gig is lucrative and very competitive. It is also quite political.

It is political because the assumptions you make about your future returns directly affect state and city budgets. Typically, states require themselves to “dollar-cost average” their funding over time so that pension funds stay fully funded. If you reduce the future returns you expect to make on your investments, you increase the amount of present-day funding needed from the various government entities.

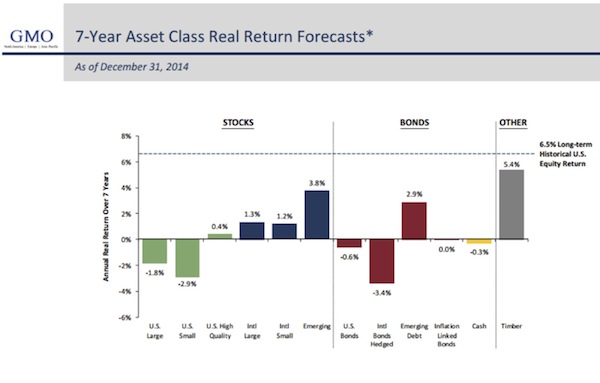

The average pension fund is 71.8% funded. But that’s assuming high returns. What are returns actually likely to be? Let’s look at a few estimates by professionals. First, the folks at GMO annually make a seven-year real return forecast. This is the one from the end of last year:

Note that US stocks are projected to produce negative returns. US pension funds are heavily weighted to US markets. Even adding in developing-market equities would still leave you with negative returns. I highly doubt that any pension-fund consultant would suggest that their clients aggressively overweight emerging-market equities. Now, look at the returns for bonds.

This forecast would suggest that, over the next seven years, returns will be negative for the balanced portfolios that most pension funds have. If GMO is correct, pension funds will require significant state and local funding to make up the difference, .

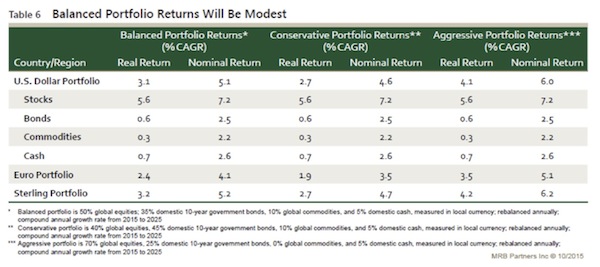

The Macro Research Board (MRB) recently developed a total portfolio forecast for dollar, euro, and pound sterling portfolios. They made detailed forecasts for equities, bonds, currencies, and commodities, taking into consideration inflation and global growth. These are guys I take very seriously, as their forecasting methods are rigorous. Let’s go straight to their 10-year forecast.

The average US pension fund, according to the data above, can expect returns somewhere between MRB’s balanced and aggressive portfolio projections. That suggests positive real returns of around 3.6% for US pension funds – a far cry from the almost 6% that most funds are projecting and nearly two full points lower than many pension funds are currently anticipating. MRB’s projections mean that today such funds actually have only 68% of what they need to be fully funded in 20 years.

Do you think MRB’s forecasts are pessimistic? Actually, the assumptions they make and their projections are more generous than the ones I would make and also exceed the more conservative GMO assumptions. I could go tick off a whole host of reasons why I think growth is going to be slow (though not fall off the cliff), but there isn’t enough room today. Suffice it to say that I still believe in my Muddle Through economic scenario.

But since funds are already funded at only about 72% of what it would take to pay promised benefits to retirees, the math means that funds have less than 50% of the money they need currently in their accounts. Since funds have $2.86 trillion (give or take), then no matter how you slice it, pension funds are underfunded today by about $2 trillion, if you assume MRB’s projections are correct. Since pension funds are forecasting that they will grow their funds almost fivefold, that means a future shortfall in the neighborhood of $10 trillion, which during the intervening time is going to have to be made up from tax revenues.

Of course, I made a lot of assumptions in the preceding paragraph. What if states decide to aggressively start making up the shortfall? That would certainly reduce the ending deficit. There are other factors that could positively affect returns as well. This is certainly a back-of-the-napkin estimate; but if I am wrong, it is only in the final destination and not in the direction of the problem. Pension funding is going to be a huge burden on government budgets everywhere, in a time when they are already strained.

On top of that, add in the cost to the government of Social Security and other entitlements. Further compounding the problem, as I demonstrated over the past two weeks, is the very real potential that the average person retiring today will live 10 years longer than actuaries currently predict. Various estimates say entitlements in the US will run to the tune of $80 trillion over time. And the situation is just as bad in Europe. In fact, many countries in Europe are in worse shape than the US.

You’re On Your Own

There are no easy answers for individuals here. I think more and more potential retirees will find it necessary to continue working. Further, you should plan on living a great deal longer than you probably assume in your current financial plan. And unless your financial manager is a wizard, you should seriously think about what kind of returns she can produce for you and what level of withdrawals you can actually afford. The 5% annual withdrawal that many financial planners use in their models is simply not realistic in today’s low-yield world.

Making sure you have enough money for your retirement, whatever that looks like, is very serious business. It is okay to hope that governments figure it all out and can send you your pension and meet their other obligations. But hope is not a strategy, just as denial is not a river in Egypt. We (and I do include myself here) need to be very realistic about the assumptions we are making for returns and what our future retirement portfolio values will be.