by Menzie Chinn, Econbrowser.com

Appeared originally at Econbrowser 05 February 2014

Caption illustration added by Econintersect.

The output gap remains large, even as the external sector supports growth; this outcome is partly due to excessively rapid fiscal consolidation

Economic Slack, Now and Next Year

The CBO released Budget and Economic Outlook on Tuesday 04 February 2014. As part of the report, the CBO released its estimates of potential GDP in a manner consistent with the new GDP measures that incorporate intellectual property in the investment data. The output gap remains large and negative, using these updated estimates.

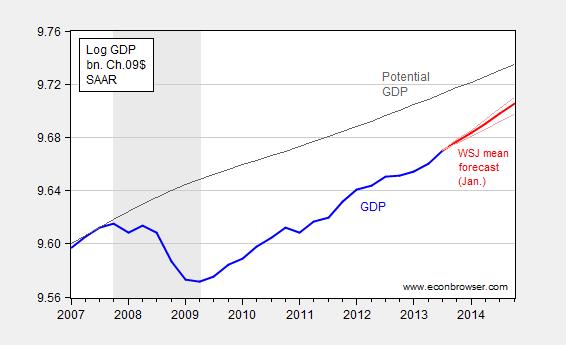

Figure 1: Log GDP (blue), mean forecast from January WSJ survey (red), and high and low forecasts from 20% trimmed sample (pink), and potential GDP (dark gray), all in billion of Ch.2009$, SAAR. NBER defined recession dates shaded gray. Source: BEA 2013Q4 advance release, CBO Budget and Economic Outlook (February 2014), Wall Street Journal January survey, NBER and author’s calculations.

Note that by 2013Q4, the output gap is -4.3% (log terms), and taking the mean WSJ survey response, the output gap at 2014Q4 is -2.9%. Even with the high estimate of GDP growth (after trimming the sample by 20%), the gap is -2.4% (Joseph Carson/Alliance Bernstein), whereas the low (after trimming) forecast indicates a -3.7% gap (Julia Coronado/BNP Paribas). The CBO projection (under current law, and based on data available as of December 2013 and the 2013Q3 second release) is 3.3%.

Fiscal Policy in Action

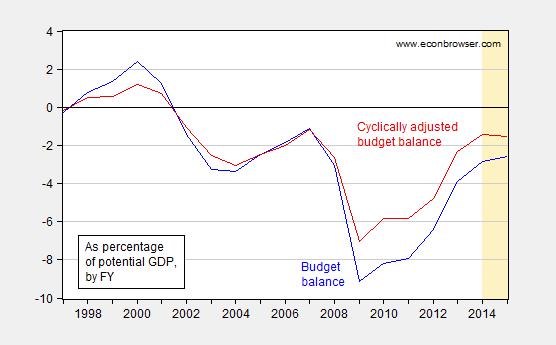

Part of the reason the progress in shrinking the output gap slowed in 2013 can be directly attributable to fiscal drag — in other words the prediction that the sequester would slow growth was realized. [1] (When the sequester deal was nearly finalized in April February, Macroeconomic Advisers forecasted 2.6% growth for 2013 , with an sequester plus Fed offset scenario growth of 2.1%; q4/q4 growth turned out to be … 2.7%. [2])[Edits 2/7 8:25AM – MDC] Consider the shrinkage in the cyclically adjusted budget balance (expressed as a share of potential GDP). The adjusted deficit shrank substantially in Fiscal Year 2013.

Figure 2: Budget balance (blue) and cyclically adjusted budget balance (red), both as a share of potential GDP, in percentage points. Tan shaded areas denote forecasts. Source: CBO Budget and Economic Outlook (February 2014).

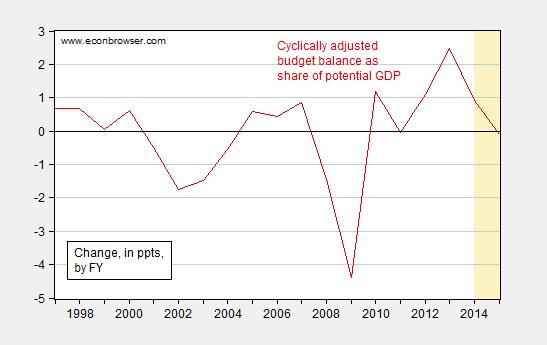

It’s perhaps easier to see the extent of fiscal consolidation by examining the change in the cyclically adjusted budget balance, as displayed in Figure 3.

Figure 3: Change in the cyclically adjusted budget balance as a share of potential GDP, in percentage points. Tan shaded areas denote forecasts. Source: CBO Budget and Economic Outlook (February 2014), and author’s calculations.

Notice the adjustment peaks at nearly 2.5 ppts of potential GDP in FY2013, and nearly a percentage point in FY2014. For more on fiscal drag, see [3] [4]

The External Environment

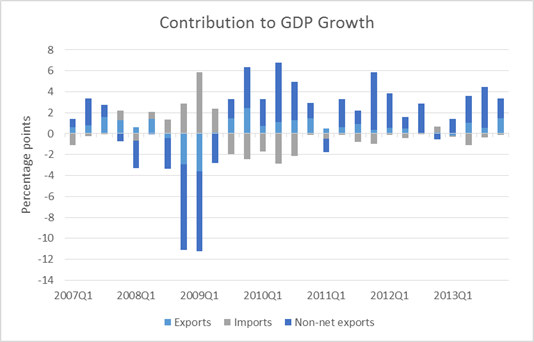

Net exports accounted for 1.33 of the 3.2 ppts of growth in 2013Q4 (SAAR); exports accounted for 1.48 ppts.

Figure 4: Contributions to real GDP growth from exports (light blue), imports (gray), and consumption, investment and government spending (dark blue). Source: BEA 2013Q4 advance release and author’s calculations.

The advance estimate relies upon forecasts of certain components, including December exports and imports (which will be released Thursday morning). One question is whether support from net exports will continue into the future.

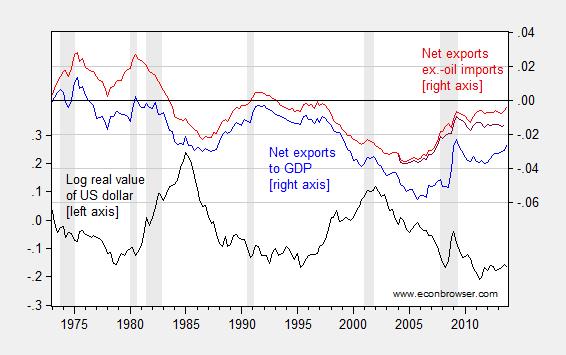

Figure 5: Log real value of US dollar against broad basket of currencies (black, left axis), net exports (blue, right axis), net exports ex.-oil imports (red), and net exports ex.-oil products (dark red), as a share of GDP. NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, BEA 2013Q4 advance release, BEA/Census, NBER, and author’s calculations.

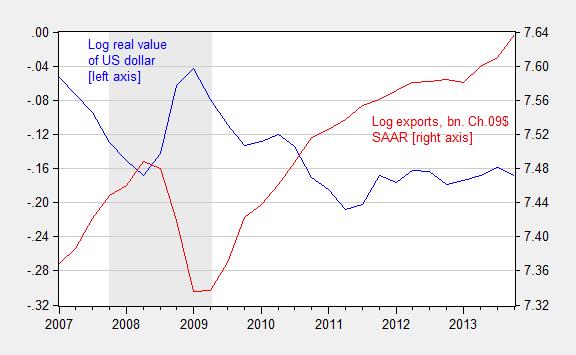

In other words, there has been substantial improvement in the trade balance. Exports in particular have surged in the past couple quarters, despite the relative stability of the US dollar, in inflation adjusted terms.

Figure 6: Log real value of US dollar against broad basket of currencies (blue, left axis), and log exports of goods and services, in billions of Ch.09$ SAAR (red, right axis). NBER defined recession dates shaded gray. Source: Federal Reserve via FRED, BEA 2013Q4 advance release, and NBER.

It remains to be seen whether export growth will continue at this pace given the turmoil in emerging markets and the tentative nature of the recovery in Europe. In particular, depreciating emerging market currencies [5] could result in a stronger dollar — the daily nominal index has recently exceeded levels in early July and in August. For its part, CBO projects a relatively stable dollar in 2014, while Deutsche Bank forecasts a twelve-month 8% appreciation (from 12/18).

Update, noon 2/6: December trade figures released today indicated a $38.7 billion trade deficit, slightly larger than the Bloomberg consensus of $36 billion. Jim Dorsey at IHS-Global Insight as well as Macroeconomic Advisers estimate that 2013Q4 growth will be 0.4 ppts lower (q/q SAAR) as a consequence of these figures.

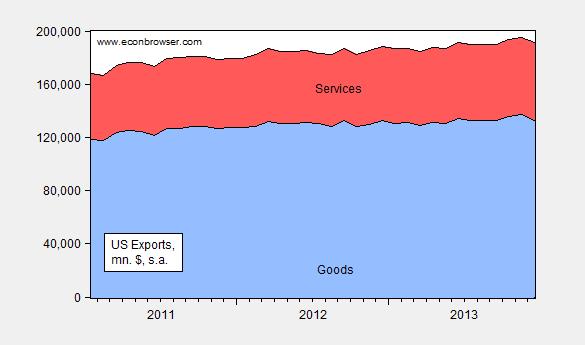

Nominal exports are shown in Figure 7 below.

Figure 7: Nominal exports of services (blue) and services (red), in millions of dollars, per month, seasonally adjusted. Source: BEA/Census.